{kind=link}

For a topic that gets a lot of airtime, ETF liquidity is widely misunderstood by people in the investment industry. And, given the extraordinary times that we are living in today, understanding ETF liquidity has never been more important. In this piece, our partners at Rize ETF debunk some of the longstanding misconceptions around ETF liquidity that we continue to hear from people in the investment industry.

1. What is an ETF?

An ETF is an investment vehicle that trades on a stock exchange, and allows investors of all types to buy and sell it throughout the trading day (in the same way that you can buy and sell shares in a publicly-traded company). From a regulatory perspective in Europe, an ETF is no different to a mutual fund. Both are typically structured as UCITS funds. The main difference between an ETF and a mutual fund is that an ETF can be bought and sold in real-time throughout the business day whereas a mutual fund can only be traded at the end of the business day.

2. What is liquidity?

In simple terms, “liquidity” in the context of investments is a measure of how readily you can buy or sell an investment.

For example, shares in a large publicly-traded company are typically very liquid as there is a high level of public demand to invest into the company meaning at any given time there are always plenty of people who are willing to either buy or sell shares in the company. The value (number of shares multiplied by the price) traded in a day can often be used as a measure of the liquidity of the company. For investors, this is important, primarily because investors want to have the ability to sell their shares on demand. A company that has a low volume of shares traded could be difficult to sell, especially in times of market stress.

3. How do you measure the liquidity of an ETF?

One of the biggest misconceptions with ETFs is the notion that you can generalise their liquidity based on their structure. ETFs come in many shapes and sizes tracking a wide range of asset classes, therefore it is impossible to generalise the liquidity of ETFs. However, it is not the ETF structure itself that determines the liquidity of the ETF. Like any mutual fund, it is the underlying assets that the ETF is invested in that determine its liquidity.

We discuss above how you can measure a company’s liquidity based on the value that trades on exchange. Later we will debunk the myth that the same measure can be used to measure an ETF’s liquidity, where it is wrong to look at the value of shares traded of the ETF itself.

Accordingly, in order to assess the liquidity of an ETF (i.e. how readily you can buy or sell shares of the ETF), you have to look at and assess the liquidity of the assets held by the ETF.

4. Why does an ETF’s assets determine its liquidity?

We can use a simple example of a FTSE 100 ETF. The ETF will hold all of the FTSE 100 companies matching the percentage weights that are in the FTSE 100 index. If you want to invest £10m in an ETF that provides exposure to the FTSE 100 index, the ETF investment manager needs to be able to buy £10m worth of shares in the companies comprised within the FTSE 100 index. If you sell that ETF, the investment manager sells the FTSE 100 companies to be able to pay you for the shares that you are selling.

Using this example, an ETF which invests in the companies comprised within the FTSE 100 Index, will have a liquidity profile matching the FTSE 100 companies’ liquidity. Comparatively, an ETF which invests in a basket of high yield bonds, will be as liquid as those bonds. As different asset classes (bonds, equities, commodities, real assets etc) exhibit different levels of liquidity, their respective liquidity profiles will be reflected in the corresponding ETFs that are designed to provide exposure to them. Therefore, we cannot generalise the liquidity of ETFs, each has their own liquidity characteristics according to what they are invested in. A fund structure often has conventions for the frequency of trading, e.g. intraday (ETFs), daily (mutual funds), monthly (certain hedge funds) but the frequency is not always linked to the liquidity. What matters (on top of the frequency that you can buy or sell the fund) is what each specific fund or product invests in, as that is what needs to be bought or sold to ensure sufficient liquidity for investors to buy and sell the fund.

To recap, in determining the liquidity of an ETF, what matters are the assets in which the ETF invests, because it is those securities that need to be either bought or sold to enable investors to buy and sell the ETF.

5. Why is the ETF structure not relevant to an ETF’s liquidity?

To understand why the ETF structure is not relevant in determining the liquidity of an ETF, it is critical to understand the basics of the ETF ecosystem and the roles and responsibilities of its key participants.

