{kind=link}

2023 was a turbulent year.

We started last year with deadly earthquakes in Turkey and Syria, followed quickly by a US regional banking crisis, an economy-boosting tour from Taylor Swift, the King’s coronation, and panic over the US debt ceiling. And that was all in the first six months.

In June we saw ‘Barbenheimer’ attempting to inject some life into cinema theatres in the midst of a writers’ strike, Trump being indicted (again), and conflict erupting between Hamas and Israel. Throughout the year, interest rates continued to rise, and artificial intelligence (AI) quickly captured the world’s attention, becoming a central theme for investors and businesses.

For the 2023 market roundup, I’ve looked back through all the headlines and selected five of the major stories which affected investors during the year.

For a view on what’s likely to come in 2024, including what’s changed in our portfolios and how we’re positioned for the coming year, follow the link below.

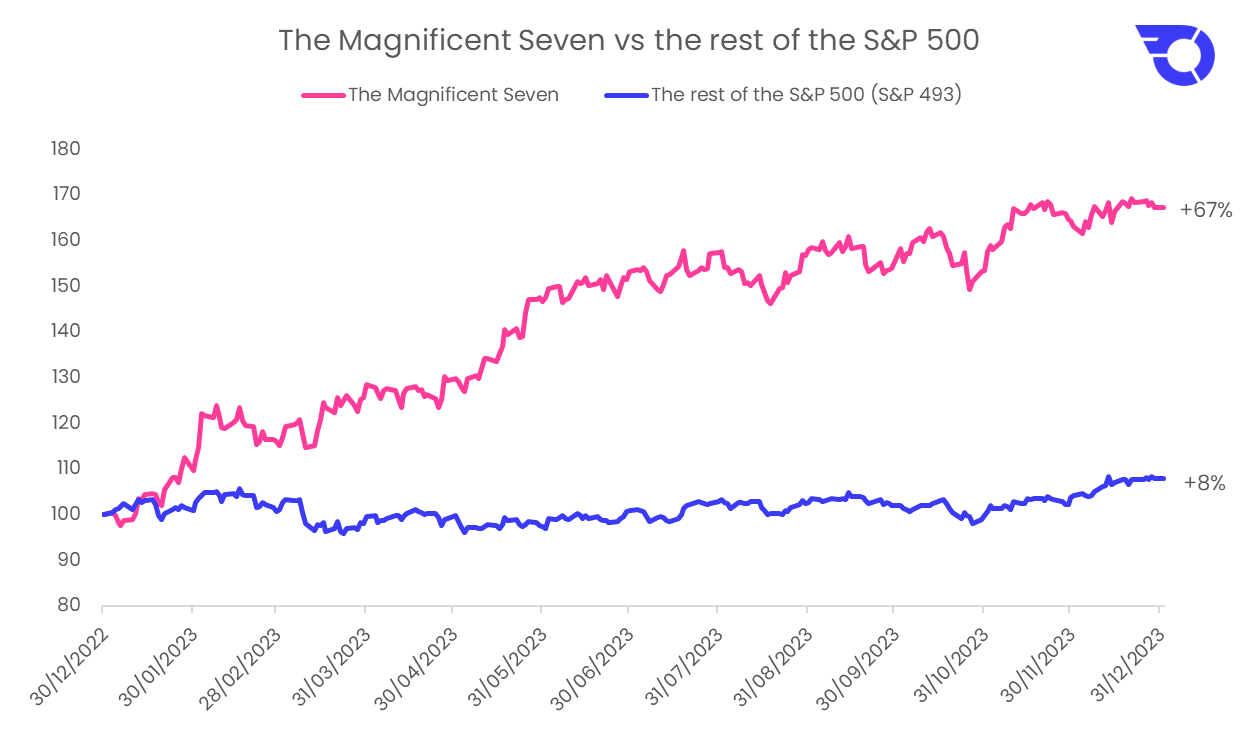

Story 1: The Magnificent Seven

To start with what was by far the most discussed story affecting global equity returns last year: 2023 was the year of the ‘Magnificent Seven’.

These seven companies: Alphabet, Amazon, Apple, Meta Platforms, Microsoft, NVIDIA, and Tesla, all produced stellar returns. Between them they drove equity markets higher, which was especially notable because it was in stark contrast to the rest of the US market which produced decidedly pedestrian returns

This bifurcation between the Magnificent Seven and the rest of the market is shown in the chart below, which visualises the performance of these 7 stocks against the other 493 stocks in the S&P 500. A portfolio of the Magnificent Seven gained almost 70% in 2023, but the rest of the S&P 500 returned only 8%:

These seven’s returns were largely driven by excitement over artificial intelligence technology, with advances in AI creating significant opportunities for the group. The proliferation of AI tools, such as ChatGPT, resulted in AI storming into the public consciousness and brought the technology’s potential to the attention of global investors.

