{kind=link}

Welcome to the latest edition of our monthly market roundups. This time we’re looking at the key topics from October, a challenging month across most major asset classes. We’ll also take a look at some of last month’s more unusual market stories.

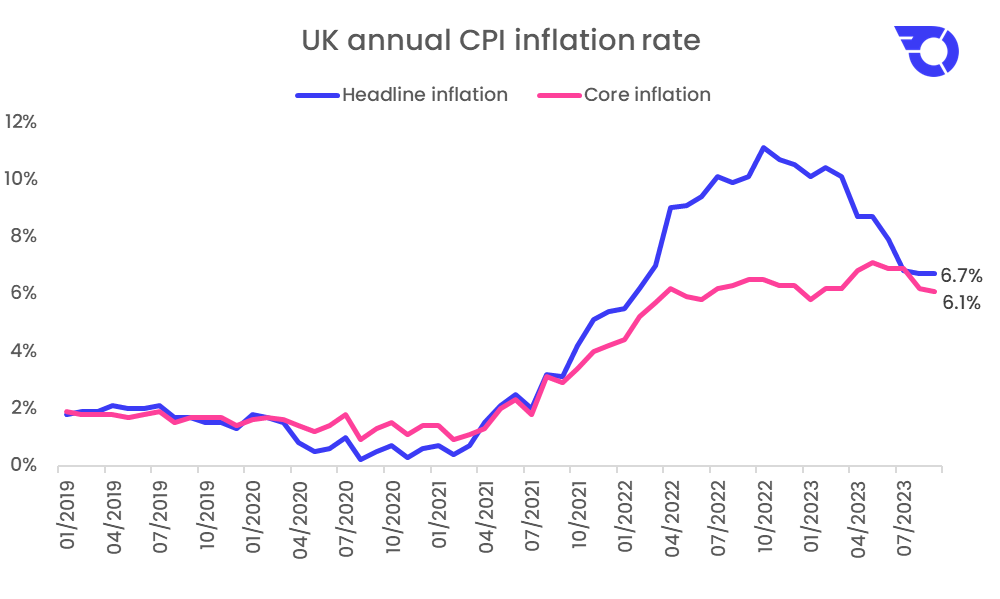

Inflation steadies

Inflation remained sticky with the headline figure coming in at 6.7% in the 12 months to September, unchanged from the previous month.

While petrol prices rose, this was offset by falling food prices, with food and drink inflation falling from 13.6% to 12.2% on an annual basis. On a monthly measure, food price inflation fell 0.2%, the largest drop since September 2021, as the cost of items like milk and eggs began to decline.

Due to the easing food price inflation, core inflation, which excludes food and energy, slowed to 6.1% from 6.2%. While core inflation showed signs of moderating, this was still above the 6% expected by economists.

Source: Bloomberg

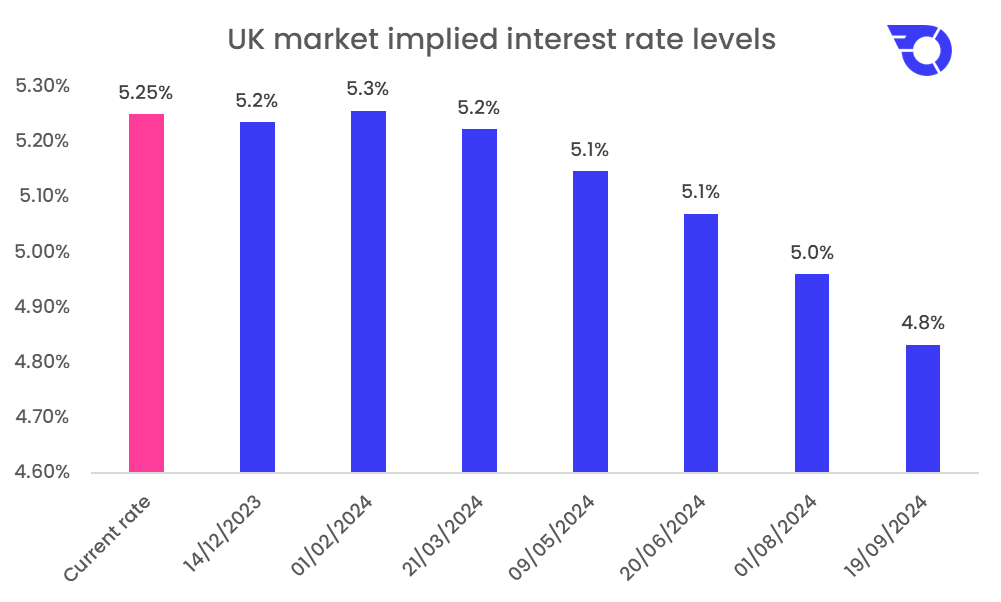

Interest rates unchanged

At the most recent Bank of England meeting on the 2nd of November, the central bank held rates at 5.25%.

The Bank of England governor, Andrew Bailey, noted that it was too early to be thinking about rate cuts, and said rates will need to stay high for an “extended” period of time. The question now is how long a period the word “extended” implies.

The bank noted that recent inflation deceleration can be attributed, in large part, to reduced contributions from the energy component. However, it was also acknowledged that significant upside inflation risks may still arise from the conflict in the Middle East.

