{kind=link}

“I have yet to see a time when it made sense to make a long-term bet against America,” said Warren Buffett, in his February letter to Berkshire Hathaway shareholders, reflecting on this past 80 years of investing experience.

It seems that the Sage of Omaha, as Buffett is known, is on the money. So far in 2023, the US economy and equity markets have shrugged off banking stress, recession risk and monetary tightening. However, to fully understand what is going on, it is worth taking a more nuanced look at the market. Different US indices have displayed vastly different performance. Indeed, the year to date has been yet another reminder to investors that index and product selection in US markets is one of the most important decisions, especially given that US equities account for around 70% of a global equity portfolio.

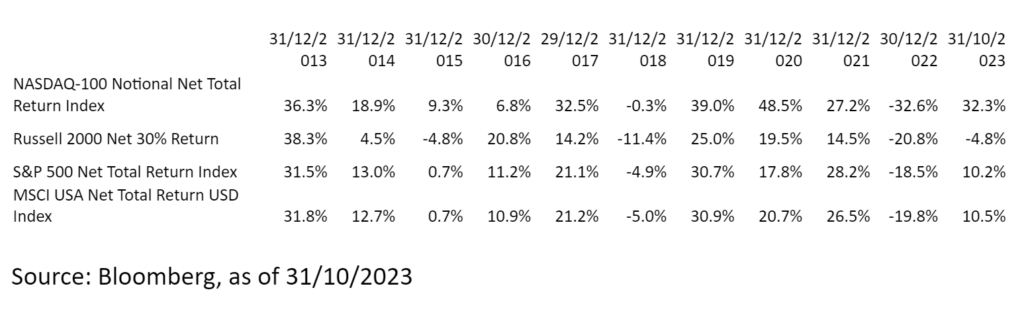

Even the differences between the two traditional entry routes to the US equity market, the S&P 500 Index and the MSCI USA Index, are widening this year.

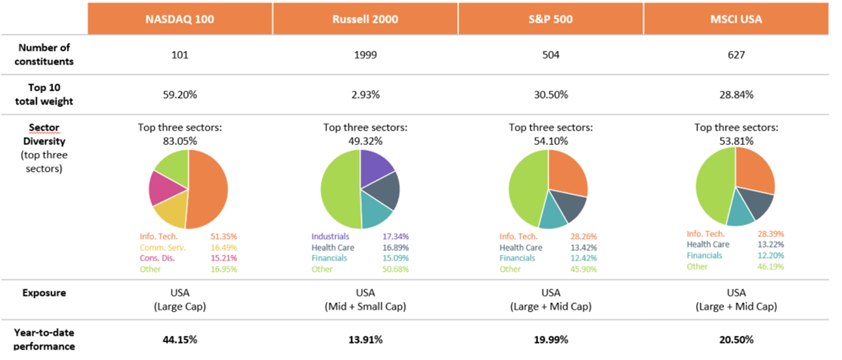

The S&P 500 is the most widely tracked index by exchange traded fund (ETF) investors in Europe² and comprises the shares of the 500 largest listed US companies. Together, these companies represent more than 80% of the total market capitalisation of companies listed on the US stock exchange. The MSCI USA has 626 constituents and slightly more mid-cap exposure. Over the past 20 years, the performance difference between the two indices has been around 0.06% per annum. However, over the past two years, we have seen episodes of relative outperformance or underperformance of 2%³. This illustrates how detached the performance of the heavier weightings in the US have become from the average US stock.

The differences are even greater when we look at two other widely followed indices: the Russell 2000 Index and the Nasdaq 100 Index. The Russell 2000 tracks small-cap companies, often seen as a bellwether for broader economic expectations. The index is down 4.8% in the year to end of October. The consumer-tech-heavy Nasdaq 100, which focuses on non-financial stocks listed on the Nasdaq exchange, is up more than 30% in a year that also marked the Nasdaq’s best first half year since 1983⁴.

The reasons for this performance disparity appear, at least on the surface, to be straightforward: the Nasdaq 100 comprises a smaller number of stocks, particularly in the consumer tech sector, many of which are already among the largest companies in the world. These have benefitted disproportionately from the recent sentiment around artificial intelligence and big data.