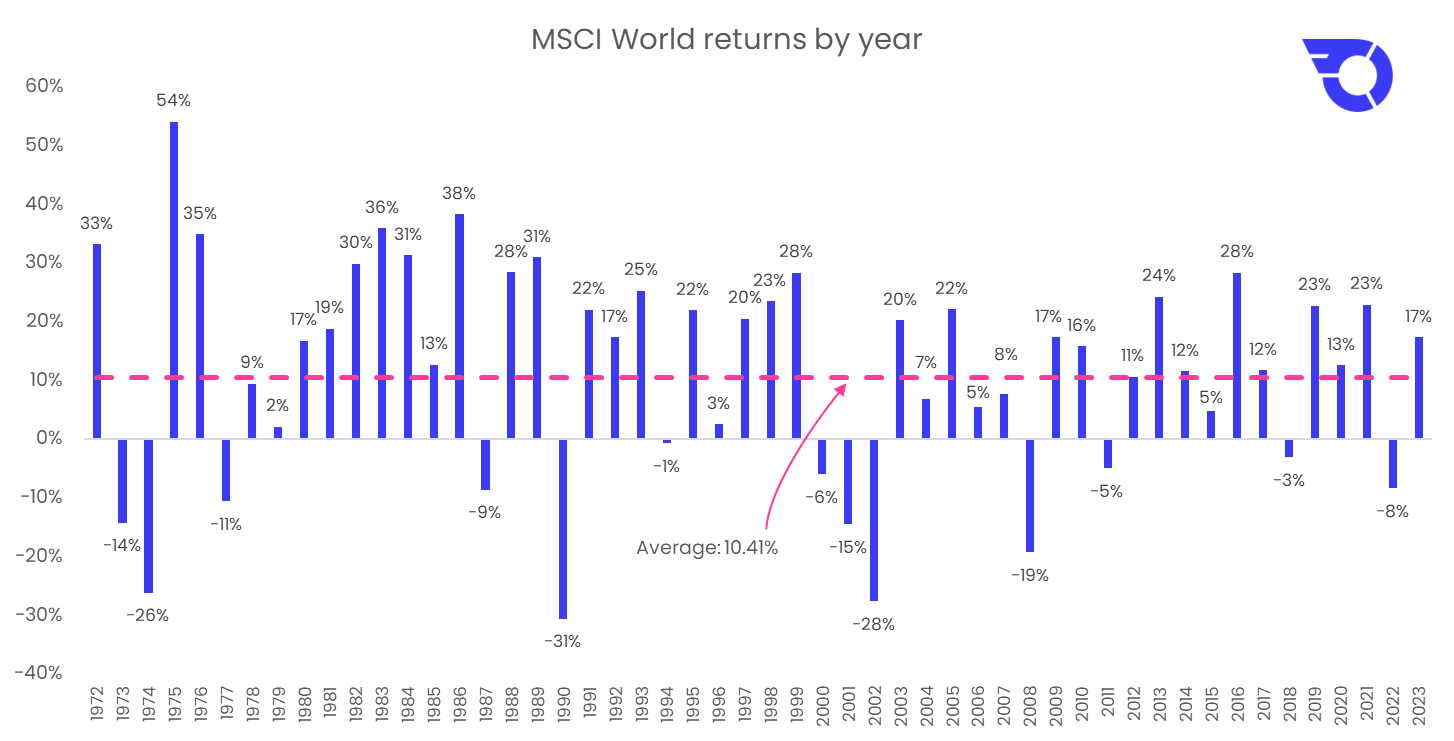

The strength of the Magnificent Seven meant that returns for global markets were higher than average in 2023. But it’s worth remembering – especially after a strong year for markets – that market returns are never average. This is especially true for equity markets, which are more volatile, meaning returns for equity investors are almost always remarkably different to average:

Out of the last 52 calendar years of global market performance, only 9 years have been within 5% of the average market return (either 5% higher or 5% lower) over that time.

So while the Magnificent Seven helped equity markets produce strong returns in 2023, this level of returns should not be relied upon to occur every year, and equity investors should remain prepared for years of drawdown and high volatility.

