{kind=link}

Originally published in HANetf’s Thematic & Digital Assets Review

Copper plays a central role in the energy transition

Critical in construction, industrial machinery, electronics and more, copper’s utility in wide-ranging applications has made the copper market the behemoth it is today. The copper market is the third largest metals market by dollar value and the price of copper is considered a barometer of the health of the global economy.

Copper’s superior electrical conductivity, second only to silver, has made it particularly indispensable to the transmission of electricity. As a result, copper’s previous supercycle, led by the industrialization and urbanization of China, is giving way to a new cycle dominated by the global energy transition.

The world is committing to net-zero targets

Electricity demand is expected to surge 86% by 2050, relative to 2022. Underlying this are developing economies expanding electricity usage and nations around the world engaging in a global energy transition to phase out CO2-intensive energy sources with cleaner sources.

The European Union (EU) and 193 countries have now ratified the Paris Agreement, an international treaty to slash greenhouse gas (GHG) emissions on a schedule intended to limit global warming to 2 degrees Celsius (or preferably, to 1.5 degrees Celsius). To achieve this, the world needs to reach net-zero emissions by the year 2050.

Decarbonisation is copper intensive

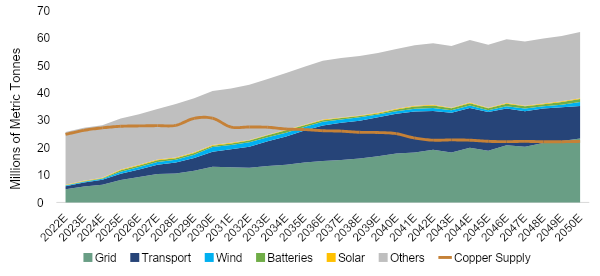

The clean energy transition relies on carbon-free electricity, both in our power grids and transportation vehicles. All systems that produce, transmit and store electricity depend on copper for transmission.

Decarbonizing transportation necessitates the transition from burning fossil fuels in cars with internal combustion engines (ICE) to electric vehicles (EVs). Similarly, decarbonizing power generation requires the transition from burning fossil fuels, i.e., natural gas and coal, to cleaner sources. In the case of transport, EVs require 2.4x more copper than ICE vehicles. Renewable energy sources, solar and onshore wind, both require 2.5x more copper than their fossil fuel counterparts for an equivalent amount of energy produced (per MW). Offshore wind, however, requires an even greater amount of copper at 7x that of fossil fuel counterparts per MW.

Consequently, copper demand may increasingly be driven by EVs and renewables. Renewable investments are expected to grow steadily for years and electric vehicle sales in 2022 eclipsed 10 million, or 5x the EV sales in 2019.2 Further, EV sales for 2023 are forecast at 14 million vehicles, putting 23 countries at the 5% adoption rate. This adoption rate is considered a tipping point for a technology’s penetration of its overall market as it moves along an “S” curve from early adopters to early majority.

Carbon-free technologies are copper-intensive and require the expansion of electricity networks, which rely on copper. As the amount of electricity produced globally increases, there is an increase in the amount of grid development to connect new builds. New builds of wind and solar plants are generally smaller than other sources like coal and gas plants and, therefore, require a greater number of power plants, which need an increase in power lines. Finally, these plants are more likely to use underground power lines, which, rather than overhead lines, often use copper. Undergrounding is increasing the demand for copper as urbanization grows.

Figure 1: Copper supply and demand imbalance likely to grow

Copper’s supply is struggling to meet demand

The global copper supply is constricted, and supply may likely not be able to match the increases in demand. The copper mining market is large and mature, with the red metal first mined thousands of years ago. Many of the high-quality projects have already been mined and major copper discoveries are becoming less common, and ore grades are declining. Today, they are typically 1% or less compared to 150 years ago when they exceeded 5%. Long lead times compound the issue as it takes, on average, 16.5 years to move from discovery to first production. Existing copper mine projects have also been the subject of numerous disruptions. For instance, multiple challenges have impacted Codelco, the world’s largest copper producer, which recently reduced 2023 production guidance after posting its lowest copper production in approximately 25 years in 2022. These supply constraints signify the importance of copper miners.

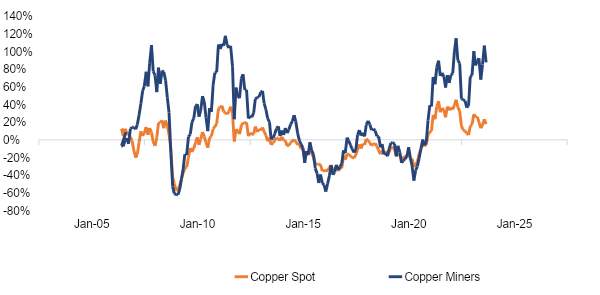

Opportunity for copper miners

Copper prices and copper miners may gain from the widening supply-demand disparity. Some copper miners, in particular, are benefitting from the increasingly bright long-term copper demand outlook. Copper is a strategic focus for the largest diversified miners and has been driving mergers and acquisitions in 2022-2023. Mining giants BHP and Rio Tinto both purchased copper miners at $6.4B and $3.3B, representing 49% and 67% stock premiums, respectively. Automakers are also concerned about future security of critical minerals supply like copper and some are making direct equity investments into miners. Stellantis invested $155 M in McEwen Copper in February 2023 and then upped its investment by another $120 M in October.

Investments in copper miners may be poised to increase, given the supply-demand dynamics, and the potential for copper equities to provide operating leverage to the underlying spot price. In addition, we believe the copper price will have to rise further to incentivize new production to meet the growing demand.

Figure 2: Copper equities outperform spot during bull markets

Educational content produced as part of a paid partnership

Important information

Capital at risk. The value of your portfolio with InvestEngine can go down as well as up and you may get back less than you invest. ETF costs also apply.

This communication is provided for general information only and should not be construed as advice. If in doubt you may wish to consult a professional adviser for guidance.

Tax treatment depends on personal circumstances and is subject to change, and past performance is not a reliable indicator of future returns.