{kind=link}

As an investment platform we serve thousands of different investors with myriad different strategies. We have clients that take a global approach to portfolio construction, those that prefer to base their decisions on certain sectors, people who prefer to invest closer to home and those that like to take on more risk in their investments.

One strategy we do occasionally see is that of concentrating investments within a single ETF, sector or geography. We believe, fundamentally, that this comes with notable risks when compared with a portfolio that’s diversified across different regions, which we want to be sure that our DIY investors are aware of.

In this deep dive, we’ve outlined several benefits to adopting a more global approach to investing, as well as how InvestEngine may be able to help improve your portfolio.

1. One country’s returns can be poor

When investing in a single country’s stock market, investors run the risk of the chosen country performing worse than a more globally diversified portfolio. Sometimes this underperformance can be severe and prolonged.

For example, research from Deutsche Bank showed that three members of the G7 group of leading industrialised nations, Italy, Germany and Japan, saw returns from equities worse than those of government bonds over a fifty year period from 1962.

The Italian stock market even managed to deliver a negative real return over those 50 years, at -0.38% on an annualised basis, versus +2.64% for bonds. In Japan, government bonds delivered a real return of 4.17% a year, beating the 2.72% of equities. While in Germany bonds returned 4.28% versus 3.46% for equities.

By limiting investments to one country, this increases the chances an investor’s portfolio suffers the same returns of Italy, Japan, or Germany.

We might reasonably believe the UK market is always likely to avoid a long period of stagnation – the UK is a well-developed market, has a strong economy, corporate governance, regulations, and relatively free movement of labour and capital.

But this is a risk investors do not need to take. Portfolios holding securities from many different countries reduce the impact of any single country’s poor performance on the portfolio as a whole, which reduces the portfolio’s risk.

Not only does global diversification reduce a portfolio’s vulnerability to any single country’s poor returns, it also reduces dependence on any single sector, which can further boost the risk-return profile of a portfolio

2. Sector concentration can be risky

One of the reasons the FTSE 100 has performed well in 2022 is due to its relatively large exposure to energy companies.

As of October 2022, the energy sector now constitutes 16% of the index, with even larger weightings to financials and consumer staples companies. These weightings, particularly in energy and consumer staples, are significantly higher than would be found in a more globally diversified portfolio.

By investing in only the UK – or in any single country – investors are taking the view that the sectors which have the highest weighting in that country’s local index are likely to outperform going forwards.

No single sector has generated consistently strong performance. Technology might be the exception to this rule, having spent more time towards the top of the chart over the last 10 calendar years, but has performed famously poorly this year. Conversely, the energy sector spent most of its time languishing as the worst performing sector of the last 10 years, only to become the top performing sector in 2021 and 2022.

