{kind=link}

With 2023 now behind us, we can turn our attention to our outlook for the coming year.

Our investment philosophy is focused on the long-term, meaning you won’t find us making any predictions for 2024 asset class performance, or providing S&P price targets. Because our asset allocation is based on long-term return data, we have no need to gaze into the unreliable crystal-ball of forward 12 month returns.

Our aim is to remain a safe pair of hands for your capital, and to generate attractive risk-adjusted returns over multiple decades. Our philosophy is therefore based on peer-reviewed, academic evidence which has been validated through real-world results. We don’t indulge in short-term market calls.

For an overview of the top stories in 2023 from our investments team, click the button below.

What will our managed portfolios look like in 2024?

Heading into 2024, we will continue to offer low cost, long-term portfolios with low minimum investments and market-leading analytics. Our investment approach will still focus on providing excellent value for money, and our ability to improve our service, both for managed and DIY account holders, will only improve as we continue to scale as a business.

In terms of portfolio construction, we remain committed to our approach outlined in our investment philosophy document. As one of the primary determinants of how well a fund performs versus its benchmark is the fees it charges, we will continue to hold low-cost index tracking funds as our vehicle of choice. Within equities, we diversify away from pure market beta by introducing other sources of risk (known as ‘factors’) – which are designed not only to improve long-term risk adjusted returns through the diversification benefit they provide, but also to reduce the distribution of terminal wealth outcomes and minimise the impact of luck in final portfolio values.

Within bonds, we continue to hold only the highest quality government bonds in portfolios, to provide maximum safety in the event of a market drawdown. Following on from the discussion on duration above, we maintain a preference for shorter-duration bonds, to minimise the potential for large bond drawdowns which clients may not expect in the safe segment of their portfolios (as many longer-duration bond holders experienced to their chagrin during 2022).

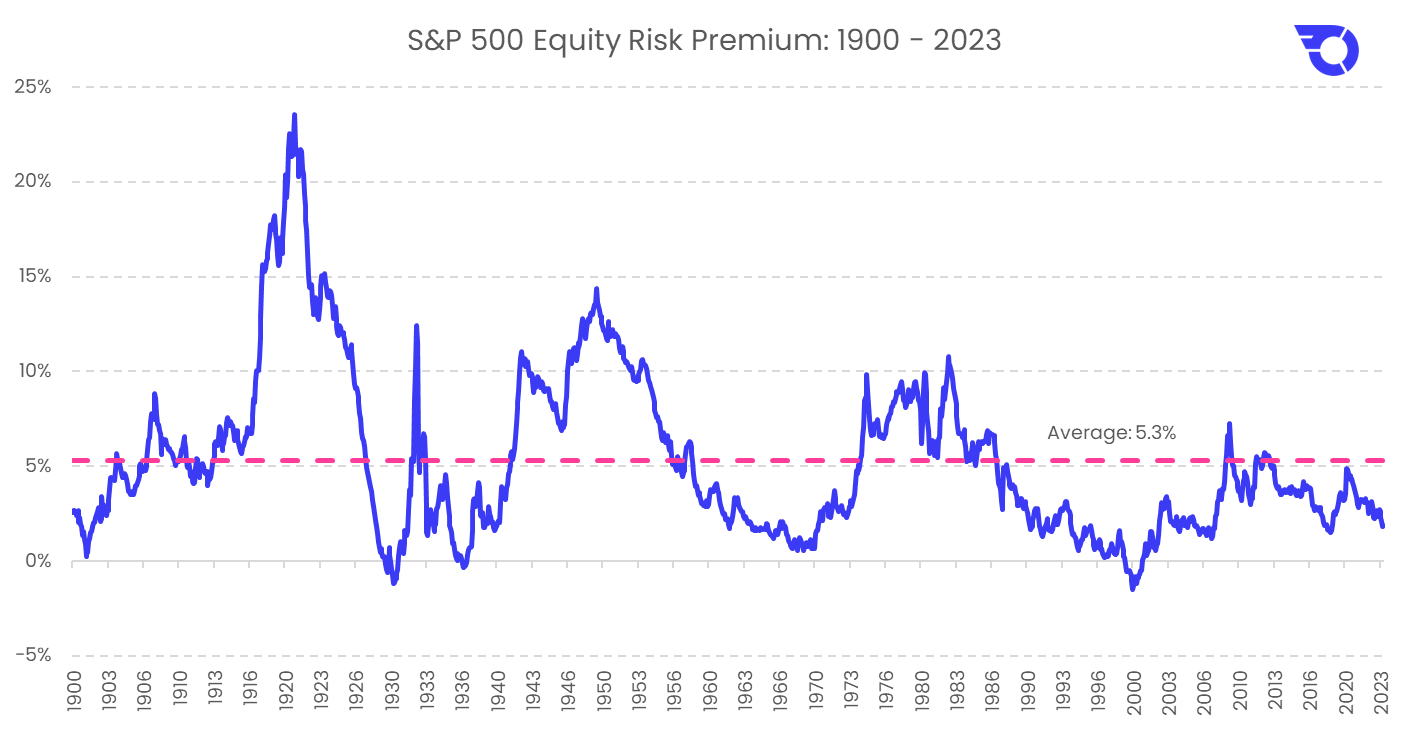

Because bond yields are currently much higher than they’ve been in the recent past, and because bond returns are so highly correlated with their starting yield (particularly for government bonds), their expected returns are now also much higher. With equity market valuations verging on the higher side of their historical averages, this reduces their longer-term expected returns (although this relationship is far less certain than when looking at bonds). The result is the expected additional return for owning stocks compared to owning bonds, also known as the ‘Equity Risk Premium (ERP), now being lower than average, making bonds more attractive relative to stocks.

This analysis is crude, and subject to many estimation errors and variations in calculation methods, but nonetheless does a good job of illustrating the point that bonds are now providing better competition for equities than at any point over the past fifteen years.

As a result of our internal quantitative mean-variance optimisation analysis, which considers the long-term expected returns, risk, and correlations of all our asset classes, we have a slight overweight to bonds over stocks in portfolios.

With the preponderance of returns being generated by so few stocks this year, from a qualitative basis this gives us comfort that we will be more defensively positioned should any pullback occur – although this qualitative judgement did not affect our asset allocation decisions. (We aim to remove as much human judgement from the investment process as possible, given how fallible even us investment professionals are to behavioural biases.)

So our portfolios in 2024 will look much the same as they did in 2023. Low cost, simple, diversified, transparent, liquid, and not reliant on macroeconomic forecasting, market timing, or stockpicking.

To wrap things up, I’d like to end on a note of thanks to you, our clients.

Firstly, thank you for entrusting us with your capital. Managing your wealth is not a responsibility we take lightly, and we hope you remain pleased with the service we offer. Thank you for the invaluable feedback you provide, which goes to help improve everything we do. And thank you for continuing to spread the word about InvestEngine. Our growth as a business this year has been incredible, and I hope you continue with us on this journey for many years to come.

Important information

Capital at risk. The value of your portfolio with InvestEngine can go down as well as up and you may get back less than you invest. ETF costs also apply.

This communication is provided for general information only and should not be construed as advice. If in doubt you may wish to consult a professional adviser for guidance.

Tax treatment depends on personal circumstances and is subject to change, and past performance is not a reliable indicator of future returns.