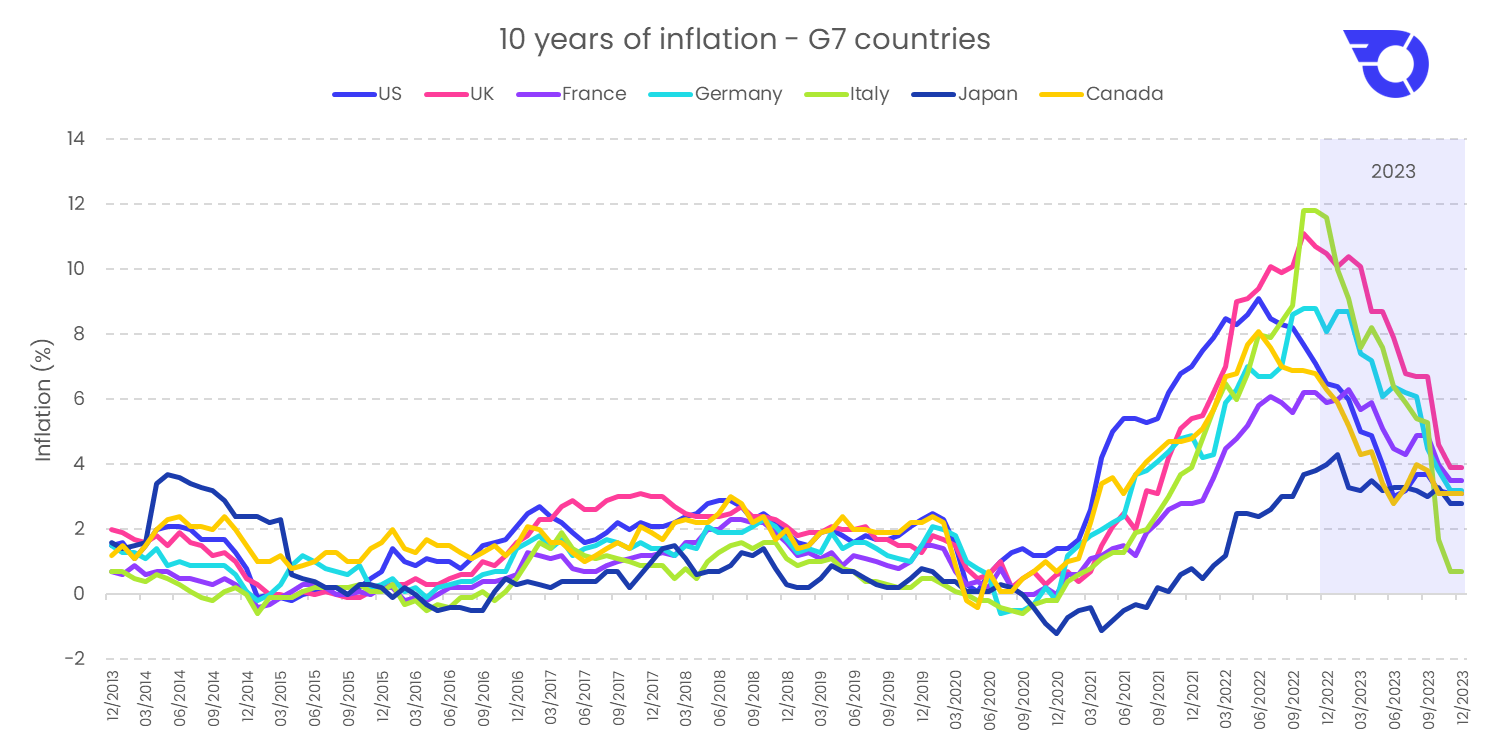

Turning to our second major story of the last year, the market-related story which grabbed the most headlines out of all the stories during 2023 was inflation. Specifically, 2023 can be remembered as the year inflationary pressures finally started to fall.

Story 2: Inflation recedes

Last year saw most countries starting to make headway against the high levels of inflation caused by supply chain disruptions and the COVID pandemic, with the inflation levels of all G7 countries finishing the year lower than when they started:

The UK and Italy saw particularly large declines in the rate of headline inflation, and while other measures of inflation may be proving slightly stickier, the general trend for global inflation seems to be heading lower.

