{kind=link}

ETFs by J.P. Morgan Asset Management

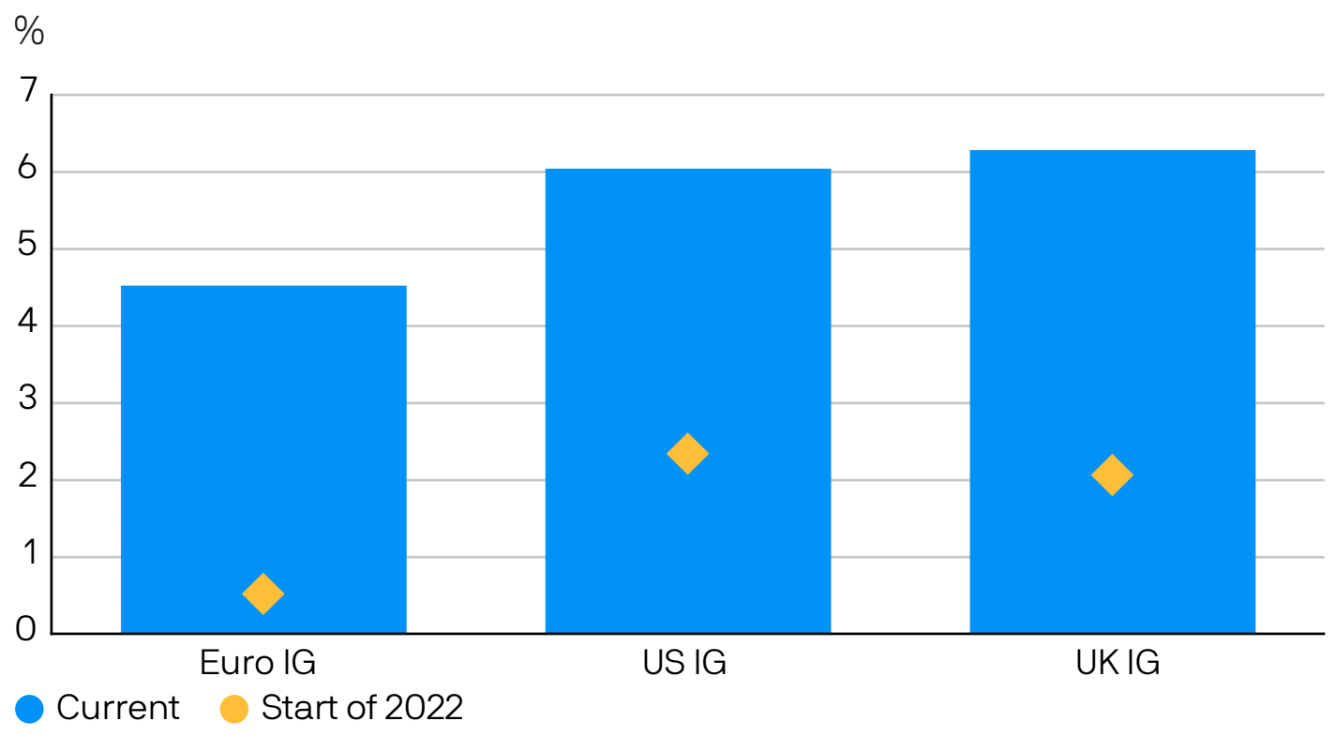

1. Yields are attractive

Current investment grade (IG) yields are at decade-plus highs, with US IG companies currently offering yields of over 5%, and their European counterparts over 4%. Investment grade bonds are issued by the highest quality issuers, as rated by credit rating agencies such as Moody’s and S&P.

Fixed income yields

These yield levels help reduce downside exposure for longer-term investors. Spreads (the difference between IG yields and government bond yields) have tightened, and now sit broadly in line with long-run averages, reflecting the market’s expectation for higher-for-longer interest rates alongside a thus far resilient earnings outlook.

However, investment grade spreads have not tightened as much versus historical averages as spreads in the lower quality high yield market, particularly in the US. As a result, valuations in the higher quality segments of the credit market look attractive relative to their high yield counterparts.

