{kind=link}

Welcome to the latest edition of our monthly market roundups. This time we’re looking at the key topics from June, as well as covering a few of last month’s more unusual market stories.

As has been the theme so far in 2023, inflation and interest rates were the headline, with stubborn inflation forcing the Bank of England to raise rates even further.

Interest rates continue to rise

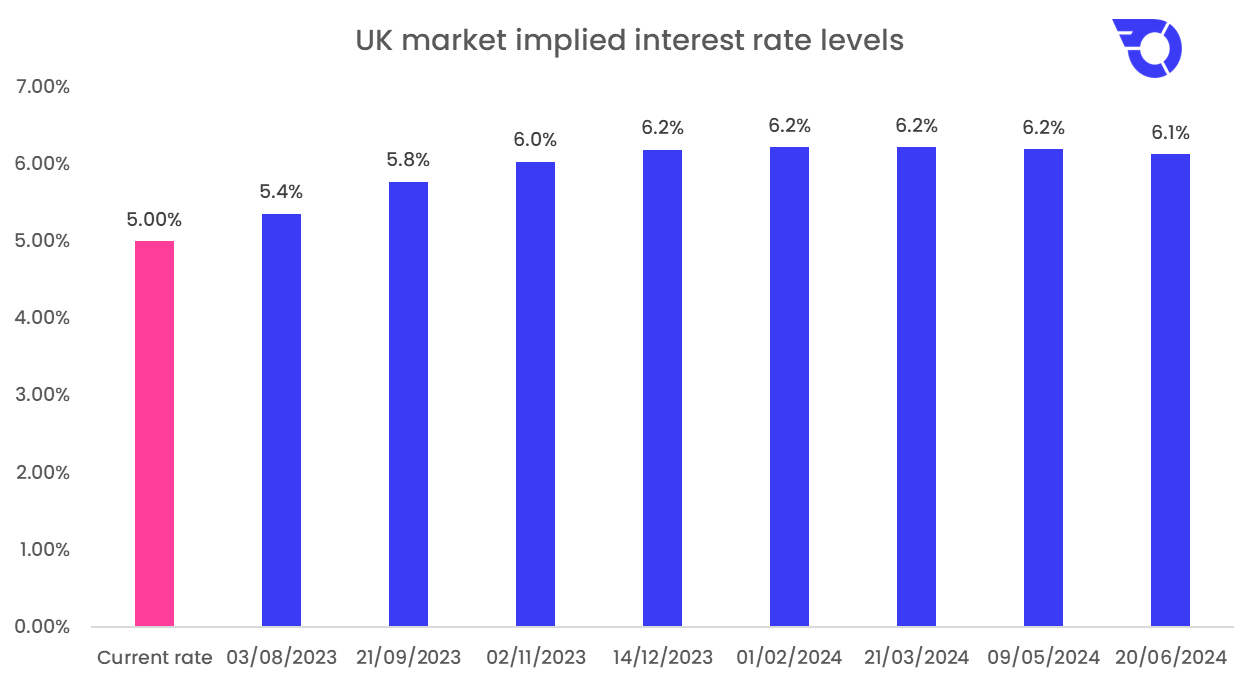

The Bank of England defied the market’s expectations with a surprise 0.5% rise in interest rates on 22 June, taking the base rate to 5%.

UK interest rates are now at their highest level since 2008, with the market expecting rates to climb to over 6% by the end of the year, the highest figure since 2000.

