{kind=link}

TL;DR: For a UK small business owner, a Business Account complements personal investing rather than replacing it. A typical stack is: a Stocks & Shares ISA (tax-free growth and withdrawals, up to £20,000 a year), a SIPP (tax relief on contributions, accessible from age 55, rising to 57 in 2028), and an InvestEngine Business Account (a General Investment Account in the company’s name) for surplus company cash and retained profits. InvestEngine allows ISAs, SIPPs and Business Accounts to be held on the same platform.

If you run a small business, investing probably means multiple different things to you. There’s the money you’re building up for your own future, and there’s your company’s cash.

A Business investment account sits alongside your personal investments, not in place of them. Think of it as building a stack of accounts, each with a clear job to do.

Personal investments: your tax-efficient base

Most UK investors start with the personal wrappers, because the tax benefits are hard to beat.

First, there’s the Stocks & Shares ISA for up to £20,000 a year tax-free growth, dividends, interest and withdrawals. Ideal for medium- to long-term personal goals.

Then you have the Self-Invested Personal Pension (SIPP) for retirement. You get tax relief on contributions, the money grows tax-free, and you can usually access it from age 55 (rising to 57 in 2028).

For most people, filling personal ISA allowances and contributing sensibly to a SIPP are the first steps. These are the workhorses of personal investing.

Business Account: your company’s cash, put to work

A Business Account does the equivalent of these personal accounts, but for your company’s money. This cash that technically belongs to your business, not to you personally.

It’s useful for:

- Surplus cash sitting in the business bank account, earning little to no interest

- VAT and Corporation Tax money that you might set aside in advance, which can earn a potential return on the way to its due date

- Long-term retained profits that you don’t plan to distribute as dividends in the short term – you can invest this instead