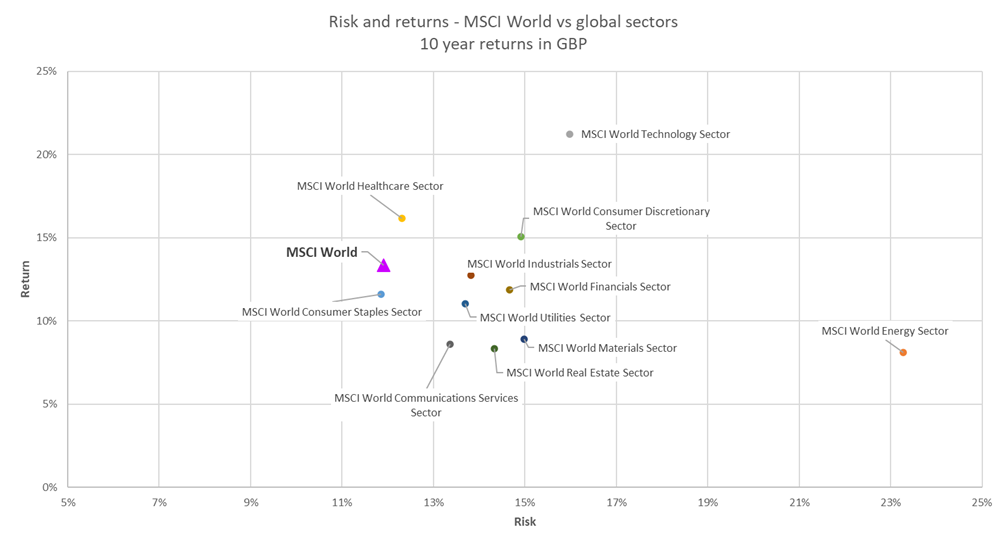

Less intuitively, and more interestingly, the MSCI World (used a proxy for a globally diversified portfolio) ended up as the fourth best performer – despite only having spent one year as a top four best performer. The index spent most of its time towards the middle of the pack – never being a top performer, but never being the worst, either. When these consistent returns were compounded over 10 years, the index ended up being one of the best performers compared to its constituent sectors.

There are theoretical reasons why a low dispersion of returns is attractive for investors – predominantly because it reduces what’s known as the “volatility drag”. Investors want to avoid large gains and large losses, as the losses require disproportionately larger gains to recover from.

And not only did holding a more diversified portfolio of sectors provide strong returns, but being diversified by sector meant that holders of the global index managed to avoid the more extreme losses incurred by investing in any single sector – never losing more than 5% in a calendar year, compared to some significant double-digit losses from individual sectors.

Looking at the volatility of returns, the power of diversification becomes even more apparent.

The chart below shows that by combining each individual sector together into the global index, the MSCI World itself has a lower level of risk than almost every single one of its constituent sectors:

By combining sectors with higher levels of volatility together, the risk of the overall portfolio is reduced.

Not only does being diversified by sector result in lower risk, but the more diversified portfolio’s returns are also higher than the majority of any individual sector, resulting in an extremely attractive risk/return profile.

3. Only a few stocks generate most of the returns

Investing in only a single country will affect portfolio returns.

Occasionally this may work in the investor’s favour – the FTSE 100, for example, has outperformed the global index this year thanks to its high exposure to energy stocks.

But the more concentrated a portfolio is, the higher the variance in long-term returns is likely to be.

Investors in concentrated portfolios may outperform the market as a result of their concentration, but they also have a higher chance of underperforming too – and the more concentrated the portfolio, the more extreme the outcome is likely to be.

To help anchor investors’ expectations on how likely it is investors will achieve consistent long-term outperformance, S&P Dow Jones Indices release a semi-annual ‘Persistence Scorecard’, which tracks the degree to which historical relative performance predicts future relative performance.

The Persistence Scorecard shows that regardless of asset class or style focus, active management outperformance is typically short-lived, with few funds consistently outranking their peers or benchmarks. For example, of the top-quartile performing domestic US funds in 2017, only 1.66% remained top-quartile at the end of 2021.

These results suggest that generating consistent long-term outperformance is incredibly rare, implying that the longer investors hold concentrated portfolios, the less likely they are to outperform a more diversified portfolio over the longer term.

