{kind=link}

Almost 70 years ago, in Shippingport, Pennsylvania, the world’s first nuclear power plant started to produce electricity. This power plant was relatively small in output, being able to produce just 60-megawatts of power. That’s dwarfed by modern day nuclear power plants, such as the Bruce Nuclear Generating Station in Canada, with the ability to produce 6550-megawatts. But that small nuclear in Pennsylvania proved uranium could be harnessed to produce abundant and reliable electricity. The so-called Atomic Age had begun.

But then it faltered. While nuclear power enjoyed growing support in the 1970s, particularly in light of the OPEC oil embargo, by the end of the century it went into decline. Nuclear energy as a share of global electricity peaked at 17.6% in the late 1990s, falling to around 10%. In the US, that share has fallen from around 20% in the 1990s to around 18% today. The Atomic Age, it seems, never really got going.

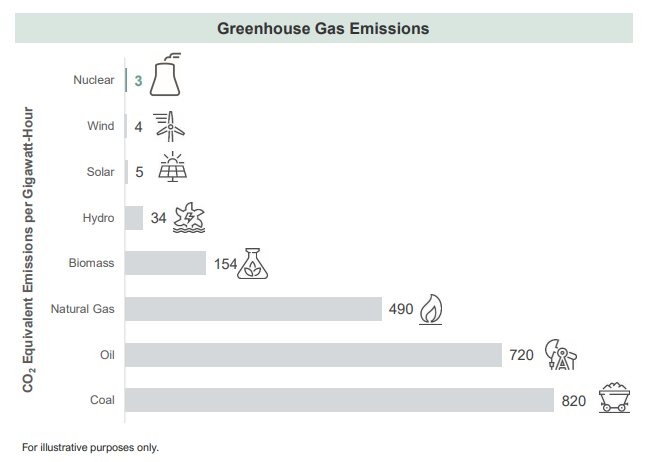

Now, with the twin threats of climate change and energy security, nuclear energy may now be at a turning point. At COP 28, we saw 22 countries, including the US and UK, commit themselves to tripling their nuclear energy capacity by 2050. This is on the back of a growing consensus that nuclear power is vital for any feasible pathway to net-zero. Nuclear energy produces almost no carbon emissions, while avoiding the intermittency issues that still plague renewable energy forms. While solar and wind will play a role in decarbonising electricity grids, nuclear energy will be required for reliable, baseload generation.

When it comes to energy security, nuclear power stands out. Unlike most energy sources, nuclear will typically have two years of fuel stored on-site. As a result, nuclear power is much less vulnerable to fuel supply disruptions. Following the invasion of Ukraine, Europe shifted away from Russian gas, resulting in energy price spikes. This makes nuclear energy highly appealing. At the same time, the cost of nuclear energy fuel – uranium – represents a relatively small amount of the operating costs of a nuclear power plant. As a result, nuclear energy is much less vulnerable to price shocks when compared to oil and gas.

What does this nuclear renaissance mean for investors?

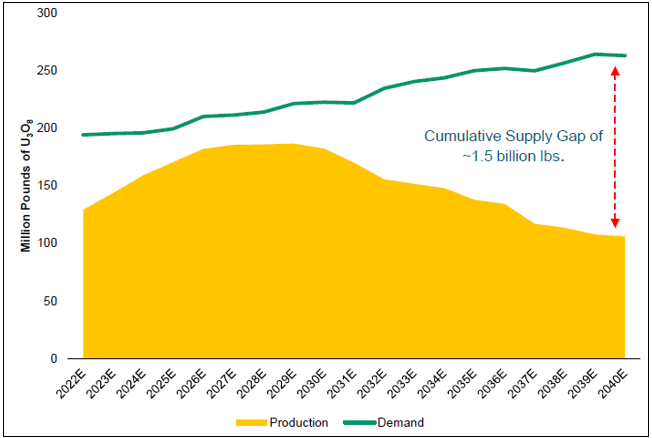

This expected expansion of nuclear power coincides with relatively low levels of uranium production. Primary uranium mine supply is significantly trailing demand, with a forecasted cumulative supply shortfall of approximately 1.5 billion pounds by 2040.