To better understand performance differences, a useful indicator is the weighting of the IT sector. The weighting of the sector varies widely across indices, with even the S&P 500, a supposedly diversified index, allocating a near 30% to information technology – it is slowly becoming a tech-driven index.

Concentration is another useful indicator. The higher the concentration of the index, the higher the allocation to these mega-caps.

Looking ahead, the artificial intelligence theme seems unlikely to kickstart another sensational half of US equity performance. DWS’ Chief Investment Office expects greater equity market volatility, driven by the demanding expectations now embedded in the valuations of the digital and tech titans that dominate the S&P 500. The average S&P 500 company is now currently trading at 20 times earnings, with the top 10 by market capitalisation at 30 times earnings, and the top five highest-valued companies at 60 times earnings⁵.

However, while earnings multiples are well above historical averages – suggesting expectations of strong future growth – they should still be kept in perspective. The Nasdaq 100’s multiple of 35 times earnings is still well below its record high of over 110 times earnings at the peak of the dotcom rally⁶.

Overall, while taking into account Warren Buffett’s sound advice to never bet against the long-term ability of the US economy to create wealth, shrewd investors might also wish to take a nuanced approach to US equities, bearing in mind the key principles of building diversified portfolios that are a true reflection of the broader US economy.

This could mean including sectors or thematic investments in allocations to maintain exposure to evolving themes, while avoiding some of the concentration that comes with being allocated to the largest stocks. Index selection within the US market is key. Xtrackers offers a range of US equity market ETFs, including one that provides exposures exposure to an equal-weighted version of the S&P500. The subtleties of the different types and styles of US equity indexes are definitely worth exploring.

What the NASDAQ 100 is already pricing in

Source: Bloomberg Finance L.P., DWS Investment GmbH as of 8/2/23

Educational content produced as part of a paid partnership

1 Source: MSCI, based on MSCI World country distribution, as of 31/10/2023

² Source: Bloomberg, based on AUM of UCITS ETFs, as of 31/10/2023

³ Source: Bloomberg, net total returns, as of 31/10/2023

⁴ Source: Bloomberg, net total returns, as of 31/10/2023

⁵ Source: Bloomberg, as of October 2023

⁶ Source: Bloomberg, as of October 2023

Important information

Reviewed and reissued by InvestEngine (UK) Limited which is Authorised and Regulated by the Financial Conduct Authority.

Created and issued in the UK by DWS Investments UK Limited. DWS Investments UK Limited is authorised and regulated by the Financial Conduct Authority. CRC 1758

PAST PERFORMANCE DOES NOT PREDICT FUTURE RETURNS

This document is intended as marketing communication. This document has been prepared without consideration of the investment needs, objectives or financial circumstances of any investor. Without limitation, this document does not constitute an offer, an invitation to offer or a recommendation to enter into any transaction.

Investments are subject to various risks, including market fluctuations, regulatory change, counterparty risk, possible delays in repayment and loss of income and principal invested. The value of investments can fall as well as rise and you may not recover the amount originally invested at any point in time. Furthermore, substantial fluctuations of the value of the investment are possible even over short periods of time.

Before making an investment decision, investors need to consider, with or without the assistance of an investment adviser, whether the investments and strategies described or provided by DWS are appropriate in light of their particular investment needs, objectives and financial circumstances. Information in this document has been obtained or derived from sources believed to be reliable and current. However, accuracy or completeness of the sources cannot be guaranteed.

Investors should refer to the Risk Factors in the prospectus and Key Investor Information Document (KIID). For general information regarding the nature and risks of the proposed transaction and types of financial instruments please go to https://etf.dws.com/en-gb/risks-and-terms/etf-risk-factors/

Any investment decision in relation to a fund should be based solely on the latest version of the prospectus, the audited annual and, if more recent, un-audited semi-annual reports and the Key Investor Information Document (KIID), all of which are available in English upon request to DWS Investment S.A., 2, Boulevard Konrad Adenauer, L-1115 Luxembourg or on www.Xtrackers.com

Xtrackers is an undertaking for collective investment in transferable securities (UCITS) in accordance with the applicable laws and regulations and set up as open-ended investment company with variable capital and segregated liability amongst its respective compartments.

DWS Investment S.A. acts as the management company of Xtrackers, Xtrackers II and Xtrackers (IE) plc.