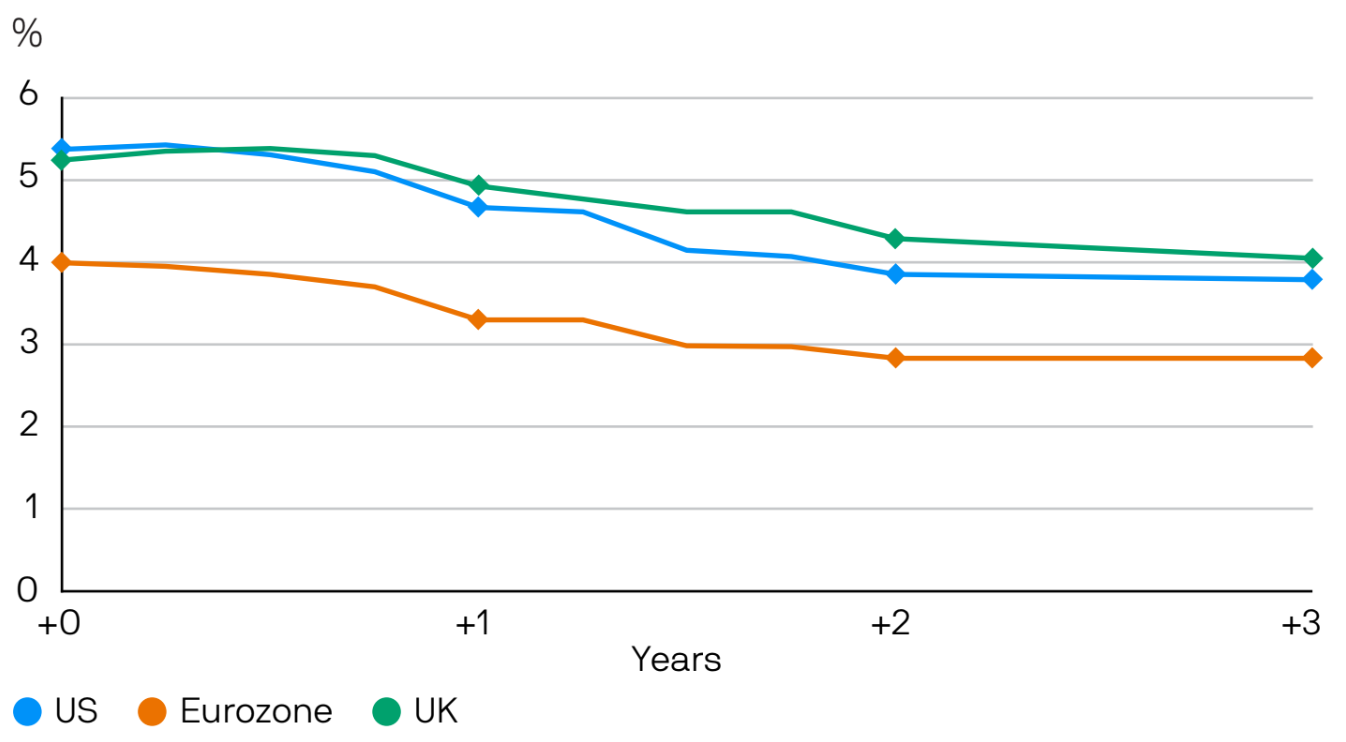

2. End of interest rate rising cycle is generally a positive

Base rates in developed economies are elevated and we expect them to remain so for a fairly extended period. However, investors are increasingly confident that rate rising cycles are reaching a conclusion, both in the US and Europe.

Market expectations for central bank policy rates

While the path of the economy has varied after the last rate rise of a tightening cycle, bond returns have been fairly consistent, with high quality fixed income typically performing well. In particular, in the US a broad high-quality bond index has always outperformed cash over the two years from the last increase of the cycle (in every instance since the 1980s). Thus, a peak in rates should be a positive for higher quality fixed income.