Notably, we’ve also seen Kazatomprom, the world’s largest uranium producer, cut its forecast production for 2024 by 14%. The company also noted it would likely miss its 2025 forecast productions.

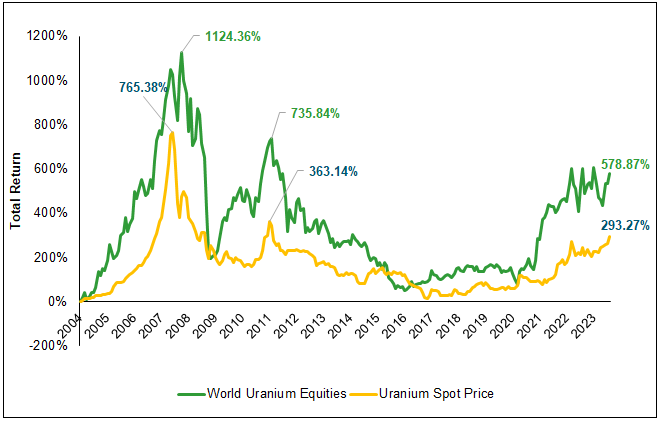

As a result of these supply and demand dynamics, the spot price of uranium has surged. In 2023, the price of one pound of uranium went from $48 to $91, while in 2024 the price breached $106 per pound.

As a result, uranium miners may be poised to generate higher revenues and potential profits when mining production ramps up. While in 2023, uranium miners lagged the performance of the spot price, historically, miners have outperformed.

In particular, there is a growing interest in the prospects of smaller cap – or “junior” – uranium miners. With uranium prices now around $100 per pound, it becomes economical for many of these new producers to either begin or restart production. At the same time, junior miners may be better placed to participate in the surge in uranium prices. While many of the larger producers have contracted their future production at historically lower prices, that is often not the case for the junior miners. Output from the smaller producers has the potential to be sold into the market with higher prices.

Will the uranium market stabilise?

As with all mining and materials, uranium is theoretically cyclical. Higher prices send a signal to producers to increase output, which in turn brings prices back down. While this cyclical dynamic has the potential to play out over the longer term, supply increases will not come quickly or easily. As we’ve already noted, the world’s biggest producer, Kazatomprom, is struggling to meet its forecast production for both this year and next. At the same time, it will take years for new large-scale mining projects to start providing supply. As Cantor Fitzgerald notes, “The next cohort of new large-scale uranium mine builds are not expected to come on-line until the 2028-2030 time period. This schedule is permitting/construction timeline dependent and cannot be pulled forward regardless of uranium price.” As a result, uranium prices have potential to increase further.

Alternatively, when the price of a commodity remains relatively scarce, with prices elevated and supply unable to increase, we sometimes see “demand destruction”. End users either cease operation or switch to alternatives. The risk of this happening for uranium, we believe, is relatively low. As noted above, nuclear energy is vital for achieving net-zero and energy security.

At the same time, nuclear power plants can absorb these higher costs. As noted above, uranium represents around 4-8% of a nuclear plant’s ongoing costs. That makes nuclear fuel buyers price agnostic. As Ocean Wall notes: “The fuel buyer at the nuclear power plant will never get in trouble for the price they pay for uranium, but instead for not securing the supply of it. To the world’s nuclear power plants uranium is completely price inelastic – they must have it.”

The price of uranium, alongside uranium miners, therefore, is potentially positioned for strong appreciation, as demand continues to surge among a market facing severe supply constraints.

Educational content produced as part of a paid partnership

Important information

Capital at risk. The value of your portfolio with InvestEngine can go down as well as up and you may get back less than you invest. ETF costs also apply.

This communication is provided for general information only and should not be construed as advice. If in doubt you may wish to consult a professional adviser for guidance.

Tax treatment depends on personal circumstances and is subject to change, and past performance is not a reliable indicator of future returns.