{kind=link}

In an historic landslide victory, the Labour party have won an overwhelming majority in the UK general election. The results represent one of the largest swings in British political history, and a crushing defeat for the Conservative Party, losing 250 seats in a worst-ever result for the party.

UK equities have reacted with typical British understatement, and the impact on markets has been limited.

At the time of writing (8:30 a.m.):

- The FTSE 100 index is up 0.3%, while the FTSE 250 – which includes more UK-focused shares – is up just under 1%.

- Bond yields on 2-year and 10-year gilts have both fallen by around 0.5%.

- Sterling is unchanged both against the US dollar and the Euro.

- The path of interest rate movements remains unchanged.

So why has the market not reacted more strongly? Here are 6 reasons:

- It was already priced in.

A Labour majority had been a foregone conclusion in the minds of investors for some time. Polls indicated a 40% share of the vote going into election day versus 21% for the Conservatives, 16% for Reform UK, 11% for the Liberal Democrats, and 6% for the Green Party. The last time the Conservatives were ahead of Labour in the polls was in 2021. Although the announcement of a snap election came as somewhat of a surprise, markets have had plenty of time to digest the idea of a Labour government, and had already adequately reflected the expectation of a Labour win into prices.

- Remembering lettuces.

Economic policies of the major parties were much more aligned compared to the last election. Both Labour and the Conservatives had committed to adhering to current fiscal rules as overseen by the independent Office for Budget Responsibility, avoiding radical economic policy shifts. This consensus reflects the spectre of Liz Truss’ 2022 mini-budget crisis, which still looms large in the collective political memory.

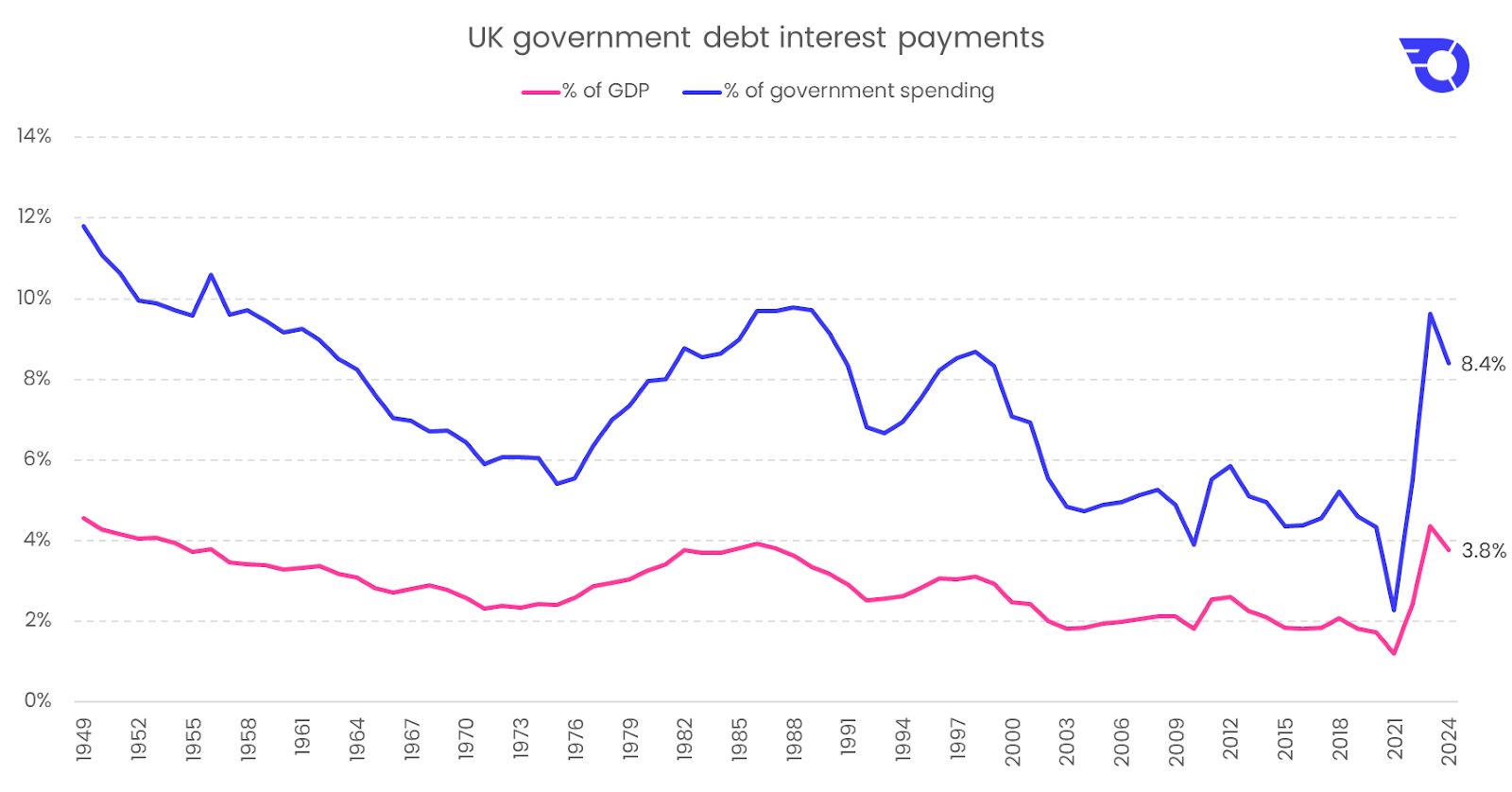

- Either party inherits a high debt burden.