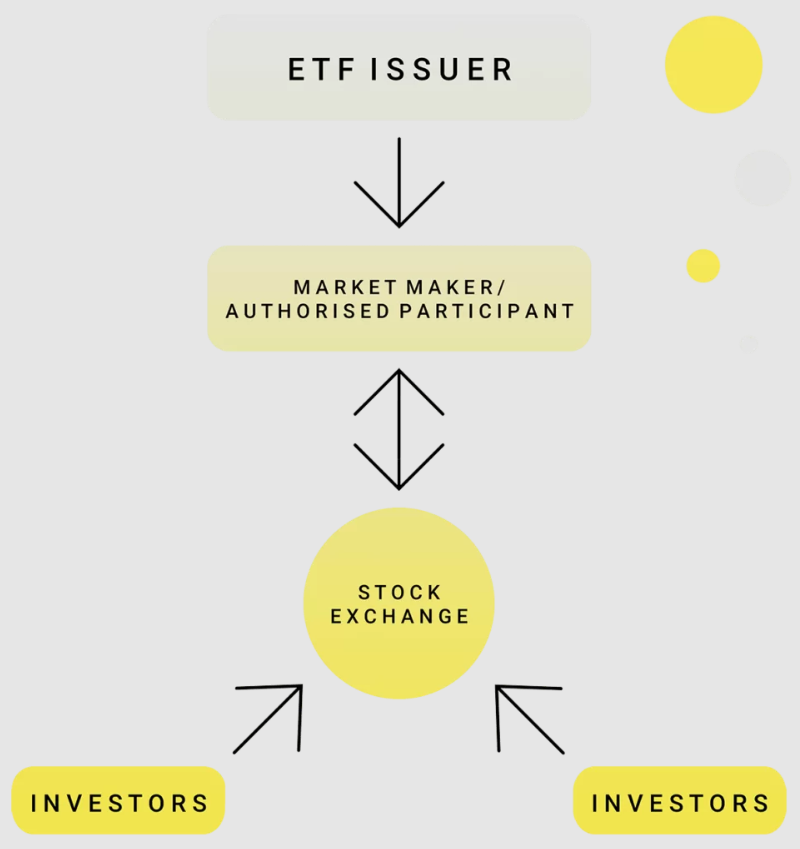

Firstly, ETFs have primary and secondary markets.

What is the primary market?

The “primary market” is for institutions called “Authorised Participants” who have legal agreements in place with the ETF that allow them to buy or sell shares in the ETF directly with the ETF issuer. These institutions are typically market makers who provide exchange liquidity, and other institutional ETF brokers, who create and redeem shares of the ETF directly with the ETF issuer. This involves increasing and decreasing the total ETF shares in issue. This is important as a fixed number of shares in issue would mean that an ETF is priced much more on the demand and supply of that ETF instead of the underlying assets. However, because ETFs are open-ended, it is the underlying assets that are the key driver of the price rather than ETF supply or demand.

We will look at this further in the premium and discount section below. When new shares are created in the primary market (e.g. an investor buys £10 million of ETF shares), the investment manager must buy the underlying assets of the portfolio, the opposite is true of redemptions, where shares are sold back to the ETF issuer and those shares are cancelled.

What is the secondary market?

The “secondary market” refers to all buying and selling of the ETF that takes place outside of the primary market. It is generally considered to be the ETF trading that occurs on the stock exchange. To trade on the stock exchange, an ETF requires a market maker. Each ETF traded in Europe will typically have a contractual market maker who commits to providing liquidity on exchange. This means that a market maker will be contractually obliged to offer a price for any investor who wants to buy or sell shares in the ETF. The market maker commits to a maximum distance between the buy and sell price to minimise the transaction cost for the investor.

The other important market maker commitment is in terms of the number of shares. A market maker will make a certain number of shares available to buy and sell on exchange, which is replenished as and when investors buy and sell the ETF. This means that even with zero demand for an ETF, an investor can still buy or sell on exchange.

How do ETFs ensure transparency in pricing?

As the market maker buys and sells ETF shares, they will build up net short positions (having sold shares to investors who are buying) or a net long positions (having bought shares from investors who are selling), and as such will be creating and redeeming shares in the primary market.

Before a market maker goes to the primary market, they will hedge their net long or net short positions in the ETF by buying or selling the underlying holdings of the ETF to stay market neutral. They can do this accurately, and therefore price the ETF accurately, because they know, often with an error margin of less than 0.01%, exactly what the ETF holds. It is this transparency that ETFs have become known for relative to other investment vehicles.