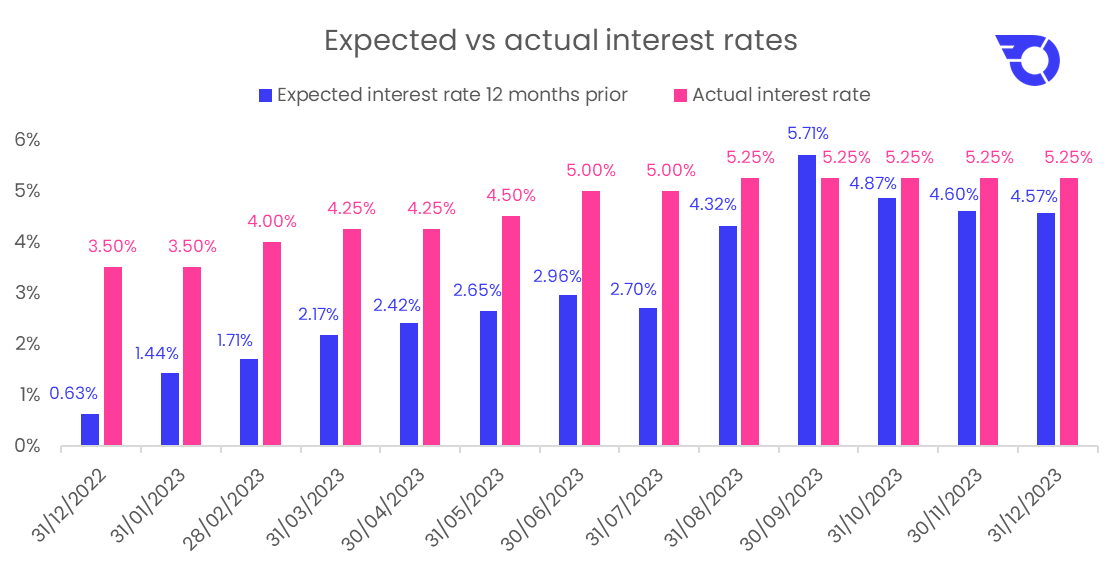

But casting our minds back to 2022, markets didn’t see inflation remaining so high for so long. The narrative at the time, especially among central banks, was that any inflation would be transitory.

We can see this view reflected in what the markets believed interest rates were going to be in 2023, compared to what they actually were. By looking at the interest rates for each month in 2023 versus what the market expected them to be 12 months prior, we can see just how much the market underestimated inflation’s staying power:

The market significantly underestimated how high interest rates were going to rise, especially in the first half of 2022, with actual rates rising 2-3% more than markets expected. A brief period of over-exuberance caused markets to predict rates of over 5.7% in September, before falling back to underestimating their rise by around 0.5%.

While we could never expect rate predictions to be perfect, the degree of difference between expected versus actual rates, especially in the first half of the year, shows just how difficult it is to make accurate market predictions. In the words of physicist Niels Bohr: “It is difficult to make predictions, especially about the future.”

This difficulty of consistently making correct market calls is one of the reasons why we ensure our own investment philosophy for the managed portfolios doesn’t depend on macroeconomic forecasts. We instead prefer to use a simple, systematic approach which relies on as few assumptions as possible. (for more information on our investment philosophy, you can read all about it here.)

