{kind=link}

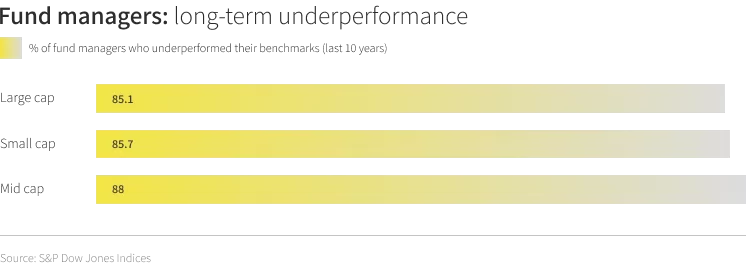

According to data published by S&P Dow Jones, over the last 10 years, the vast majority of large-cap, mid-cap, and small-cap investment fund managers have underperformed their respective benchmarks.[1] To us at Tematica, this raises a very logical question – when it comes to investing, particularly sector-based investing, if one chooses to follow the herd, how does one expect to outperform the herd?

Famed management consultant, Peter Drucker, sums it up rather eloquently, “If you want something new, you have to stop doing something old”[1]. Or, as hockey legend Wayne Gretzky would say, “I skate to where the puck is going to be, not to where it has been.”[2]

The quote speaks to the heart of thematic investing, which not only allows one to focus on the structural changes that will play out over the longer-term, shaping and altering competitive landscapes, but also to look past short-term market or sector noise and uncertainties. By identifying companies poised to benefit from evolving thematic tailwinds, investors can take advantage of opportunities while sidestepping the risks associated with companies whose business models are being impacted by thematic headwinds.

“You need to divorce your mind from the crowd. The herd mentality causes all these IQ’s to become paralyzed.”[3] – Warren Buffet

What is thematic investing?

Thematic investing focuses on structural changes emanating from the shifting global landscape of economics, demographics, technology, and psychographics and from time to time regulatory mandates. These structural changes alter consumer and company behaviour and therefore spending in one form or another. That sea change in spending gives rise to thematic tailwinds that power the businesses of companies that have identified and positioned themselves to ride those tailwinds, either organically or through M&A.

Companies that capture incremental revenue, profits and cash flow stemming from these structural changes tend to be rewarded with expanding valuation multiples over time. In the lexicon of the investing world, thematic investing identifies the causality of alpha.

Further, because thematic investing isn’t rooted in sector-based classification schema, it isn’t trapped in antiquated thinking. Often, such thinking incorrectly categorises a company’s business or finds itself falling behind, as new technologies, products and services come to market and disrupt existing business models. Rather than a vertical, siloed approach, thematic investing is a horizontally-focused strategy that cuts across sectors and geographies to identify companies that are best positioned to capitalise on long-term catalysts.

For example, while Amazon (AMZN) is widely thought of as a disruptive powerhouse in retail when examining the company’s business, the driver of its profits is actually its cloud business.[5] From a sector perspective, online food ordering and delivery company GrubHub (GRUB) is an internet company, but it – along with Door Dash, Postmates and similar businesses – are upending the restaurant industry.[6] Uber (UBER) and Lyft (LYFT) fall into the Industrials sector, but their businesses are putting pressure on automotive demand, hitting Ford (F), General Motors (GM), and Honda Motor (HMC), as well as on the re-sale value for used cars at CarMax (KMX).[7]

This evolving and forward-looking investment approach helps investors position themselves for changes associated with the development of new technologies, business model disruption, and demographics reshaping the needs and preferences of the world’s population.

Why should investors go thematic?

Thematic investing allows investors to focus on the structural changes or themes that will play out over the longer-term, shaping and altering competitive landscapes, but also to look past short-term market or sector noise and uncertainties. Themes have three defining characteristics that makes it appealing to the ordinary investor:

- They offer recognizable signals that make them digestible, recognizable and relatable to investors, and helps them to make investing decisions based on things they know and can observe.

- They can help insulate a person’s overall investment portfolio, as they sidestep investments in funds and companies that are vulnerable to the changing landscapes ahead of them.

- The combination of multiple themes blowing on a company’s business, compared to a lone one, allows well-positioned companies to capture incremental revenue and profits at an even faster rate.

How is thematic investing different from sector-based investing?

There are major challenges associated with grouping companies based on sector classification. Even S&P Dow Jones is realising the shortcoming to be had with that framework, and recently rolled out its largest revision to the Global Industry Classification Standard (GICS) since 1999. S&P Dow Jones now classifies thousands of companies across not 10 but 11 sectors.[8] While there have been strides of late to update sector classifications, the reality is that these strides have built on already dated schema, and are nothing more than band-aids. At best, these changes are likely to become outdated yet again, and at worst, further complicate matters for investors.