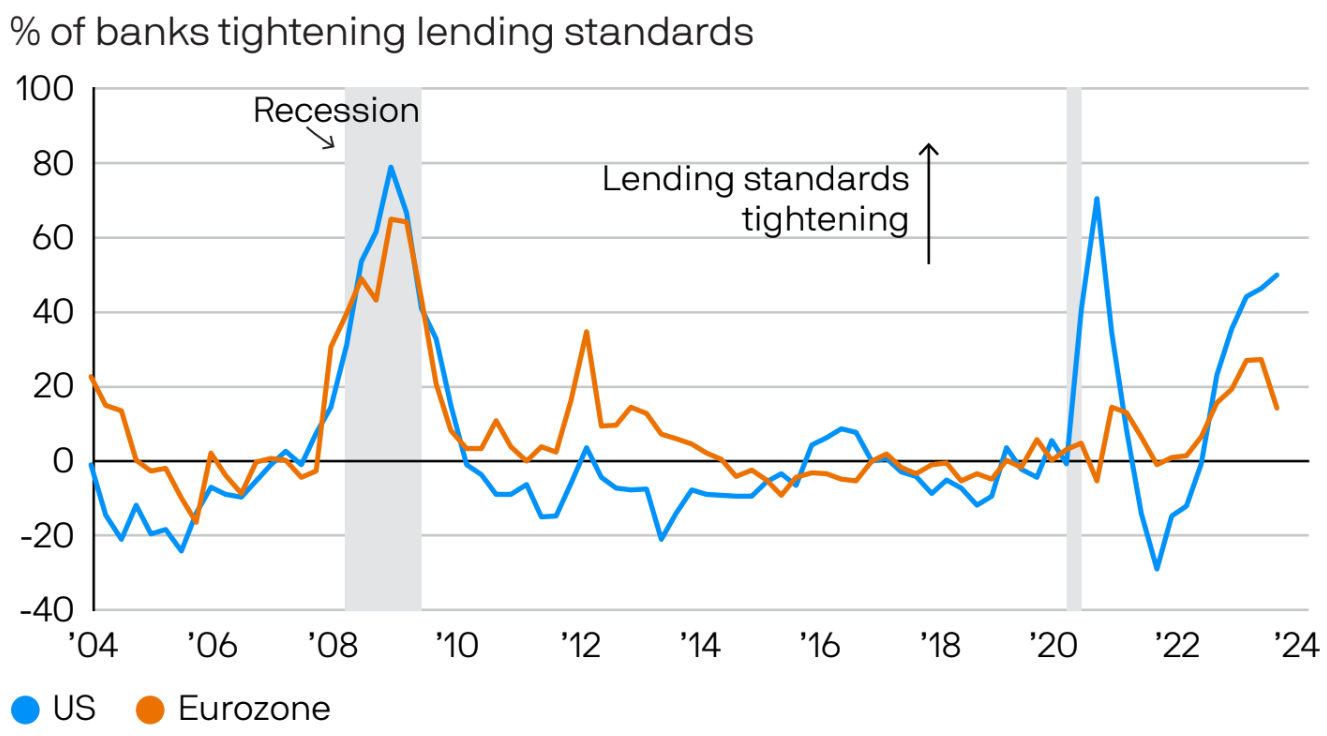

3. Lending standards tightening, but fundamentals are resilient

Lending to companies has slowed over recent quarters as the impact of the central bank tightening cycles feeds through to the real economy. Banks have tightened lending standards in both the US and Europe, leading to a fall in corporate bank loan demand. However, lower financing needs and available internal funding were cited as reasons for this lower demand alongside higher interest rates.

US and eurozone lending standards

Corporate fundamentals look resilient, with ratings in both the US and European corporate sectors drifting higher. Firms have also been remarkably successful in pushing out maturity schedules, locking in the lower yield levels of 2020 and 2021. US non-financial IG firms have just 6% of debt coming due in 2024, and only 8% in 2025.

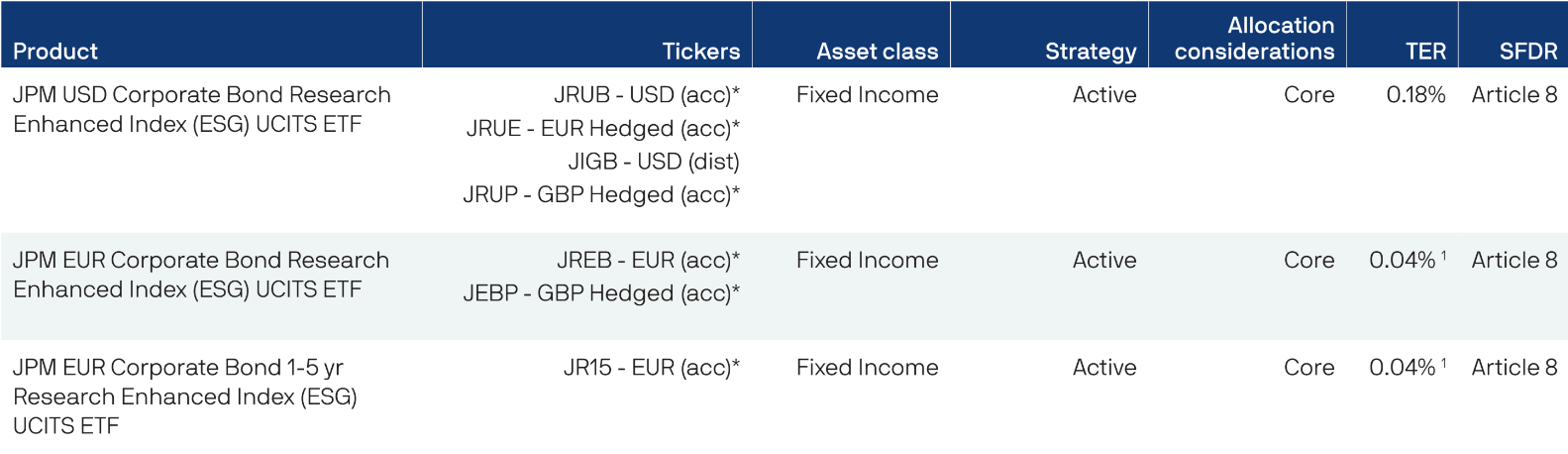

Investment grade corporate bonds: ETF building blocks

¹The TER includes a fee waiver by the Management Company in the amount of 0.15% per annum. From 1 June 2024 the ongoing charge will revert to 0.19% per annum.