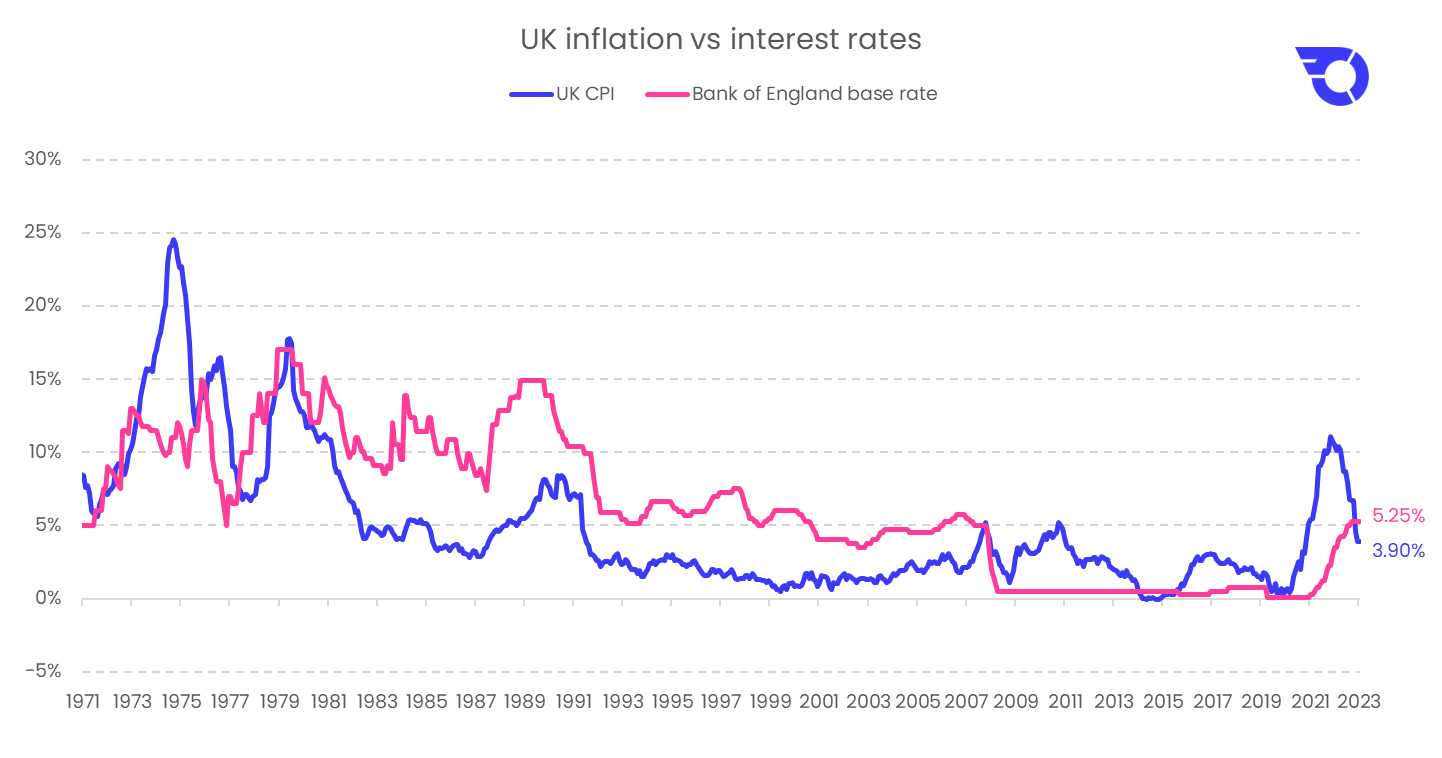

While inflation did rise more than expected in 2023, we’re by no means in unfamiliar territory. If we take a step back and put the past year in perspective, we can see inflation in the UK far exceeded 2023 levels in the 1970s. Not only has inflation failed to reach the heady heights of almost 25% in the 70s, but it’s now started to fall with interest rates only having risen to under a third of what they were in the late 70s – and rates are now in keeping with what would’ve been considered average levels pre-2008:

How much credit you ascribe to central banks for bringing inflation down versus how much you believe inflation has been brought down by the combination of easing of supply chain disruptions, the reduction in excess savings, and the reduction in pent-up demand from COVID is one I’m sure you will all have been debating over the Christmas dinner table. At any rate, mortgage-buyers will be relieved we haven’t hit the 15% interest rates of the 70s and, if the market/central bankers are to be believed (see above), rates may have now peaked.

