{kind=link}

TL;DR: The right “keep vs invest” split comes down to one question: how confident are you that you won’t need the money soon? Start by ringfencing taxes and near-term obligations, then build an operating buffer that matches your risk. Only after that should you consider investing what is genuinely surplus.

This article is only meant to constitute general information, not financial advice. Every business has different cash-flow risk. You should keep enough cash to meet obligations and avoid being forced to sell investments at a bad time.

Why cash in the bank can be misleading

A healthy bank balance can hide cash that isn’t really available. VAT you have collected may be due soon. Corporation Tax may be building up quietly across the year. Annual bills or a planned hire might be around the corner.

If you invest before you clearly earmark cash into various categories, you can accidentally commit money that has a deadline attached to it.

A safer approach is to separate cash into three buckets: obligations, buffers, and surplus.

Ringfence the non‑negotiables first

Most small businesses have commitments that, if missed, cause immediate damage. VAT, payroll, and key supplier payments tend to be the big ones, with rent, debt repayments, and insurance close behind. Even if you do not calculate these perfectly, the act of ringfencing them reduces the risk of being caught out.

If you want a simple starting checklist of what usually counts as “non‑negotiable”, it’s typically:

- Tax liabilities (VAT and Corporation Tax)

- Payroll and employer costs

- Rent or premises costs

- Key supplier payments

- Debt repayments and leases

- Insurance and professional fees

If you do only one thing, start a “tax pot”. It’s one of the simplest ways to stop VAT or Corporation Tax money blending into day-to-day cash and disappearing.

Build a buffer that reflects your risk

Once obligations are covered, the next decision is how much buffer the business needs. The right buffer depends on how predictable revenue is and how quickly you can adjust costs if something goes wrong.

If your income is up and down, or customers pay late, or you rely on a small number of clients, you typically need a larger buffer. If you have stable recurring revenue and predictable costs, you may be able to run leaner.

The goal of the buffer is to protect you from being forced into bad decisions, like missing payroll or selling investments during a market dip. It pays to be cautious here, as having a buffer that’s too big beats having one that’s too small.

Define “surplus cash” in a practical way

Surplus cash is not “what’s left at the end of the month”. It is the cash you can genuinely leave untouched without putting operations at risk. A useful test is to imagine revenue dropping next month. If you could still pay staff, suppliers, and tax without panic, you are closer to having true surplus.

Once you have that clarity, you can start to consider investing as a long-term decision rather than a short-term bet.

Match any investment plan to your time horizon

Even when cash is surplus, timing still matters. Money you might need in weeks or a couple of months is usually better kept accessible, because markets can fall and selling takes time. Money you won’t need for years can usually tolerate more volatility, because you have time to ride out downturns.