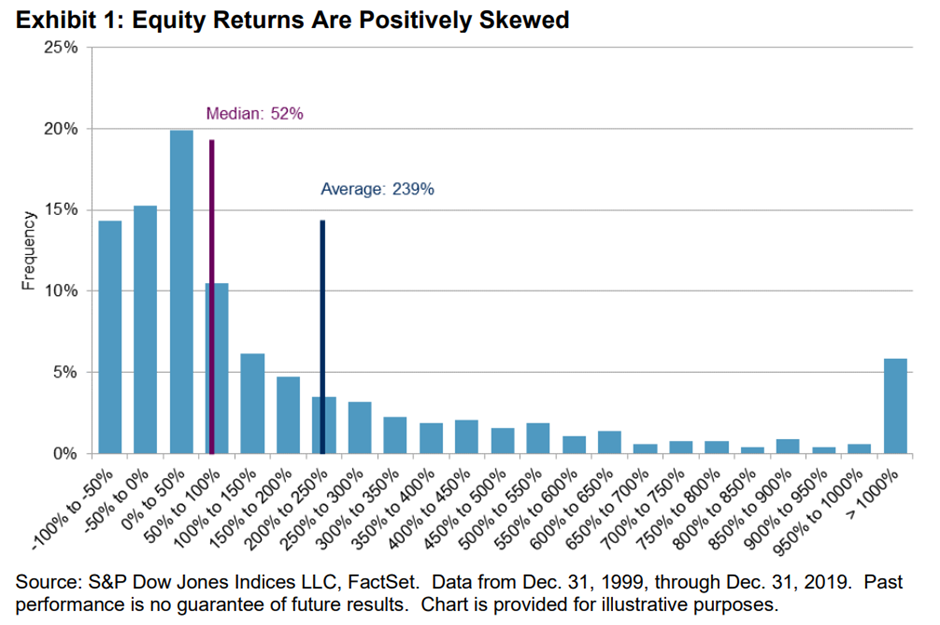

One reason why more concentrated portfolios are less likely to outperform in the long run is due to something known as “positive skew”. When looking at stock market returns, researchers have found that the vast majority of gains are generated by a small minority of stocks over the long-run.

This chart, from S&P Dow Jones Indices LLC, shows that while the median stock in the S&P 500 appreciated only 52% in the 20 years to 31/12/2019, the average stock returned 239%.

This is because very few stocks (just over 5%) generated returns of over 1,000%, which dragged the average – and the index – up. The difference between the median return and the average (mean) return shows the difference in returns investors would have achieved had they failed to own those very few stocks which drove the index up.

This feature of stock market returns occurs because the most a stock can ever lose is 100%, but its upside is potentially unlimited. This means the gains from the largest winners will more than compensate for the losses among the largest losers. Compounding increases this positive skewness over time, as the returns from the biggest winners continue to outpace the losses from the losers, meaning the longer an investor’s time horizon is, the more skewness will affect returns.

This finding that equity returns are positively skewed has been replicated many times:

· A famous academic paper has shown that since 1990, only 1.3% of stocks created 99% of global wealth.

· According to JP Morgan research, more than 40% of companies that were ever in the Russell 3000 Index experienced a 70% decline which was not recovered.

· According to Vanguard research, between 1987 and 2017, 47% of stocks were unprofitable investments, almost 30% lost half their value, but 7% had cumulative returns of over 1,000%.

Because investors with more concentrated portfolios are less likely to own the few stocks which generate the majority of the gains, the longer such concentrated portfolios are held, the less likely it is they will keep up with the more global diversified portfolio which does hold these long-term winners.

So global diversification helps in two ways:

- It reduces the dispersion in terminal wealth compared to more concentrated portfolios. This reduces the risk of an investor suffering an unlucky series of returns and experiencing more severe long-term underperformance.

- It allows an investor’s portfolio to participate in the few stocks which drive the majority of market gains – wherever in the world they happen to be located. Given the compounding effect that positive skew can have on returns, being globally diversified is especially important for investors with long time horizons.

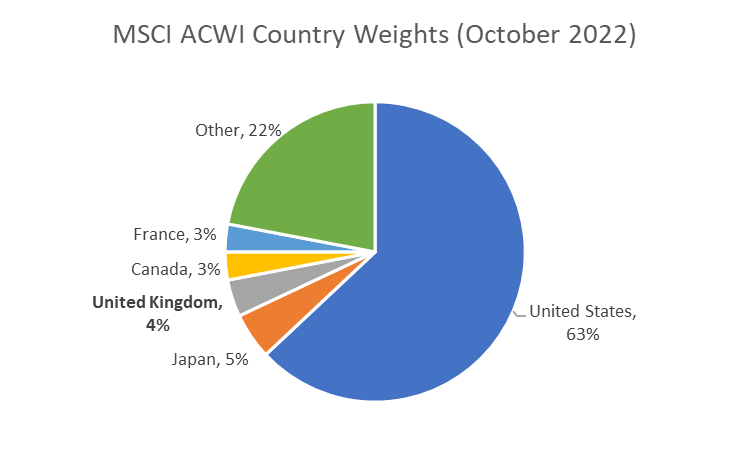

4. The UK is just 4% of the global market

It’s easy to overestimate the relative size of the UK economy given how exposed UK investors are to domestic companies.

But it’s worth remembering that relative to the rest of the world’s markets, the UK makes up only 4% of the global market:

This is relevant for investors, because it relates to an investing theory known as the Efficient Market Hypothesis (EMH).