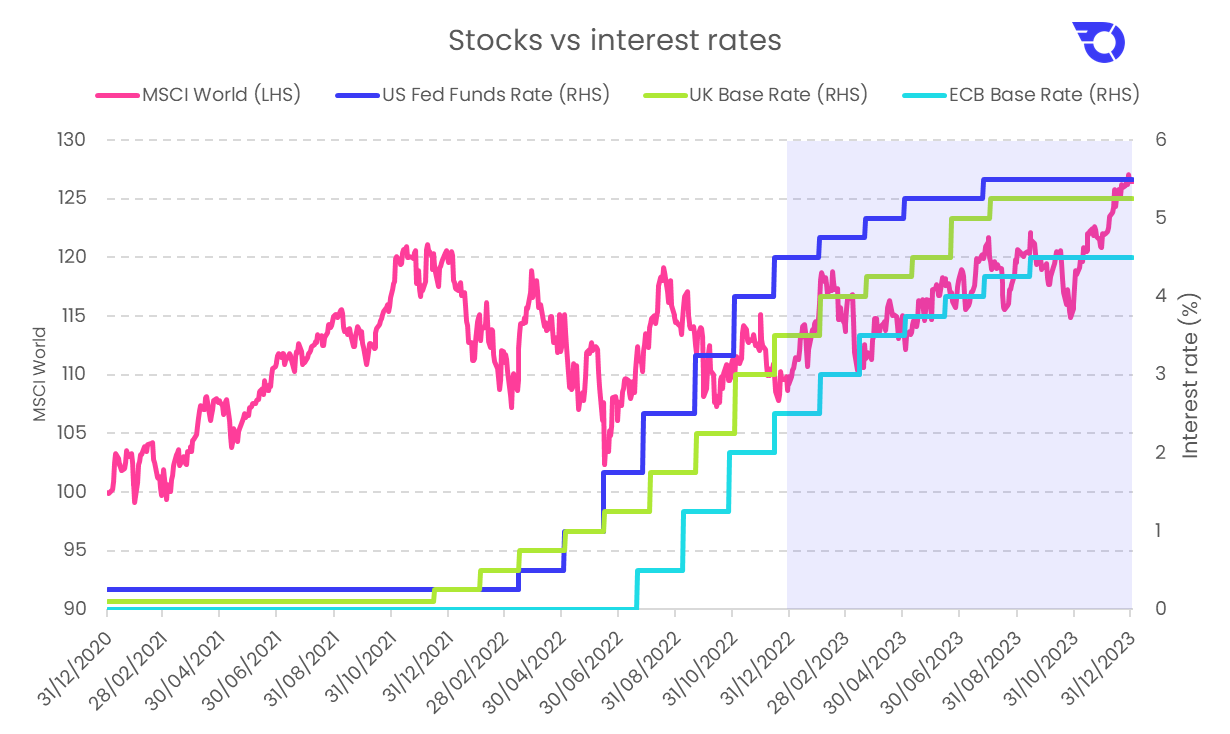

What was equally pleasing for 2023 was that, despite these rising interest rates, stocks still managed to generate strong returns. This brings us to our third story of 2023.

Story 3: Interest rates rise, but so do stocks

This was, at first glance, a surprising result.

Textbook theory suggests that rising interest rates are bad for stocks. Rising rates increase companies’ costs of borrowing, and make their future cashflows less valuable. Instead of buying a stock for its future cashflows, you could put the cash in the bank and earn high rates of interest – increasing the opportunity cost of owning stocks. This did not play out in 2023, though, as despite rates not only rising, but rising faster than expected (as mentioned above), global stocks still generated double-digit returns for the year:

If you’d asked any (truthful) institutional investor at the end of 2021 what they imagined stocks would have returned if rates were to go from almost zero to over 5% in 2 years, almost none would’ve said stocks would be up, and exactly none would have said they’d be making all-time highs.

This strength of the stock market during a rising rate environment is explainable by two factors: 1) markets are forward looking, and 2) rate rises don’t occur in a vacuum. Much of the pain for the stock market caused by rising rates was felt during 2022, where both stocks and bonds fell in unison as the market realised rates were going to have to rise faster than was previously expected. 2022 bond prices fell on the expectation of rate rises throughout 2023. But despite rates continuing to rise in 2023, as the year progressed and inflation started to slow, the market (helped by central bank rhetoric) quickly began to price in interest rate cuts for the following year. The prospect of lower interest rates in 2024 helped stocks generate strong returns in 2023, and recover the ground lost in 2022.

Now for the second reason stocks have continued to rise during a rising-rate environment: rate rises don’t occur in a vacuum. While it’s true that a simple increase in the interest rate reduces the value of a stock, this assumes no other changes to how the business operates. Last year’s rate rises coincided with potentially revolutionary advances in artificial intelligence, which served to greatly improve the prospects for many companies – most notably the largest US technology companies. Even putting the AI hype to one side, the wider market still saw strong earnings results and forward guidance throughout the year, implying many companies are continuing to thrive in a world with higher rates. Businesses are adapting, and higher rates have in many cases been offset by expectations of higher future cashflows.

