{kind=link}

Despite inflation slowing for the second month in a row, UK households are still paying a lot more for goods and services when compared to 12 months ago, with food and energy being the key drivers.

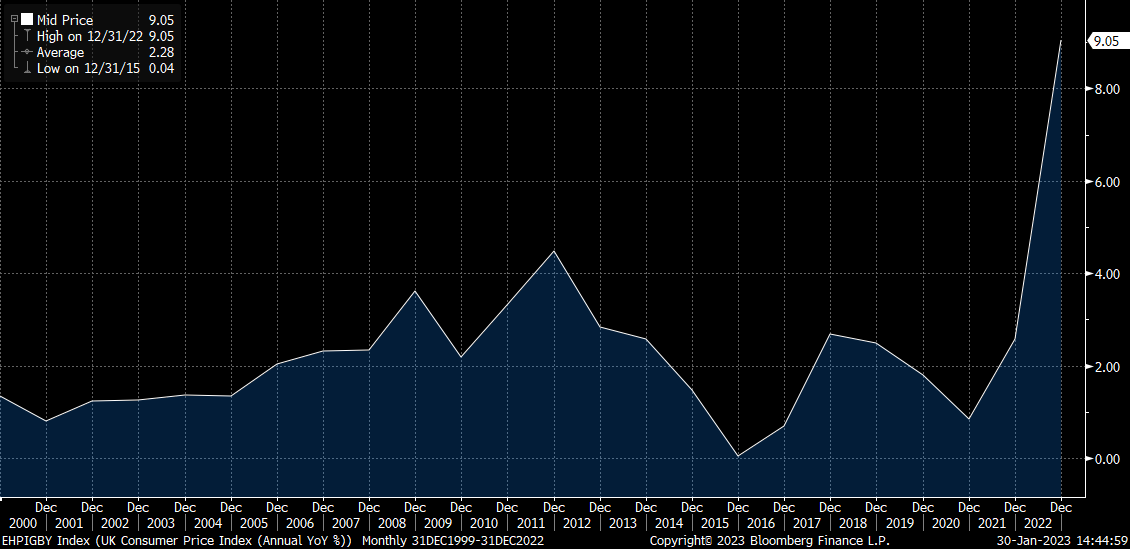

The UK’s CPI cooled down marginally to 10.5% in December 2022 as the Bank of England raised rates for the ninth time in a bid to slow price rises down.

In this post, we’ll cover the topic of inflation and explore how it impacts your savings and investments over the long run.

What is inflation?

Inflation is the measure of how much the price of goods (like food or fridges) and services (like haircuts or train tickets) have risen over time.

Usually, inflation is measured by comparing the price of things today with how much they cost a year ago. The average increase in these prices is known as the inflation rate.

For example, if inflation is 3%, it means prices are 3% higher (on average) than they were a year ago. If a loaf of bread cost £1 a year ago, and £1.03 today, then its price has risen by 3%.

To keep inflation under control, most Central Banks in developed economies will target an annual rate of around 2%.

How is inflation measured?

Every month, the Office for National Statistics (ONS) looks at around 180,000 prices of a basket of 700 items. These change as our spending habits evolve and include the likes of eggs, child car seats, draught lager, screwdrivers, mobile phone charges, driving lessons and pet insurance.

It is also important to note that the CPI and RPI numbers are usually very different from household to household. For example, the inflation basket of goods includes televisions, household appliances down to bread, milk, eggs and clothes. It is easy to argue a case where a household would buy milk more frequently than a new TV.

In 2022, pet collars, antibacterial surface wipes and meat-free sausages were added, while coal and doughnuts were removed. As each household’s spending varies, each person’s inflation rate will likely differ from the rate reported.

The average price of the goods and services in the basket is compared with last year’s figures to work out the rate of inflation. The consumer price index (CPI) measure of inflation, which is the most commonly used, does not take into account housing costs but it factors in other goods and services.

The retail price index (RPI), which was previously used, includes mortgage interest payments, which means it’s heavily affected by house prices and interest rates.

When is each measure of inflation used?

The UK uses both measures of inflation for different purposes.

For example, the RPI (which includes housing costs) is taken into account in train tickets; mobile phone tariffs; final salary pension payments; car taxes and alcohol duties.

On the other hand, the CPI (which excludes housing costs) is linked to state pensions and a number of social services like universal credit, housing benefits and income support.

The government tends to link its own spending to CPI. These decisions include things like the state pension, for example.

The effects of inflation

As mentioned above, inflation is the measure of the cost of living presented as a rate at which the prices of goods and services increase over time.

- High inflation translates to the loss of buying power and living standards if wage increases fail to keep pace.

- Low inflation means prices are rising slowly; this tends to be good for consumers as prices are unlikely to be rising faster than wages.

- Stagflation refers to a period in which inflation is rising while economic growth is falling. This is considered the worst case scenario and it is often the situation that prompts central banks to increase interest rates.

- Deflation is when prices fall. This occurs when there is very low demand for goods and services. This usually translates into consumers putting off spending, as they expect prices to continue to get cheaper. This is rare, and also a sign of a severe economic problem.

Why is inflation so high right now?

A combination of factors has contributed to inflation running at multi-decade highs.

The combination of a surge in global energy prices and complications within global supply chains, has been thrown into sharp relief by the widely globalised world we live in today. Rising food prices and energy prices continue to be the biggest contributors to the high inflation figures we’re seeing in the UK.

Is Inflation good or bad?

Low inflation is, generally, seen as a positive as it tends to encourage spending given the expectation of prices rising in the future.

High inflation (usually in excess of 2%), on the other hand, tends to mean a reduction in the standard of living as goods and services get more expensive. This, in turn, puts pressure on disposable incomes.

High inflation is also problematic for savers as interest rates are unlikely to be above inflation, meaning that real terms purchasing power is slowly eroded away.

Despite the recent increase in rates across savings accounts, these offers are still unlikely to beat inflation, which will continue to erode the value of accounts in real terms.

This is why many investors believe that the best way to combat high inflation continues to be by investing your money.