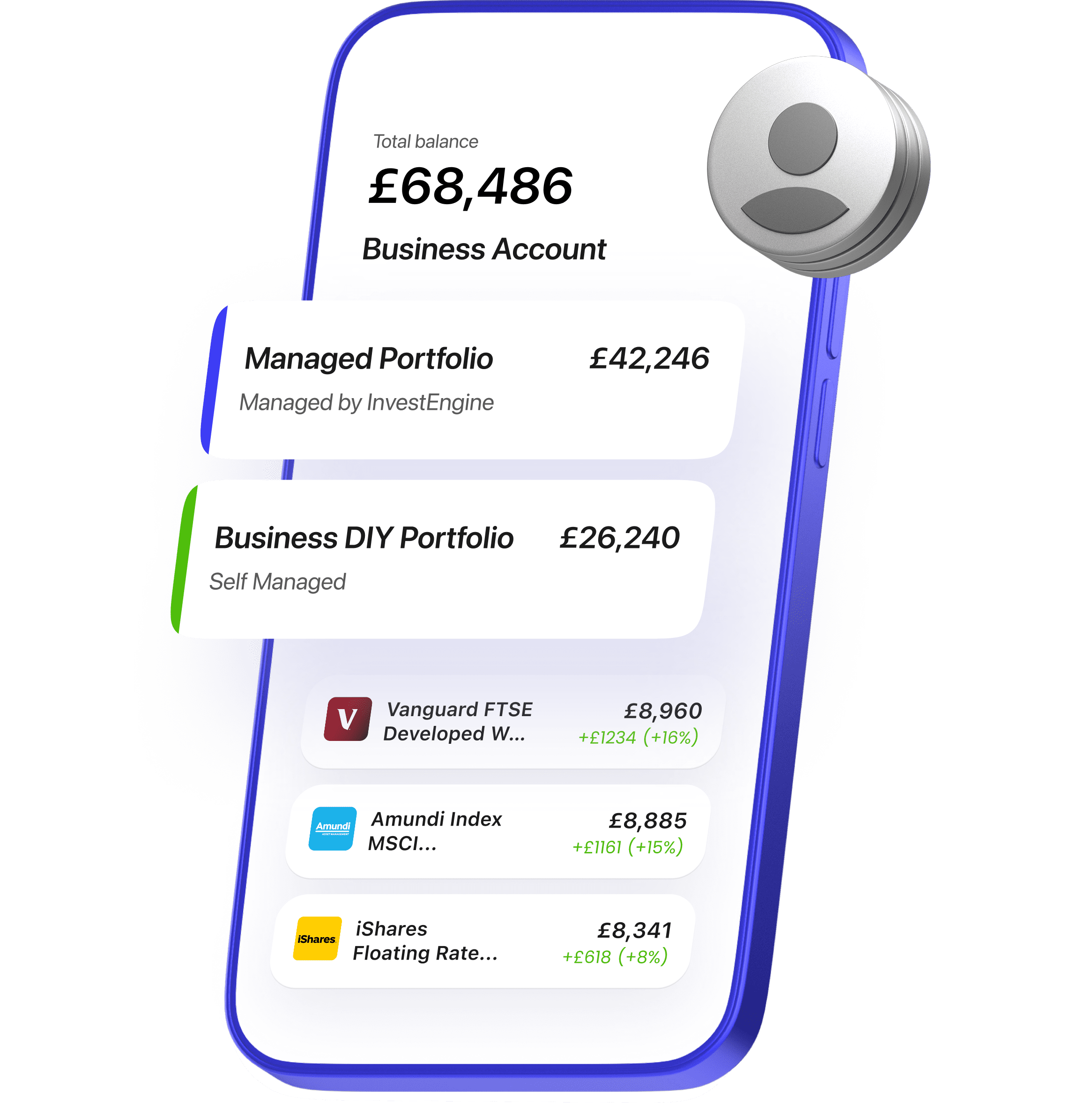

A business account is a separate, ring-fenced General Investment Account (GIA) in your company’s name, so company money stays as company money on the balance sheet.

A typical small business owner’s stack

A founder, contractor or freelancer running a limited company might end up with something like this:

- Personal Stocks & Shares ISA: £20,000 a year of tax-free investing for personal goals

- Personal SIPP: tax-efficient contributions for retirement

- Business Account (GIA): for the company’s surplus cash and longer-term retained profits

Each account has a clear job, and each one is taxed differently. Together they give you a flexible way to invest both your personal money and your company’s.

How the pieces tend to be used (a quick example)

Imagine a founder paying themselves a small salary and the rest in dividends through their limited company:

- Salary and personal dividends → into the personal current account → topping up the ISA and the SIPP each year.

- Surplus cash in the business (beyond next quarter’s VAT, payroll buffer and a sensible reserve) → into the Business Account, possibly split between:

- An Overnight Rate or short-duration bond ETF for near-term cash and tax money

- A diversified portfolio for retained profits the company doesn’t need for 5–10+ years

No one account is doing it all, and that’s the point. It’s a fully functional stack of investment accounts designed to compliment the investor’s broader goals.

Why it matters that they’re kept separate

Keeping personal and company investments in their own separate accounts is beneficial for a few reasons:

- Clear ownership. There’s never any ambiguity about which money belongs to you vs. your company.

- Cleaner accounting and tax. Your company accounts only need to deal with the company’s investments; your personal tax return only deals with yours.

- Different risk and time horizons. Your retirement pot might be 100% global equities; your company’s VAT-money buffer probably shouldn’t be.

- Cleaner exit planning. If you ever sell the company, distribute funds or change structure, separate accounts make the process much simpler.

Should I prioritise personal investing or the Business Account?

This is one of the most common questions we see from business owners. The answer depends on the business, the owner and the goals.

Generally, your personal tax wrappers (your ISA and SIPP) are often used first or in parallel, because the tax benefits are powerful.

It usually makes sense to keep a healthy cash buffer in the business bank account before investing any surplus. This is to cover any unexpected expenses your company might have.

For anything specific to your situation, your accountant or a qualified financial adviser is the right person to help you weigh it up. InvestEngine doesn’t give personal advice.

All under one roof

With InvestEngine, you can hold your ISA, SIPP and Business Account all on the same platform. This gives you one login, one set of tools, and one place to manage everything. Personal goals and business goals can be laid out side by side, with consistent reporting and the same range of ETFs across all accounts.

To summarise

A Business Account doesn’t replace your personal investing, it complements it. Used together with an ISA and a SIPP, it gives small business owners a complete toolkit for putting both their own money and their company’s money to work, with each account doing the job it’s designed for.

Put your business cash to work

Take advantage of powerfully simple business investing with InvestEngine. We make it easy to build and maintain a long-term investment portfolio that suits you and your business.

Find out moreCapital at risk. Ts&Cs apply

Important information

Capital at risk. The value of your portfolio with InvestEngine can go down as well as up and you may get back less than you invest. ETF costs also apply.

Tax treatment depends on individual circumstances and is subject to change. This communication is provided for general information only and should not be construed as advice. If in doubt you may wish to consult a professional adviser for guidance.