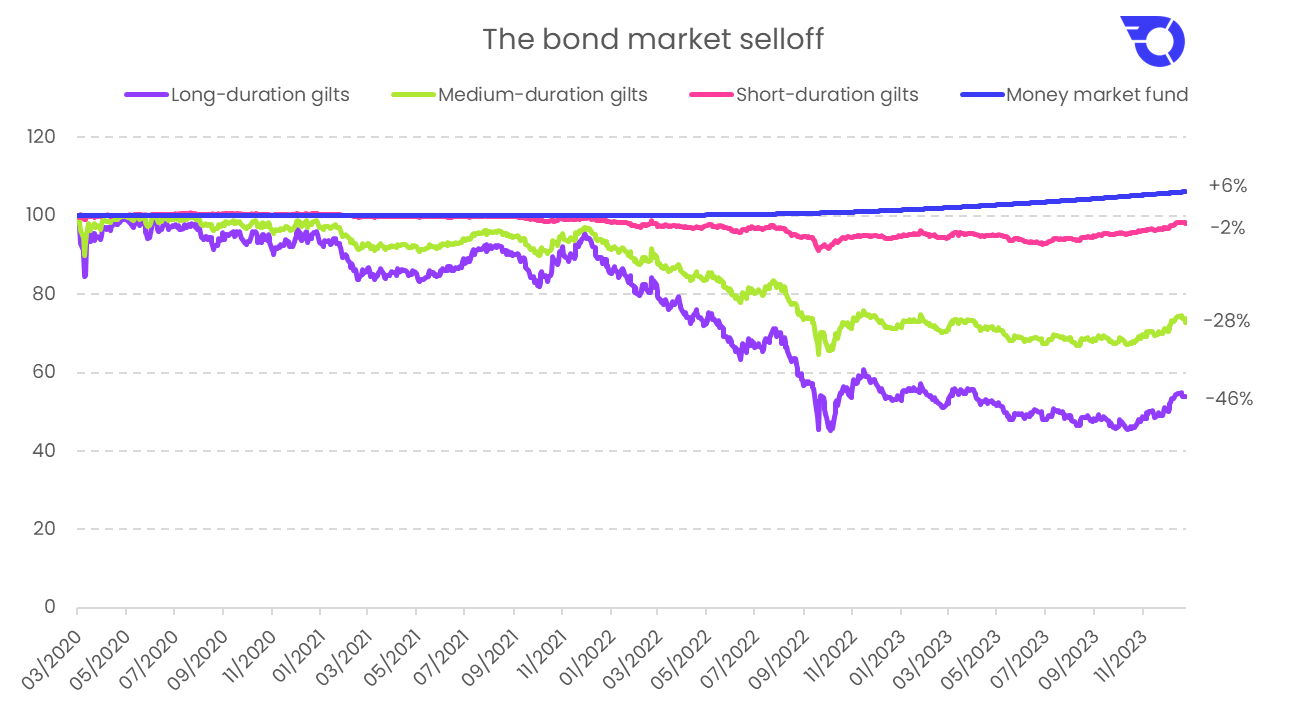

Not only did equity markets shrug off the effects of rising rates in 2023, bond investors also started to recover some of their losses.

Story 4: The bond selloff

2022 was an annus horribilis for bond investors, with the expectation of future rate rises wreaking havoc on bond prices.

For most of 2023 it seemed like this trend was continuing, with most medium to long-term bond funds falling even further as we entered October. Thankfully a last-minute bond rally over the last two months of the year relieved all of the pain felt for the first ten months, with almost all government bond funds ending the year higher than when they started.

As for how much pain bond investors felt in 2022 (and the majority of 2023), this will have depended on how much duration was being taken in their portfolios.

For those unfamiliar, duration is a measure of sensitivity to interest rates, and is dependent on how far in the future a bond’s cashflows are. Long duration bonds are those whose cashflows are far off in the future – a bond which pays no coupons, but matures in 15 years time has a duration of 15. (its duration would be lower if it paid coupons, as those coupons would be closer to today). A bond with a duration of 15 moves roughly 15% for every 1% move in interest rates – so would fall about 15% with a 1% rise in interest rates, and rise about 15% for every 1% fall in interest rates.

Because expectations of future rate rises were revised so heavily upwards during 2022, those long duration bonds, which are the most sensitive to interest rate movements, fell – a lot. Funds which hold only long-duration bonds fell to losses of 55% since the bond selloff started in March 2020, and despite the strong bond rally over the last couple of months of 2023, are still over 40% below their highs:

Gilt funds with moderate levels of duration (such as most aggregate funds, with duration levels of around 9) fell less than long-duration bonds, as expected. Short-duration bonds are now only barely below their peak, and money-market funds, which tend to have durations of under a month, are benefitting from the rising rate environment.

This is all because the shorter a fund’s duration, the less its price falls when rates rise, and importantly the faster the fund will benefit from the new bonds it’s buying, which will have higher yields resulting from the higher interest rates. As a bond fund is simply a collection of individual bonds, once interest rates rise, shorter-duration bond funds have low-coupon bonds maturing and are able to reinvest the proceeds into new higher-yielding bonds. This means they’re able to more quickly offset the reduction in price the bonds will have suffered as a result of the rate rises. Funds which hold longer duration bonds, however, fall further, and take longer to buy the new higher yielding bonds (because of their longer maturity) – therefore taking longer to recover.