6. How does ETF arbitrage work?

The ability of market makers to create and redeem in the primary market is a key aspect of ETFs, making them open ended. This means that an ETF should always be fairly priced on exchange. For example, if an ETF is trading at 1% above its fair value according to the underlying assets, then someone can sell the ETF on exchange at a premium, and be able to satisfy the sell trade by creating the ETF in the primary market, thereby locking in a 1% profit (less trading costs) in what is known as arbitrage. This arbitrage mechanism relies on tradable underlying assets in the ETF and helps to ensure that ETFs trade at fair value.

7. Why can ETF exchange liquidity be misleading?

Exchange liquidity is dependant primarily on the ability of the market maker to create and redeem in the primary market, and to hedge their position (buy or sell the ETF’s underlying assets) prior to trading in the primary market. So, the key message is that the amount available to buy or sell depends on whether the underlying assets of the ETF can be easily bought and sold.

An ETF can have zero shares traded on exchange or have vast numbers of shares traded on exchange, however, what really matters is the underlying assets. This is a crucial part of understanding ETF liquidity. For example, if a FTSE 100 ETF has zero demand from investors and therefore shows no volume traded, a traditional view of liquidity will say that the ETF is illiquid, that it cannot be easily bought or sold by investors. However, this far from reality, an ETF is not an individual stock or share, but instead an investment fund that only requires liquid underlying assets (the FTSE 100 companies in the example) to be liquid at the fund level. Therefore, liquidity needs to be looked at differently to traditional stocks or shares liquidity. In this example of a FTSE 100 ETF, having zero ETF shares traded for even a year, has no impact on the ETF being able to trade $50 million in a single day. This is because the investment manager of the ETF can invest $50 million dollars into the FTSE 100 companies with no issues. Therefore, the ETF shares traded is not a suitable indicator of liquidity. All it tells you, is the investor demand in that particular ETF.

Another example is a more illiquid underlying, for example junk bonds. In normal circumstances, a popular junk bond ETF may have significant volume on exchange as investors buy and sell the ETF throughout the day. However, the underlying is typically more illiquid than the above example. Therefore, in more extreme market conditions where the result is investors all selling at the same time, then the underlying bond liquidity is tested and again, the exchange volume of the ETF itself is not a relevant indicator of liquidity. The investment manager needs to sell the underlying junk bonds to other buyers who may be few and far between. This is the relevant aspect of the ETF’s liquidity profile.

The message here is that the liquidity that really matters is dependent on the underlying assets of an ETF, as it is for any other open-ended fund structure for that matter.

As an ETF becomes more popular and has increased trading volumes, more market makers may also provide two-way pricing for the ETF despite not having a contractual relationship with the ETF issuer, this can lead to more competitive pricing.

8. Does size matter?

A common misconception around ETFs is that those with lower assets under management “AUM” are less liquid and therefore are riskier for an investor to hold a significant proportion, or that it might impact an investors ability to sell. This is not necessarily true, and again, what typically matters most are the underlying constituents that need to be traded when the ETF is bought or sold. The other ETF size consideration is whether the ETF has sufficient assets to effectively hold and therefore track the underlying constituents of the index. For example, if an ETF tracks a corporate bond index with 1,000 bonds, it may not be able to do that effectively with USD 1 million, this is a separate point to liquidity.

If we take a FTSE 100 ETF that has USD 1 million in total assets under management, an investor might be wary of investing for liquidity reasons, however, due to the liquidity of the underlying FTSE 100 companies, an investor can very comfortably invest USD 50 million in a day bringing the total assets to USD 51 million. All that has happened is that the investment manager has bought USD 50 million of the FTSE 100 companies, exactly the same as if the investment manager is managing an ETF with USD 10 billion in existing assets or USD 1 million in ETF assets. Similarly, if the next day the same investor wants to redeem the USD 50 million invested, this is almost 100% of total assets in the example, leaving USD 1 million remaining in the ETF. Given the underlying assets are the FTSE 100, this again is no issue, the remaining USD 1 million is perfectly sufficient for the ETF to continue operating and tracking the FTSE 100 companies.