The EMH states that asset prices reflect all available information. The theory goes that it is therefore impossible to consistently outperform the market on a risk-adjusted basis, since market prices already incorporate all information relevant to an asset’s price.

In reality, while markets are not perfectly efficient, they are still highly efficient. They are at least efficient enough that the vast majority of those who attempt to outperform fail.

For example, the S&P Dow Jones ‘SPIVA’ report for mid-year 2022 indicates that over 80% of GBP-denominated UK equity funds underperformed their benchmarks on a risk-adjusted basis over the last 20 years, as did 97% of domestic US equity funds.

Using this assumption of highly (but not perfectly) efficient markets, it follows that investors quickly take advantage of any mis-pricings, and therefore all risky assets should have similar risk-adjusted returns.

If all assets have similar risk-adjusted returns, then investors should seek broad global diversification across many risky assets – a useful starting point for which is a globally diversified portfolio, with countries and securities weighted in proportion to their relative market values.

By only investing in UK companies, this is a substantial deviation away from a globally diversified portfolio for an investor. The investor is taking a significant bet that those companies listed in the UK will outperform those based in other countries, implying that they are more informed than the highly-efficient multi-trillion pound global financial markets, and have a sizeable edge over other market participants.

Traditional financial theory states that deviations from the market portfolio should be sized according to the level of confidence an investor has in their edge over the market. Having such an extreme overweight by investing only in a single country implies an exceptionally high level of confidence, and given the low success rate of professional active managers at outperforming the market, investors should be wary of taking such extreme positions.

5. Globalisation is increasing

International trade is becoming increasingly globalised, driven by free trade organisations such as NAFTA and the World Trade Organisation. Lower tariffs on imported goods, the global expansion of supply chains, and the Internet have all contributed to increasing levels of global trade. As a result, it now matters less and less where a company is listed, with more companies able to do business all over the world.

Looking at some of the largest companies listed in North America, for example: Apple generates 57% of its revenues from outside the US, Microsoft generates 50%, Alphabet 54%, and Exxon Mobil 62%. Similarly in the UK, 82% of the FTSE 100’s revenues are generated from outside the UK.

Given that companies manufacture, trade, and sell goods all over the world, where a company chooses to base itself is becoming increasingly irrelevant.

When deciding whether to invest in a single geographic market or to invest globally, investors must consider whether there is a good reason to exclude from their portfolio all those overseas-based global companies which buy from and sell to all the same individuals and companies as those based in a single country.

Because the country of geographical listing is becoming less relevant, there is little downside to owning as many companies from as many countries as possible. Maximising geographic diversification is particularly important for investors to consider given how easy it is to access a professionally managed diversified portfolio.

How we can help

As a quick recap, increasing diversification through adopting a more global approach can improve a portfolio in several ways:

- Global investors are not overly exposed to any single country, mitigating the effects of one market experiencing a particularly poor period of performance, and reducing a portfolio’s risk.

- Similarly, it reduces a portfolio’s exposure to any single sector, which helps reduce the frequency, magnitude, and length of large sector-specific drawdowns, further reducing risk.

- Global diversification also reduces the dispersion in terminal wealth compared to more concentrated portfolios, reducing the risk of an investor experiencing more severe long-term underperformance.

- It helps the portfolio increase returns, by exposing the portfolio to the very few stocks which drive the majority of market returns, regardless of where they are located.

- It keeps the portfolio aligned with financial theory, by keeping country weightings in line with the highly-efficient market portfolio, and maximizing diversification across many risky assets.

Our InvestEngine managed portfolios are built using Modern Portfolio Theory, which suggests that diversification helps to deliver a better relationship between the risk taken and the return received. On that basis, our portfolios invest in thousands of companies across hundreds of countries.

Not only are our portfolios diversified by country, but we ensure portfolios are also balanced by industry, asset class, and currency. We also diversify beyond a global index-tracking approach by including exposure to other risk factors, such as the size and value factors, to help further enhance portfolio risk-adjusted returns.

To ensure your InvestEngine portfolio is right for you, we offer a free risk-profiling service, which means your portfolio will be tailored to suit your own circumstances and needs.

If you would like to learn more about our managed portfolios, please click here.