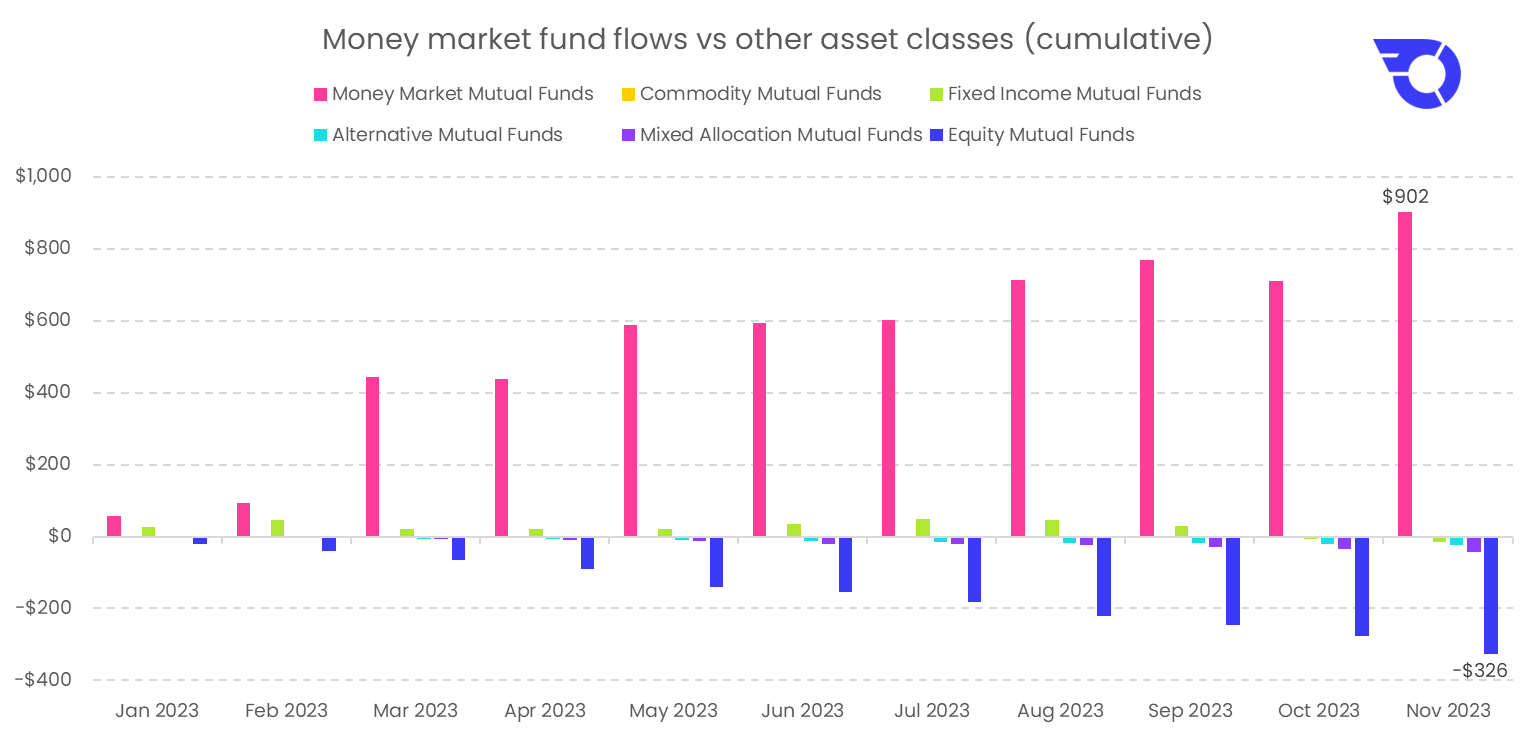

What this environment of rising rates has been hugely beneficial for, then, is money market funds.

Story 5: The rise of money market funds

As a result of the ultra-short duration money market funds benefitting from the higher interest rate environment, they’ve been attracting huge amounts of investor attention.

Looking at US mutual fund data, money market mutual funds were the only asset class to see inflows over the year. Not only did they garner inflows, but the magnitude of inflows compared to the other asset classes was staggering:

Sadly data limitations prevent a full comparison of flows for both ETFs and mutual funds, as the picture for equity funds on the whole was not as bleak as the chart above indicates – many US investors moved out of equity mutual funds into equity ETFs due to their favourable tax treatment in the US. Nonetheless, the story of money market funds dominating flows relative to the other asset classes during 2023 remained true.

With money market funds now yielding over 5%, it’s little wonder they’re investors’ asset class of choice heading into 2024.

Important information

Capital at risk. The value of your portfolio with InvestEngine can go down as well as up and you may get back less than you invest. ETF costs also apply.

This communication is provided for general information only and should not be construed as advice. If in doubt you may wish to consult a professional adviser for guidance.

Tax treatment depends on personal circumstances and is subject to change, and past performance is not a reliable indicator of future returns.