{kind=link}

Since the beginning of 2022, markets have been going through a rocky patch. The fallout from the global pandemic, coupled with Russia’s ongoing invasion of Ukraine, has sent inflation soaring and pushed many of the world’s leading economies into recession.

When markets are this volatile, it’s natural for people to want to liquidate their assets into cash and wait it out. Unfortunately, this can be a counterproductive response, particularly during periods of high inflation like the one we’re experiencing now. With cash savings being eroded over time, it’s worth looking elsewhere when building a long-term financial plan.

In this article, we’ll look at the potential cost of getting it wrong and the benefits of sticking with a long-term plan. We’ll also explain why trying to ‘time the market’ is usually a bad idea.

The cost of missing out

The problem with selling during difficult periods is that you deny your portfolio the opportunity to recover by crystallising your losses. Investors always want to ‘buy low and sell high’; it’s near impossible to get this right consistently, but selling when things are down is a surefire way to lose money.

The important thing to remember is that, historically, stock markets do recover. And, when they do, these recoveries tend to be sharp. Historically, the market’s worst days tend to be followed by its best days.

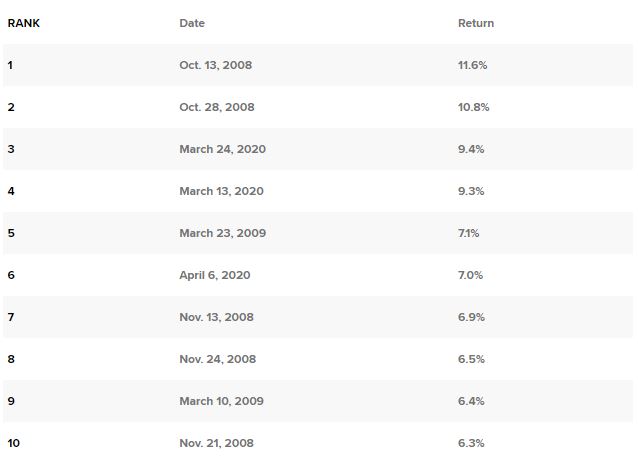

The table below shows the 10 best days in the markets over the last 20 years. Even a quick look at the dates tells you that all of them came after some historically difficult periods.

Source: J.P. Morgan Asset Management analysis using data from Bloomberg. Returns are based on the S&P 500 Total Return Index, an unmanaged, capitalization-weighted index that measures the performance of 500 large capitalization domestic stocks representing all major industries.

These recoveries can take place over a matter of months too. When the S&P 500 lost 21% in the first half of 1970, it then recovered sharply with growth of 26.5% in the second half. These are the positive periods we’re talking about when we talk about missing out.

If you’d invested $10,000 into the S&P 500 on January 1 2002, you’d have had a balance of $61,685 on December 31 2021 if you stayed the course. If you’d somehow missed the 10 best days during that period, you’d be left with $28,260.

Of course, past performance is not a reliable indicator of future returns and we could see turbulence for some time to come. This is simply here to illustrate the fact that markets are cyclical and downs are a part of investing, just like growth.

So, is now a good time to invest?

This is an easy one: yes. When you take a medium to long-term approach to investing, the answer is almost always yes. Diversification, risk level, luck – these all make a difference to an investor’s fortunes, but nothing is as impactful as time.

This is why any wealth manager focused on long-term returns will tell investors to stay the course and avoid trying to time the market. No one has a crystal ball and having faith in the long-term growth of your portfolio is a safer strategy than trying to predict the top or bottom of the market.

Staying the course can be uncomfortable when things become turbulent but it’s important to see the swings as part of the wider investment plan. This is where a diversified investment portfolio can really help. Having your risk spread across different asset types, geographies and industries can help to smooth out volatility.

How pound cost averaging can help

Investing little and often is otherwise known as ‘pound cost averaging’. This is the process of drip-feeding cash into the markets to negate the impact of market timing on investment performance. Essentially, you’ll be buying both at the top, middle and bottom of the market over a long enough timescale.

Pound cost averaging can be useful in volatile periods. Most investors are naturally risk-averse, so the idea of investing heavily before a downturn is unpalatable. Equally, we all want to take advantage of any dips in the market by ‘buying low’. With pound cost averaging, the stress is taken away because timing the market isn’t the goal.

All you need to figure out with this investment strategy is how much you want to invest and how often. It could be a case of drip-feeding any disposable cash each month into markets, then you can sit back and have faith in your long-term, diversified approach. When you spread out your investments over time, you can avoid making any seriously costly mistakes; you won’t miss the best days in the markets and you won’t throw in a lump sum before a crash.

With an InvestEngine account, you can take advantage of our AutoInvest feature to make regular top ups even more convenient. If you pay in a monthly direct debit or your ETFs pay dividends, for example, you’ll have cash in your portfolio. Switch on AutoInvest and this cash will automatically be invested during the next trading window, using the ETF weighting you’ve already selected for your portfolio. Get your investment strategy in order so that you can get back to what really matters.

Important information

Capital at risk. Past performance is not a reliable indicator of future returns. The value of your portfolio with InvestEngine can go down as well as up and you may get back less than you invest. ETF costs also apply.

This communication is provided for general information only and should not be construed as advice. If in doubt you may wish to consult a professional adviser for guidance.