Given the strained public finances and low productivity, significant economic growth remained a challenging goal for any incoming government. The deficit for the last financial year (the difference between what the government raises in taxes minus its spending) was 4.5% of GDP. With total accumulated debt levels now at 98% of GDP, the interest cost of servicing that debt is 8.4% of the government’s spending – the highest level since the late 1990s. This leaves less room for either party to enact meaningful spending policies:

- No Brexit this time.

Unlike the 2019 election, which heavily focused on Brexit, with both sides presenting starkly different options for UK-EU relationships, this election did not involve major EU relationship changes. Both major parties have accepted the existing economic relationship with the EU and are not looking to revisit the Brexit debate.

- The Bank of England is independent.

The Bank of England’s stance remains unaffected by the election. Although owned by the UK government, the Bank has independence in terms of how it carries out its responsibilities – the main of which is keeping inflation stable at its target rate of 2%. Despite recent stubborn core and services inflation data (read more here), headline inflation has reached its 2% target, with overnight index swaps indicating a 64% chance of a rate cut in August and one further cut before the end of the year. The Bank’s independence ensures it’s not swayed by the electoral timetable, and the election’s outcome has had little impact on the path of interest rates.

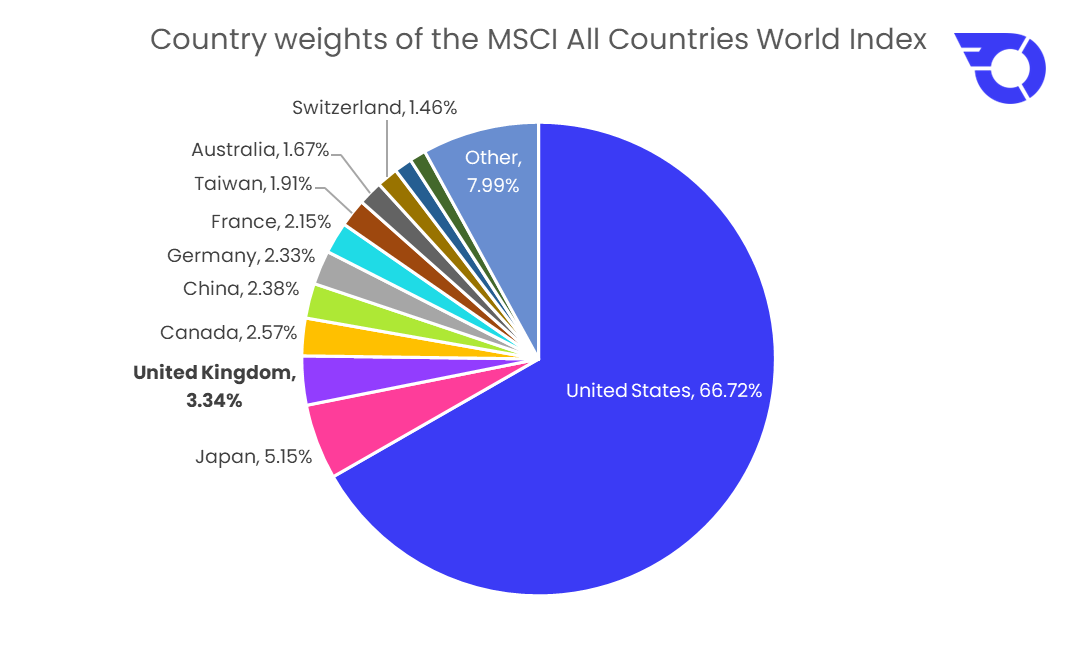

- The UK market is small.

The UK makes up an increasingly small share of the global market. With the UK market at 3% of the MSCI All Countries World Index, even if we’d woken up to large swings in the FTSE this morning, it still would have made little difference to a globally-diversified portfolio:

Source: Bloomberg

—

As ever, the market remains a forward-looking discounting machine. A Labour premiership came as no surprise, and prices had already moved to reflect this most likely outcome. The lack of an extreme market reaction serves as a useful reminder that stock prices already reflect all public information, and price movements are based on changes in expectations for what will happen in the future rather than what’s happening now.

We continue to monitor the risk levels in our managed portfolios, and remain hopeful that markets will sustain the low-volatility, high-return environment investors enjoyed in the first half of this year.

Important information

Capital at risk. The value of your portfolio with InvestEngine can go down as well as up and you may get back less than you invest. ETF costs also apply.

This communication is provided for general information only and should not be construed as advice. If in doubt you may wish to consult a professional adviser for guidance.

Tax treatment depends on personal circumstances and is subject to change, and past performance is not a reliable indicator of future returns.