{kind=link}

Last week, we saw a full house of interest rate movements across the world’s major national banks. The Bank of Japan hiked, the Fed kept rates on hold, and the Bank of England made its first cut.

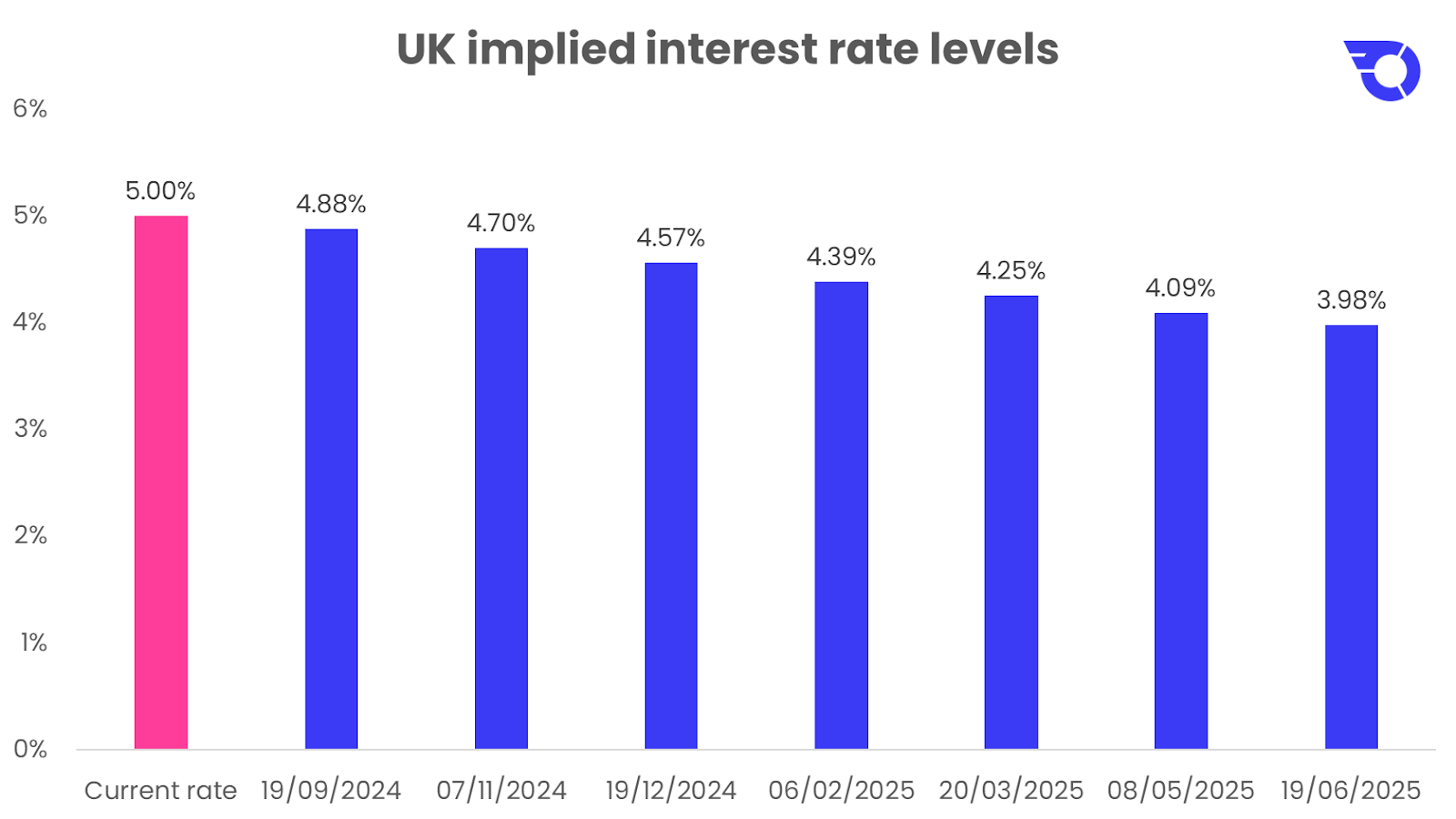

The UK’s central bank cut rates for the first time since 2020, reducing their base rate from 5.25% to 5%. The decision was voted through by a slim majority, with the Monetary Policy Committee voting five to four in favour of a cut.

The central bank also published inflation forecasts suggesting that further cuts lie ahead, and the market now expects at least one further rate cut by the end of the year. This might appear to be a slight move, but it will impact investors in the UK going forward.

What do investors need to know about the decision?

Interest rates for savers

As the Bank of England’s base rate comes down, returns on savings accounts offered by banks will also come down. In fact, you might have seen banks preemptively lowering their rates in anticipation of the Bank of England’s decision.

For InvestEngine investors, this could signal a slight change in the amount generated by Money Market ETFs. These ETFs track the SONIA rate – an average of interest rates across the UK – which has sat at 5.2% for the last year. Last week’s decision brought the SONIA rate down to 4.95%.

It’s important to remember that this figure is still high, historically speaking. Investors can still target a close to 5% return on their investments with Money Market ETFs, but further changes will impact this figure as we see rates come down.

Financial markets

Financial markets are also affected by changes in interest rates. For equities, a hike in interest rates typically increases borrowing costs for companies which may affect their profitability and future cash flow. A cut in interest rates means companies may see lower borrowing costs allowing them to expand and increase their competitive edge through debt financing.

In bonds, yields are also directly related to the base interest rate of the country. Any cut in base interest rate will translate into lower bond yields which will increase bond prices.

Interest on debts

As a general rule, high interest rates are good for people with savings and bad for people with debt. So, any decision to cut rates will be a broad positive for people with mortgages and a negative for those with cash in savings accounts.

If you have a mortgage on a variable rate, or you’re about to agree to new terms, the decision will be a welcome one. Any more cuts, as we could see before the end of the year, will further ease the burden on mortgage holders.

As for other types of debt, the answer really depends on the type of debt you have. ‘Fixed interest’ debts will obviously be unaffected. Also, depending on how competitive the debt market is, some lenders may see no reason to make any changes despite the rate cuts.

The wider economy

Let’s now turn our attention to the wider UK economy, with inflation now firmly closer to the target of 2%, with GDP figures which for 2024 have surprised to the upside, the Bank of England can begin to relax credit conditions slowly.

Whilst there have been cost pressures when it comes to the cost of living, energy prices and stubborn service inflation data, the UK economy remains strong ahead of many economists’ expectations.

Important information

Capital at risk. The value of your portfolio with InvestEngine can go down as well as up and you may get back less than you invest. ETF costs also apply.

This communication is provided for general information only and should not be construed as advice. If in doubt you may wish to consult a professional adviser for guidance.

Tax treatment depends on personal circumstances and is subject to change, and past performance is not a reliable indicator of future returns.