For example, let’s take a look at how sector investing thinks about various companies found in its newest created sector – Communications Services. There are the usual suspects that one would think of when contemplating communications services – cable companies, such as Comcast Communications (CMCSA) and Charter Communications (CHTR), as well as mobile telephony companies like Verizon (VZ) and AT&T (T). But the sector classification also includes Walt Disney (DIS), which while it does compete with the content business at Comcast Corp. (CMCSA), doesn’t have a cable, mobile network or other communications business. And while AT&T has been historically a communications focused business, its acquisition of the WarnerMedia business has dramatically altered its business mix and product strategy. How does the Communications Sector view account for that? There are other head scratchers such as gaming companies Activision Blizzard (ATVI) and Take-Two (TTWO) which are consuming network data with linked, multiplayer games, and so would they not be far more gaming and content companies, versus communication services companies?

And so on…the shortcomings expose the flaws with a system that groups companies based on predetermined sectors. Inherent in this sector-based classification schema is the idea that companies don’t change their business models, but as we’ve witnessed over the years, that tends not to be the case.

Mobile infrastructure company, Nokia (NOK), originally started as a boot company, and now it is the second-largest holder of 5G contracts.[9] Apple originally started as a personal computer company, but today its lion’s share of sales and profits come from the iPhone and its Services business, which did not exist 12 years ago.[10] Amazon started off selling books, records, and similar items, but has continued to add to its business model and today is delivering all sorts of products and services that are a long way off from that original book-based business.

Take, for example Amazon Web Services, or its acquisition of online pharmacy PillPack, or the rollout of its Amazon Go stores that employ technology that could change the retail shopping experience entirely. Then there is Amazon’s Prime Video offering that stream TV shows, movies, original content and NFL games, it’s Prime music service, as well as its Whole Foods business. And then there is its Alexa/Echo digital assistant business that is moving beyond smart speakers to being incorporated into appliances, cars and home security devices.[11] Is Amazon a Consumer Discretionary company like the Gap (GPS) or American Eagle (AEO)? Is it a Communications Services company like Walt Disney (DIS) and CBS (CBS)? Is it a Consumer Staples company like Kroger (KR) or Costco (COST)? Or is it an Information Technology company like Cloudera (CLDR) and IBM (IBM)?

We could continue but it is rather apparent that trying to shoehorn companies into predetermined lists of sectors isn’t always easy, and increasingly this process fails to properly reflect the true nature of a company’s business. Viewing the market through a sector lens fails to capture the real-world tailwinds and catalysts that are driving structural changes inside industries. These nuances are far better captured in thematic investing, which focuses on those changing landscapes and the tailwinds as well as headwinds that arise and are driving not just sales but operating profit inside of companies.

At Tematica, we came to this point of view after decades in equity research analysing countries, sectors, and companies on Wall Street. We realised that sector-focused thinking leads to investing with blinders on. We realised that the traditional approach failed to identify and understand the underpinnings of why certain companies do well over the long-term, while others don’t.

What is the difference between a trend/fad and thematic investing?

Generally speaking, trend or fad investing is a strategy that aims to capitalise on rising sales and profits from a short-lived phenomenon. We see these all the time in the apparel industry where new styles achieve short-lived popularity but fade away not long after. That “fade” is indeed what coined the term “fad”. While trend investing can be profitable for an investor, the challenge is in correctly timing one’s entry and exit to maximise profits. Stay in too long, and an investor risks seeing his or her profits shrink, if not evaporate as the trend fades away.

Because thematic investing focuses on evolving structural changes, the duration of a theme is not measured in weeks or months, but over multiple years. Initially, a structural change may have a modest impact, but over time as those changes unpack themselves, the impact becomes increasingly pronounced. Evolving technology and changing psychographics as well as demographics also have a role to play in the velocity of that structural change.

For example, the current growth of the US population aged 65 and older that is being driven by the baby boom generation is unprecedented. As they have passed through each major stage of life, baby boomers have brought with them both challenges and opportunities to the economy, infrastructure and institutions. As baby boomers continues to age over the coming 20-year period, we will see wide changes in the demand for housing, healthcare and financial services, just to name a few areas.

Can investment themes overlap?

The only thing better than one investment theme blowing on a company’s business is multiple themes doing so. We at Tematica recognize that several of our themes are complementary in nature, due in part to evolving technology, products and services. For example, aspects of our Aging of the Population investing theme are beneficiaries of the several tailwinds associated with our Digital Lifestyle investing theme, which allows goods and services to be delivered to one’s ageing parents. While older folks may not be ones to incorporate virtual reality into their lives, other aspects of our Disruptive Innovators investing theme such as autonomous cars and telemedicine are prime candidates for older citizens. As consumers and businesses wade deeper into the digital world as part of our Digital Lifestyle investing theme, the growing number of connected devices opens the door for cyberattacks and privacy violations that are at the core of our Cyber Privacy investing theme.

The combination of multiple tailwinds offers a greater tailwind velocity to a company’s business compared to a lone one, which should allow a well-positioned company to capture incremental revenue and profits at an even faster rate. Research from McKinsey & Company confirms this view, “In our experience, the most attractive opportunities are found when multiple themes converge and reinforce one another.”[12]

Is thematic investing a black box strategy or is it relatable and recognizable to all investors?