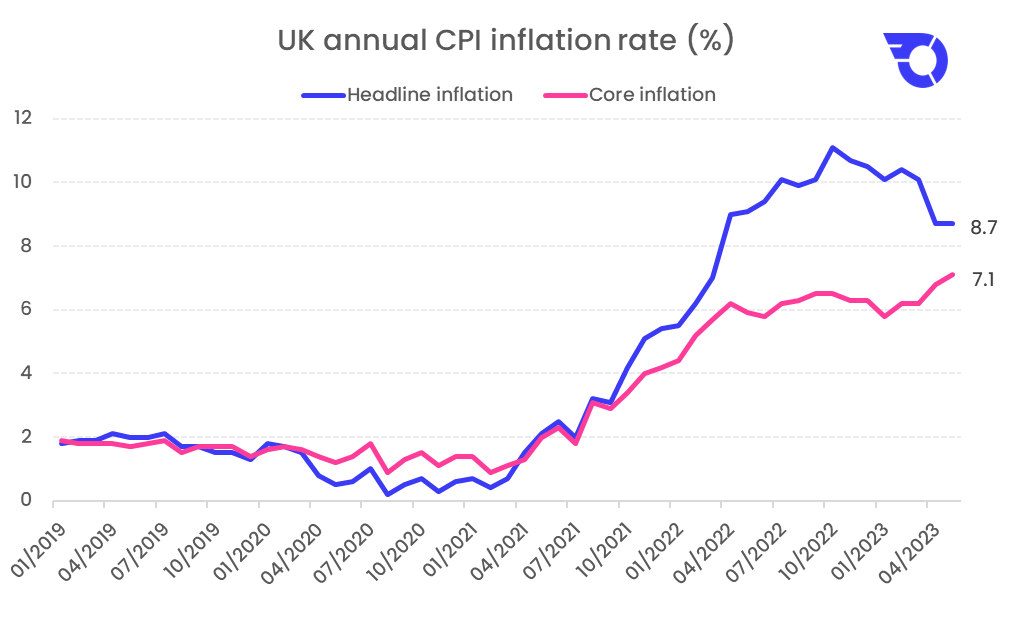

The Bank of England is stepping up its fight against persistent inflation, voting seven to two in favour of the larger-than-expected increase. Inflation remained stuck at 8.7% last month, more than four times the Bank’s target (of 2%).

Higher interest rates are designed to make the cost of borrowing more expensive, encouraging consumers to reduce spending and companies to cut back on hiring and investment, with the aim of bringing down inflation.

Inflation remains stubborn

UK inflation surprised the market by increasing for the fourth month in a row. Despite the market expecting inflation to fall, the headline rate remained unchanged at 8.7% in May (the same as in April). More importantly, core inflation – which strips out the more volatile elements of the headline inflation figure, including energy and food – was predicted to match April’s 6.8% rate. Instead, it accelerated to 7.1%. This is the highest rate since March 1992.

Partly reflecting pent-up demand from the time of the pandemic, UK households are continuing to spend. This is contributing to higher services inflation. Prices for recreational and cultural goods and services grew by 6.8% year-on-year in May, up from 6.4% in April. Partly offsetting a 13.1% drop in petrol prices, air fares became 20% more expensive than they were a year ago.

Equity markets post positive returns

June was a strong month for equity markets, with all major markets posting positive returns.

The US led the way, rising 3.9% in sterling terms and bringing year-to-date returns to an impressive 11.2%. As the US makes up around 60% of the global market, its performance has been a fantastic boost for investors.

However, the US’ performance has been particularly concentrated in a few specific stocks.

Within the US, it has really been a story of only seven stocks this year: NVIDIA (+174% YTD), Meta (+126%), Tesla (+101%), Amazon (+47%), Apple (+42%), Microsoft (+35%), and Google (+29%).

These stocks have all benefited from the rapid developments in artificial intelligence, as well as the wider optimism surrounding the technology sector. These seven stocks have together accounted for all of the S&P 500’s return so far this year – meaning the performance of the index without these stocks wouldn’t have been the +11.2% we’ve seen so far this year. Rather, the index would actually be in negative territory.

Europe has also been performing well this year, gaining a further 2.4% in June. The UK rose 1.4%, bringing year-to-date gains to 3.1%. Emerging Markets posted a 1.1% gain in June, but is still lagging on a YTD basis at -1%.