Educational content produced as part of a paid partnership

Important information

*FOR BELGIUM ONLY: Please note the acc share class of the ETF marked with an asterisk in this page are not registered in Belgium and can only be accessible for professional clients. Please contact your J.P. Morgan Asset Management representative for further information. The offering of Shares has not been and will not be notified to the Belgian Financial Services and Markets Authority (Autoriteit voor Financiële Diensten en Markten/Autorité des Services et Marchés Financiers) nor has this document been, nor will it be, approved by the Financial Services and Markets Authority. This document may be distributed in Belgium only to such investors for their personal use and exclusively for the purposes of this offering of Shares. Accordingly, this document may not be used for any other purpose nor passed on to any other investor in Belgium.

This is a marketing communication and as such the views contained herein do not form part of an offer, nor are they to be taken as advice or a recommendation, to buy or sell any investment or interest thereto. Reliance upon information in this material is at the sole discretion of the reader. Any research in this document has been obtained and may have been acted upon by J.P. Morgan Asset Management for its own purpose. The results of such research are being made available as additional information and do not necessarily reflect the views of J.P. Morgan Asset Management. Any forecasts, figures, opinions, statements of financial market trends or investment techniques and strategies expressed are, unless otherwise stated, J.P. Morgan Asset Management’s own at the date of this document. They may not necessarily be all-inclusive and may be subject to change without reference or notification to you. The value of investments and the income from them may fluctuate in accordance with market conditions and taxation agreements and investors may not get back the full amount invested. Changes in exchange rates may have an adverse effect on the value, price or income of the products or underlying overseas investments. Past performance and yield are not a reliable indicator of current and future results. There is no guarantee that any forecast made will come to pass. Furthermore, there can be no assurance that the investment objectives of the investment products will be met. J.P. Morgan Asset Management is the brand name for the asset management business of JPMorgan Chase & Co. and its affiliates worldwide. To the extent permitted by applicable law, we may record telephone calls and monitor electronic communications to comply with our legal and regulatory obligations and internal policies. Personal data will be collected, stored and processed by J.P. Morgan Asset Management in accordance with our EMEA Privacy Policy www.jpmorgan.com/emea-privacy-policy. As the product may not be authorised or its offering may be restricted in your jurisdiction, it is the responsibility of every reader to satisfy himself as to the full observance of the laws and regulations of the relevant jurisdiction. Prior to any application investors are advised to take all necessary legal, regulatory and tax advice on the consequences of an investment in the products. Shares or other interests may not be offered to or purchased directly or indirectly by US persons. All transactions should be based on the latest available Prospectus, the Key Information Document (KID) and any applicable local offering document. These documents together with the annual report, semi-annual report, instrument of incorporation and sustainability-related disclosures, are available in English from JPMorgan Asset Management (Europe) S.à r.l., 6 route de Trèves, L-2633 Senningerberg, Grand Duchy of Luxembourg, your financial adviser or your J.P. Morgan Asset Management regional contact or at www.jpmorganassetmanagement.ie. A summary of investor rights is available in English at https://am.jpmorgan.com/lu/investor-rights. J.P. Morgan Asset Management may decide to terminate the arrangements made for the marketing of its collective investment undertakings. Units in Undertakings for Collective Investment in Transferable Securities (“UCITS”) Exchange Traded Funds (“ETF”) purchased on the secondary market cannot usually be sold directly back to UCITS ETF. Investors must buy and sell units on a secondary market with the assistance of an intermediary (e.g. a stockbroker) and may incur fees for doing so. In addition, investors may pay more than the current net asset value when buying units and may receive less than the current net asset value when selling them. In Switzerland, JPMorgan Asset Management Switzerland LLC (JPMAMS), Dreikönigstrasse 37, 8002 Zurich, acts as Swiss representative of the funds and J.P. Morgan (Suisse) SA, Rue du Rhône 35, 1204 Geneva, as paying agent. With respect to its distribution activities in and from Switzerland, JPMAMS receives remuneration which is paid out of the management fee as defined in the respective fund documentation. Further information regarding this remuneration, including its calculation method, may be obtained upon written request from JPMAMS. This communication is issued in Europe (excluding UK) by JPMorgan Asset Management (Europe) S.à r.l., 6 route de Trèves, L-2633 Senningerberg, Grand Duchy of Luxembourg, R.C.S. Luxembourg B27900, corporate capital EUR 10.000.000. This communication is issued in the UK by JPMorgan Asset Management (UK) Limited, which is authorised and regulated by the Financial Conduct Authority. Registered in England No. 01161446. Registered address: 25 Bank Street, Canary Wharf, London E14 5JP.