Source: Bloomberg

Higher borrowing costs are beginning to impact consumers as UK mortgage approvals decline to an eight-month low. While mortgage rates have eased in recent months, home buyers and those who are looking to refinance are still facing larger costs compared to the first half of 2022.

In the US, the Federal Reserve has also elected to keep rates on hold, with guidance that the rise in long-duration treasury yields had reduced the need to tighten rates much further.

Equity markets fall

October saw most major equity indices finish lower for the month as a result of the geopolitical tensions in the middle east, a mixed set of earnings results, and the market adjusting to the “higher for longer” interest rate narrative.

The UK’s FTSE 100 drifted lower, with BP leading declines on disappointing quarterly earnings, dragging down the sector and the index. NatWest saw its share price decline more than 24% on the back of poor earnings.

The S&P 500 declined on a mix of corporate earnings and higher interest rate expectations. The deteriorating outlook for corporate earnings and falling profit forecasts have been partially responsible for the move lower on the index, as companies warned of a slowdown in demand and an uncertain economic outlook.

European equities declined -2.08%, having the worst month this year. Eurozone economic growth was weaker than expected and German retail sales unexpectedly fell in September given persistent high inflation.

Emerging markets declined -4.07%.

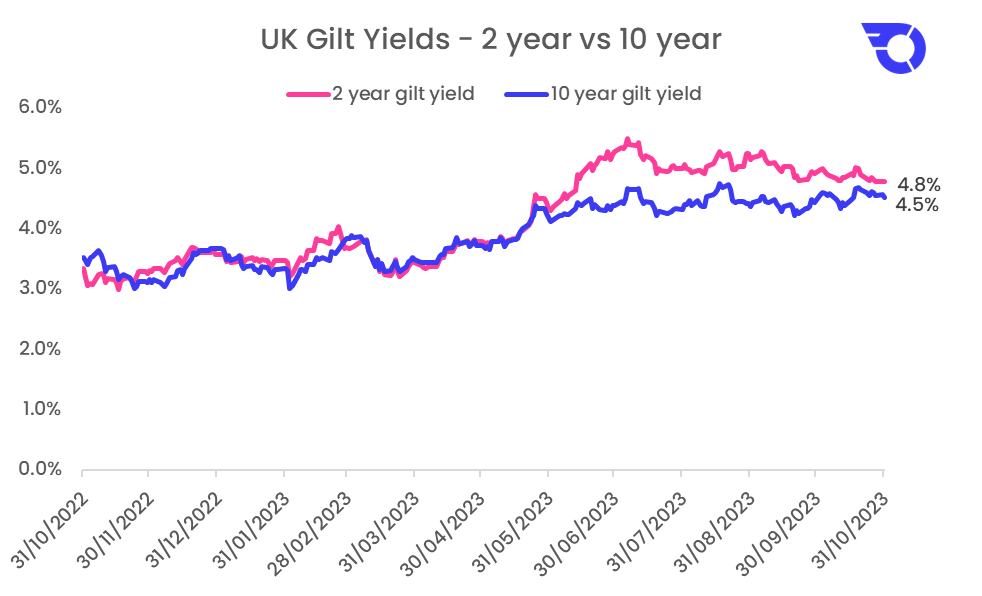

Bond yields steady

UK bond yields remained largely unchanged for the month, as central banks continue to weigh their own interest rate and inflation objectives.

The 2-year UK gilt finished the month at 4.8% and the 10-year at 4.5%:

Source: Bloomberg

In the US, a deepening bond sell-off drove the 10-year treasury yield to 5% for the first time in 16 years. The continued rise in long-term yields has been caused by multiple factors, including persistent quantitative tightening from the Fed, BRICs countries continuing to sell down their reserves of US treasury bonds, and stronger than expected US economic data.

Sterling performance broadly flat

For October, Sterling remained broadly flat, finishing at $1.2153 against the US Dollar and €1.1490 against the Euro.

Commodities

The recent geopolitical events have added volatility to the commodity sector, with oil prices rising to a high for the year of $95.03 at the end of September, before falling back to finish October at $81.02.

Off the beaten track

Now, let’s take a look at some of the more unusual market news stories from October.

The alpha of ugliness

Utilising the state-of-art deep learning technique to quantify facial attractiveness, the authors of this paper, entitled “What Beauty Brings? Managers’ Attractiveness and Fund Performance”, find that funds with facially unattractive managers outperform funds with attractive managers by over 2% per annum.

Lego outperforms most VCs

Consistent with an academic paper from 2018, more research has found that Lego blocks generate higher returns than many conventional asset classes.

Goldman Sachs insider trader had previously won an ethics competition

In a wild twist of fate, Anthony Viggiano, who once triumphed in an “Ethics Invitational” competition at the University of Tampa, has now been charged with masterminding an insider trading scheme.

Viggiano allegedly shared confidential information about upcoming mergers and acquisitions with his friends while working at Goldman Sachs, raking in over $300,000 in illicit gains.

They Cracked the Code to a Locked USB Drive Worth $235 Million in Bitcoin. Then It Got Weird

Stefan Thomas lost the password to an encrypted USB drive holding 7,002 bitcoins. One team of hackers believes they can unlock it – but the owner doesn’t want their help.

Important information

Capital at risk. The value of your portfolio with InvestEngine can go down as well as up and you may get back less than you invest. ETF costs also apply.

This communication is provided for general information only and should not be construed as advice. If in doubt you may wish to consult a professional adviser for guidance.