There is also another interesting area to consider for larger ETFs with more assets under management. If an ETF, based on its underlying assets can handle USD 50 million of sell trades in a normal single day and has total assets of USD 100 million, that means it can handle a 50% redemption. If an ETF with the same underlying assets has USD 1 billion, it can only handle a 5% redemption (USD 50 million). This can be an important consideration when looking at the existing AUM of an ETF, it may be considered too large relative to the liquidity of the underlying assets as a bigger issue than being too small. In this example, the larger assets can be detrimental if the same percentage of investors want to sell their holdings.

9. What are premiums and discounts?

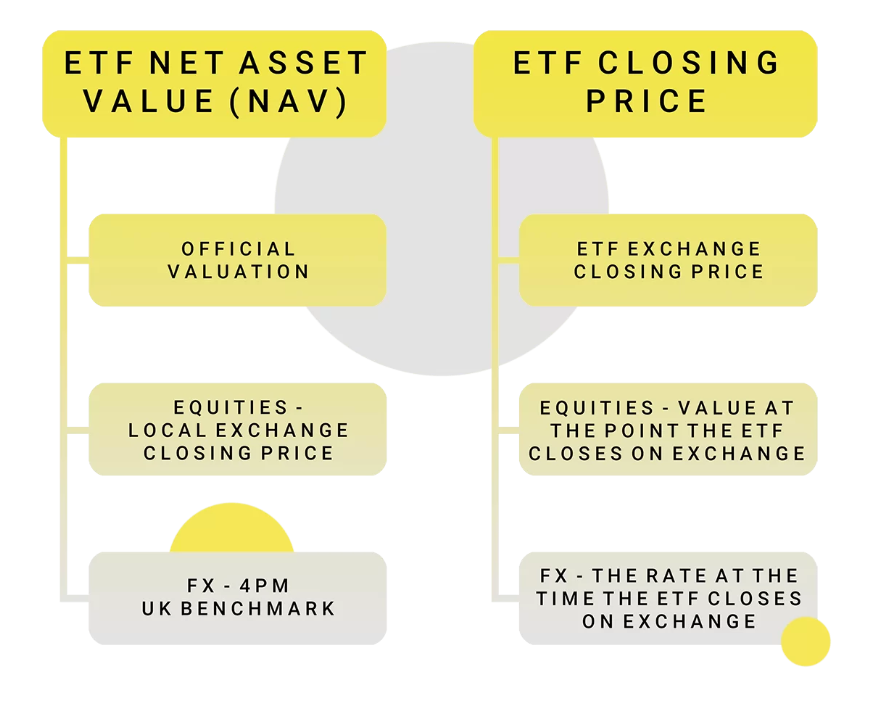

Another area and another misconception that can often be linked to ETF liquidity are premiums and discounts. Each ETF, as with any fund, has a Net Asset Value “NAV” which is calculated by an administrator, typically daily. The standard is to use the closing price of the underlying constituents of the ETF and an exchange rate benchmark at 4pm UK to convert any assets not priced in the base currency into base currency. The price on exchange of the ETF is the last traded price when the exchange closes, in Europe typically 4.30pm UK. The difference in price between the NAV per share and the price on exchange is often referred to as a premium or discount. The below chart highlights the inputs into each the NAV and the ETF exchange closing price, the difference of which is described as the premium or discount.

10. Why are ETF premiums and discounts misleading?

Based on the above definition, it is important to understand whether premiums and discounts for ETFs are a fair comparison. What if you have a European ETF that invests in US equities? The closing price of the ETF on the LSE for example will be the value of the ETF’s underlying assets at 4.30pm UK, however, the NAV value will use the closing price of the US equities which is 9pm UK. Therefore, different values are expected, and are not genuine premiums or discounts. Now, only if the closing times of the exchange the ETF trades on and the closing times of the underlying assets of the ETF exactly match is this a fair comparison, making many premium and discount metrics for ETFs redundant and misleading.

Even if there are any underlying assets with a closing time matching the time the ETF closes on exchange, there may be other misleading factors. If the underlying assets are not in the base currency of the ETF, then the exchange rates used are relevant. For most funds, the exchange rate used to value the assets is a 4pm UK benchmark. However, the exchange rate at the time the ETF closes on exchange, is the exchange rate at that time, 4.30pm in the UK. This is another misleading factor in using premiums and discounts in ETFs.