Bond yields boosted by interest rates

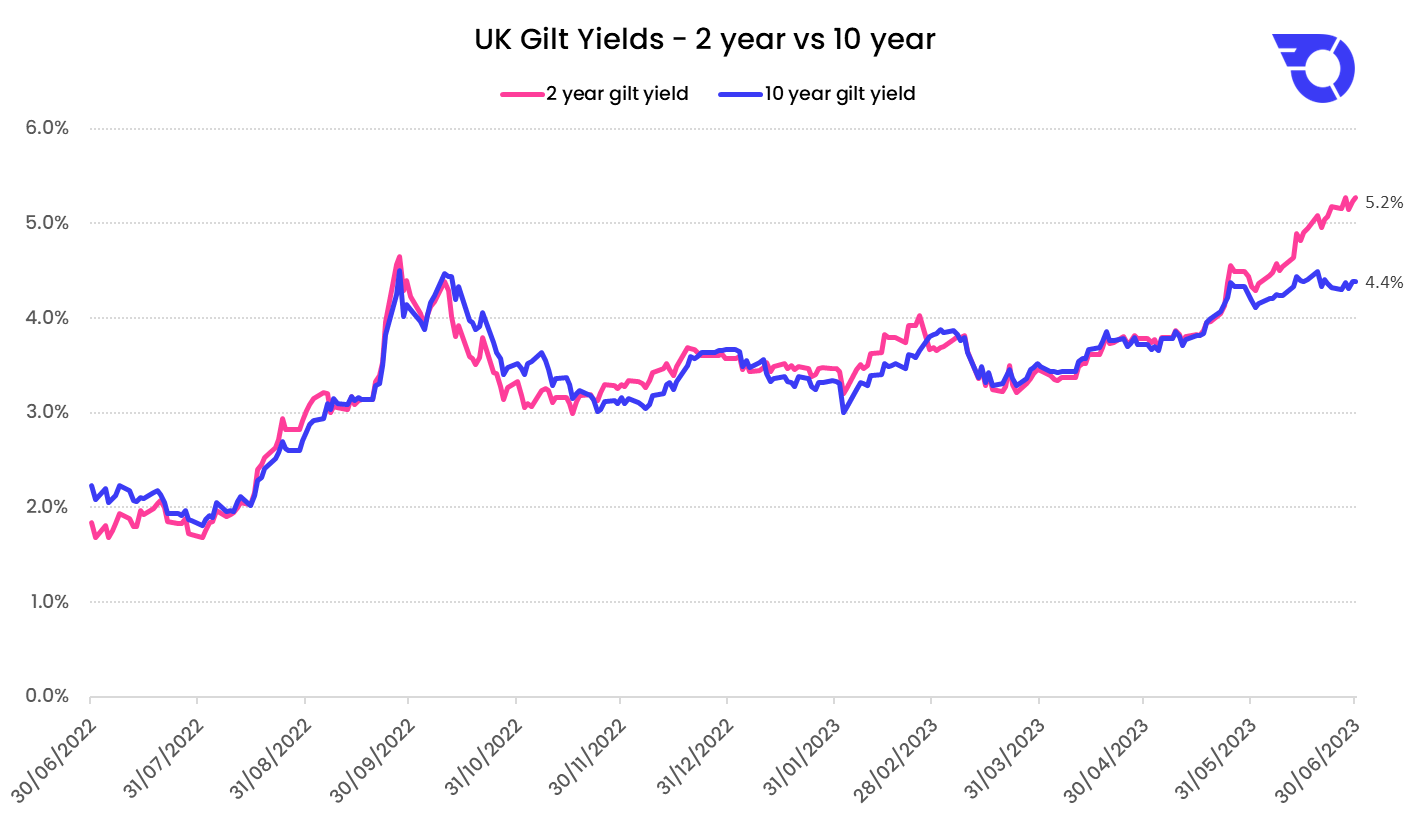

Following the larger-than-expected interest rate hike, bond yields rose over the month, with the UK 2-year government bond (gilt) yield rising to 5.2%. The UK 10-year gilt yield rose to 4.4%.

As the shorter-duration 2-year gilt yield now yields more than the longer-duration 10-year gilt, this is known as a ‘yield curve inversion’. When we have an inverted yield curve, bonds with longer maturities have lower yields than those with shorter maturities. Sometimes referred to as a negative yield curve, an inverted curve is sometimes viewed as an indicator of a recession.

Currencies

Versus the US dollar, sterling strengthened by 2.1% in June, rising from a rate of $1.2441 at the start of the month, and finishing at a rate of $1.2703.

Sterling’s rise over June was due in large part to the US dollar’s weakness, with the Fed’s pause in rate hikes combined with weaker US employment data rekindling hopes that the Federal Reserve’s hiking cycle may be behind us.

Versus the Euro, the pound was flat over June, finishing the month at €1.1637.

Off the beaten track

Now, let’s take a look at some of the more unusual market news stories from June.

Apple is taking on apples in a truly bizarre trademark battle

Apple, the company, wants rights to the image of apples, the fruit, in Switzerland.

Jeff Bezos buys a single Amazon share

Stock market analysts were scratching their heads in June when Jeff Bezos, the world’s third-richest person, did something strange: He bought a single share of Amazon for $114.77.

Elon Musk and Mark Zuckerberg agree to a cage fight

Interns have their faces broadcast across Times Square

Morgan Stanley honoured its 2023 summer analysts by broadcasting their faces and names in Times Square. The investment bank beamed the headshots of its newest summer analysts on the screens at their Times Square headquarters, sharing their full names around the building’s video boards.

“This week, we welcomed over 1,000 Analysts and Associates in North America as part of our intern class of 2023,” Morgan Stanley wrote on its LinkedIn page. “We celebrated their arrival with a tribute in Times Square and an unforgettable experience on the historic Intrepid Sea, Air & Space Museum.”

Pickleball injuries may cost Americans nearly $400 million this year

Shares of large US health insurance companies fell in June after UnitedHealth Group Inc. warned that healthcare utilisation rates were up. The company had said it was seeing a higher-than-expected pace of hip replacements, knee surgeries and other elective procedures.

UBS Group analysts offered a surprising theory about one factor that could be driving a higher pace of injuries: pickleball.

Important information

Capital at risk. The value of your portfolio with InvestEngine can go down as well as up and you may get back less than you invest. ETF costs also apply.

This communication is provided for general information only and should not be construed as advice. If in doubt you may wish to consult a professional adviser for guidance.

Tax treatment depends on personal circumstances and is subject to change, and past performance is not a reliable indicator of future returns.