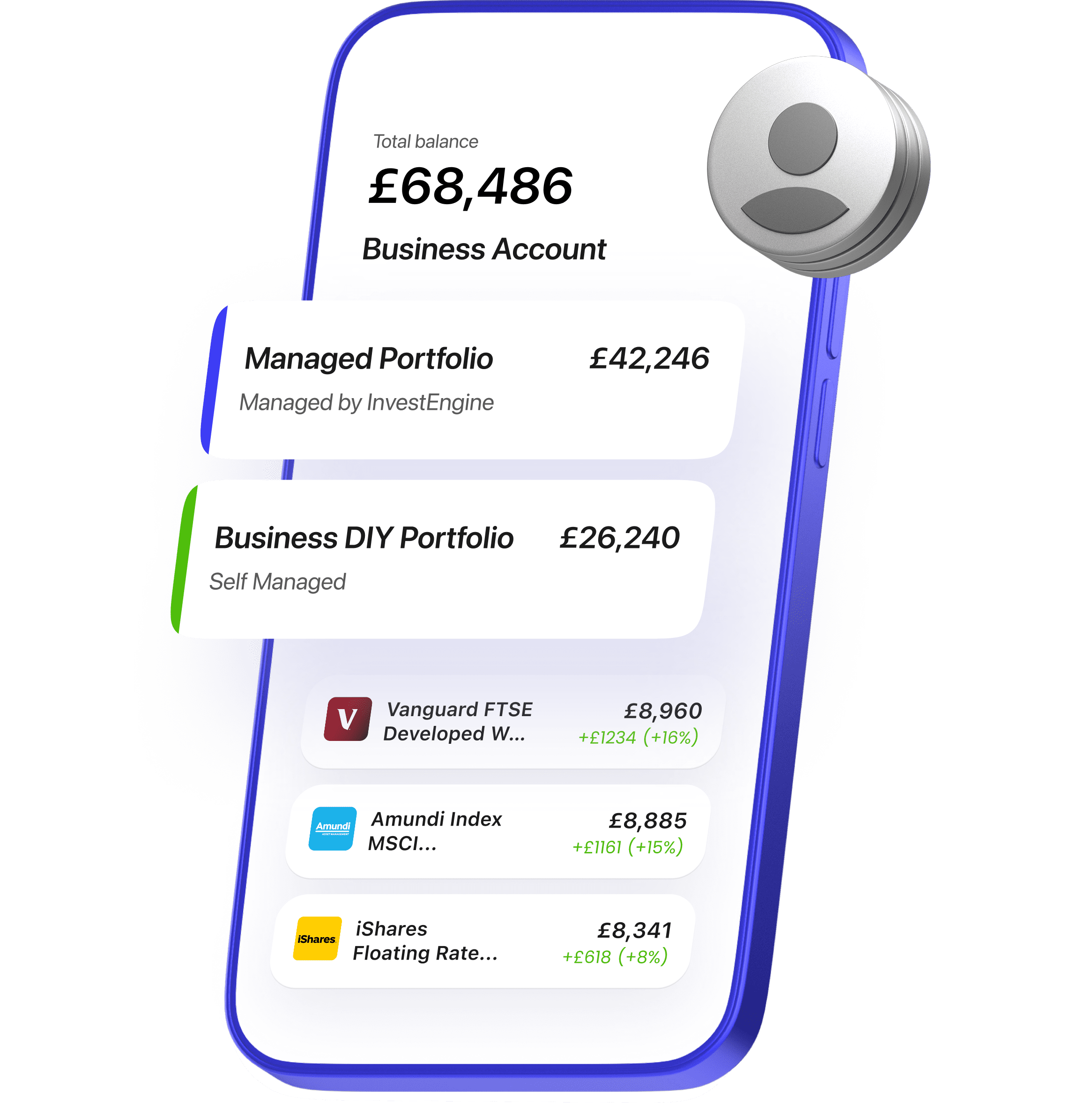

Once you’ve considered all of this, you can start putting that surplus cash to work in the form of a business investing account. Any of the other cash isn’t appropriate to invest. Be honest with yourself and the needs of your business, and err on the side of caution when it comes to buffers.

Put your business cash to work

Take advantage of powerfully simple business investing with InvestEngine. We make it easy to build and maintain a long-term investment portfolio that suits you and your business.

Find out moreCapital at risk. Ts&Cs apply

FAQs

Is it bad to hold “too much” cash?

Too much idle cash can lose purchasing power over time, but too little cash can threaten day-to-day operations. The right balance depends on predictability and plans.

How should I think about payroll as part of my buffer?

Payroll is not just wages. You need to consider the timing of PAYE/NIC payments and pensions, and many businesses choose a buffer that comfortably covers payroll through a bad month.

Can I invest money I might need for a tax bill?

Only if you are confident on timing and you are comfortable with investment risk and withdrawal timelines.

What’s the first practical step if I’m unsure?

Build a simple 13-week cash-flow forecast and list the next 12 months of obligations. That usually makes the “keep vs invest” decision much clearer.

Important information

Capital at risk. The value of investments may go down as well as up, and you may get back less than you invest. Past performance is not indicative of future performance. ETF costs apply. Tax rules can change and any benefits depend on individual circumstances. If in doubt, consider professional advice.