11. When are premiums and discounts fair?

If the NAV and the exchange closing time of the ETF are exactly the same, then the premium or discount can be used, for example, a FTSE 100 ETF, that trades on the LSE. The ETF has an exchange closing price at 4.30pm, also the NAV uses the 4.30pm closing prices of the underlying companies. However, for any ETF with global underlying assets, this metric is unlikely to be suitable and will be misleading. Theoretically, a real premium or discount should use a snapshot of the NAV using valuation times that match the exchange closing times that the ETF is traded on, this is not something that is typically done or in fact easily done.

The arbitrage mechanism described in the “What is the secondary market?” section ensures ETFs should trade at fair value. There are always nuances, and this is typically dependant on how tradeable the underlying assets are. This is where liquidity matters, liquid underlying assets should not trade at consistent premiums or discounts.

12. Why did there appear to be premiums and discounts during the recent crisis?

A useful example is the recent market turmoil’s impact to the premium and discount for high yield fixed income assets. Here there were major discounts, implying the ETFs were trading on exchange well below the NAV. There are several possible causes for this, but high yield fixed income is often considered a less liquid asset, meaning when most investors are sellers, there are limited buyers to satisfy the market demand without a significant drop in price. This means that a published price, is not always a tradeable price for an illiquid bond. In fact, the demand to sell the ETF can exceed the ability to sell the underlying assets. This is reflective of what the underlying asset is, not of the ETF structure.

A closer and more in-depth view of the above example shows some interesting conclusions. This requires a more detailed analysis on the pricing methodology in the NAV, meaning, what value for the bonds is used for the daily NAV. There is not always a transparent tradeable closing price for bonds as there is in equities. Therefore, multiple price sources may disagree and provide multiple closing prices for the same bond. In theory, the price of the ETF on exchange reflects the actual cost of trading the underlying bonds, the price is a tradeable quoted price. However, the price in the NAV is a published price representing the price of the underlying bonds that is not necessarily reflective of a tradeable value, but instead, is just a price given by a data vendor who prices bonds. Therefore, a bond could have a published closing price from a data vendor used in the NAV of 100. In normal times, this may be a tradeable price. However, during a crisis, if an investor is to sell a large quantity of the bonds, then that is not a price a seller will trade at and the actual tradeable price may be much lower. This is what can and has made ETFs appear to trade at a discount when in fact, it is due to the NAV not reflecting a tradeable value in an illiquid asset class during a time of crisis.

In this case, arbitrage that is described earlier is not possible. When trades occur in the primary market, transaction costs are typically added, this includes where the sell price of the bonds achieved by the ETF investment manager does not match the price in the NAV. This means that Authorised Participants (APs described in the Primary Market section) who redeem shares in the primary market, will pay the actual cost that the fund incurred selling the bonds, not the published price of the bond used in the NAV. This avoids existing investors suffering a loss that would otherwise be borne by the fund allowing a redemption at the published NAV value. This is why all costs are typically passed through to the AP creating or redeeming in the form of transaction costs, including the price differential between the sell price of the bond and the value of the bond in the NAV (in other mutual funds, this may be referred to as a “Swing Pricing” mechanism). An alternative is the AP redeems ETF shares for bonds themselves (the underlying asset of the ETF) rather than cash. This form of creation/redemption is typically prevalent in the ETF fixed income world, in this case, the price of the bond sold to the AP by the ETF matches the NAV price making the trade neutral from the perspective of investors in the fund and the AP. The AP bears the cost if that is not a tradable value as they now hold the bonds having sold the ETF in exchange for the underlying.

13. Conclusion

The key message is to always look at the underlying assets to determine true liquidity. Liquidity is not dependent on the structure of a fund, it is dependent on what that fund needs to buy and sell to satisfy creations and redemptions. On exchange, liquidity requires a market maker and the transparency that is typical in ETFs ensure that the market maker can accurately price the ETF. The volume of an ETF traded is not relevant in the same way as it is for an individual stock or share’s volume. There are many misconceptions around ETF liquidity, it is always crucial to look beneath the surface and examine the specific fund you may invest in rather than purely the structure alone.

Educational content produced as part of a paid partnership

Important information

Capital at risk. The value of your portfolio with InvestEngine can go down as well as up and you may get back less than you invest. ETF costs also apply.

This communication is provided for general information only and should not be construed as advice. If in doubt you may wish to consult a professional adviser for guidance.

Tax treatment depends on personal circumstances and is subject to change, and past performance is not a reliable indicator of future returns.