More often than not, most people tend to have their eyes glaze over when confronted with complex strategies and intricate investing algorithms that they don’t understand. The work of organisational psychologist Peg Neuhauser has shown that learning that stems from a well-told story is remembered more accurately, and for far longer, than learning derived from facts and figures.[13] The narrative-like nature of themes, combined with real-world signposts that serve as proof points for investors are silver linings for people that invest thematically. The digestible, recognizable and relatable nature of themes resonates with ordinary investors, and helps them make investing decisions based on things they know and can observe.

“Invest in what you know.”[14] – Peter Lynch

Can thematic investing help reduce portfolio risk?

Thematic investing can help insulate a person’s overall investment portfolio as it side-steps investments in funds and companies that are vulnerable to the changing landscapes ahead of them. While thematic tailwinds can power a company’s business, hitting thematic headwinds, such as the shifting consumer preference for healthier food, snacks, and beverages, can weigh on-demand drivers for a company’s business should it fail to adapt its product and service offering

Conclusion

We believe it’s time that investors stop following the sector-focused Wall Street herd, and embrace thematic investing to capture the rewards and alpha generation this type of investing offers. As with all investment strategies, success with a thematic approach ultimately comes down to the underlying principle of investing: identifying which securities within an emerging theme are mispriced or undervalued relative to the business opportunities ahead, and which are presenting themselves through a theme. The process requires nuance, and deep sectoral expertise to successfully identify the most likely winners with a high degree of conviction. Our thematic approach provides a forward-looking, longer-term lens to making these kinds of investment decisions, and helps investors to seek long-term outcomes that allow them to unambiguously express the views about the future.

Educational content produced as part of a paid partnership

References

CNBC, “Active fund managers trail the S&P 500 for the ninth year in a row in triumph for indexing”, 2019. Available at https://www.cnbc.com/2019/03/15/active-fund-managers-trail-the-sp-500-for-the-ninth-year-in-a-row-in-triumph-for-indexing.html

Medium, ““If you want something new, you have to stop doing something old”, 2018. Available at https://medium.com/@debsofield/if-you-want-something-new-you-have-to-stop-doing-something-old-peter-f-drucker-3ae509605b4f

Digital Realty. “Skate to Where the Puck is Going – Position for the Future to Achieve a Competitive Edge”, 2016. Available at https://www.digitalrealty.com/blog/skate-to-where-the-puck-is-going-position-for-the-future-to-achieve-a-competitive-edge

Investing Daily, “What The Investment Herd Is Missing”, 2019. Available at https://www.investingdaily.com/51832/what-the-investment-herd-is-missing/

Amazon, “Amazon.com Announces Third Quarter Sales up 24% to $70.0 Billion”, 2019. Available at https://ir.aboutamazon.com/news-releases/news-release-details/amazoncom-announces-third-quarter-sales-24-700-billion

DoorDash, “The Restaurant Industry Has Gotten Even More Competitive–Here’s How to Survive”, 2019. Available at https://get.doordash.com/the-restaurant-industry-has-gotten-even-more-competitive-heres-how-to-survive

The Detroit News, “Used-car price tumble spells trouble for the U.S. auto market”, 2019. Available at https://www.detroitnews.com/story/business/autos/2019/10/10/used-car-price-tumble-spells-trouble-us-auto-market/40294195/

S&P Dow Jones Indices, “S&P Dow Jones Indices and MSCI Announce Select List Of Companies Changing Due To Revisions To The GICs® Structure In 2018”, 2018. Available at https://www.msci.com/documents/10199/238444/GICS+Press+Release+Jan+2018.pdf/dd19f706-a28c-48a1-b940-88254bb91581

Fierce Wireless, “Which vendor leads in 5G contracts?”, 2019. Available at https://www.fiercewireless.com/5g/which-vendor-leads-5g-contracts

Apple, “Apple Reinvents the Phone with iPhone”, 2007. Available at https://www.apple.com/newsroom/2007/01/09Apple-Reinvents-the-Phone-with-iPhone/

TechCrunch, “Echo Auto brings Alexa to cars”, 2018. Available at https://techcrunch.com/2018/09/20/echo-auto-brings-alexa-to-cars/

McKinsey & Company, “From indexes to insights: The rise of thematic investing”, 2014. Available at https://www.mckinsey.com/industries/private-equity-and-principal-investors/our-insights/from-indexes-to-insights-the-rise-of-thematic-investing

Harvard Business Publishing, “What Makes Storytelling So Effective For Learning?”, 2017. Available at https://www.harvardbusiness.org/what-makes-storytelling-so-effective-for-learning/

Equities.com, “5 Time-tested Lessons from Peter Lynch’s One Up on Wall Street.”, 2018. Available at https://www.equities.com/news/5-time-tested-lessons-from-peter-lynch-s-one-up-on-wall-street

This Featured Article has been produced by Tematica Research LLC. Rize ETF Ltd make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability or suitability of the information contained in this article.

Important information

Capital at risk. The value of your portfolio with InvestEngine can go down as well as up and you may get back less than you invest. ETF costs also apply.

This communication is provided for general information only and should not be construed as advice. If in doubt you may wish to consult a professional adviser for guidance.

Tax treatment depends on personal circumstances and is subject to change, and past performance is not a reliable indicator of future returns.