{kind=link}

Welcome to the latest edition of our monthly market roundups.

To say July was a turbulent month would be an understatement. We saw the dawn of a new era of government in the UK, a US presidential assassination attempt, the sitting president dramatically dropping out of the re-election race, an unprecedented rally of support for his party’s replacement, global IT chaos, and record sums wiped off the major US tech stocks.

The market, however, remained laser-focused on the only thing the market cares about – company earnings. Despite Taylor Swift’s best efforts, inflation appears to be heading in the right direction, giving central banks more confidence to cut rates, which provided a tailwind for stocks, and especially bonds in July.

In our ‘Off the beaten track’ section, we look at how much it would cost to buy a stegosaurus, how Elon Musk is planning on putting a million humans on Mars in the next 20 years, and which stock returned 265 million per cent over the last 100 years.

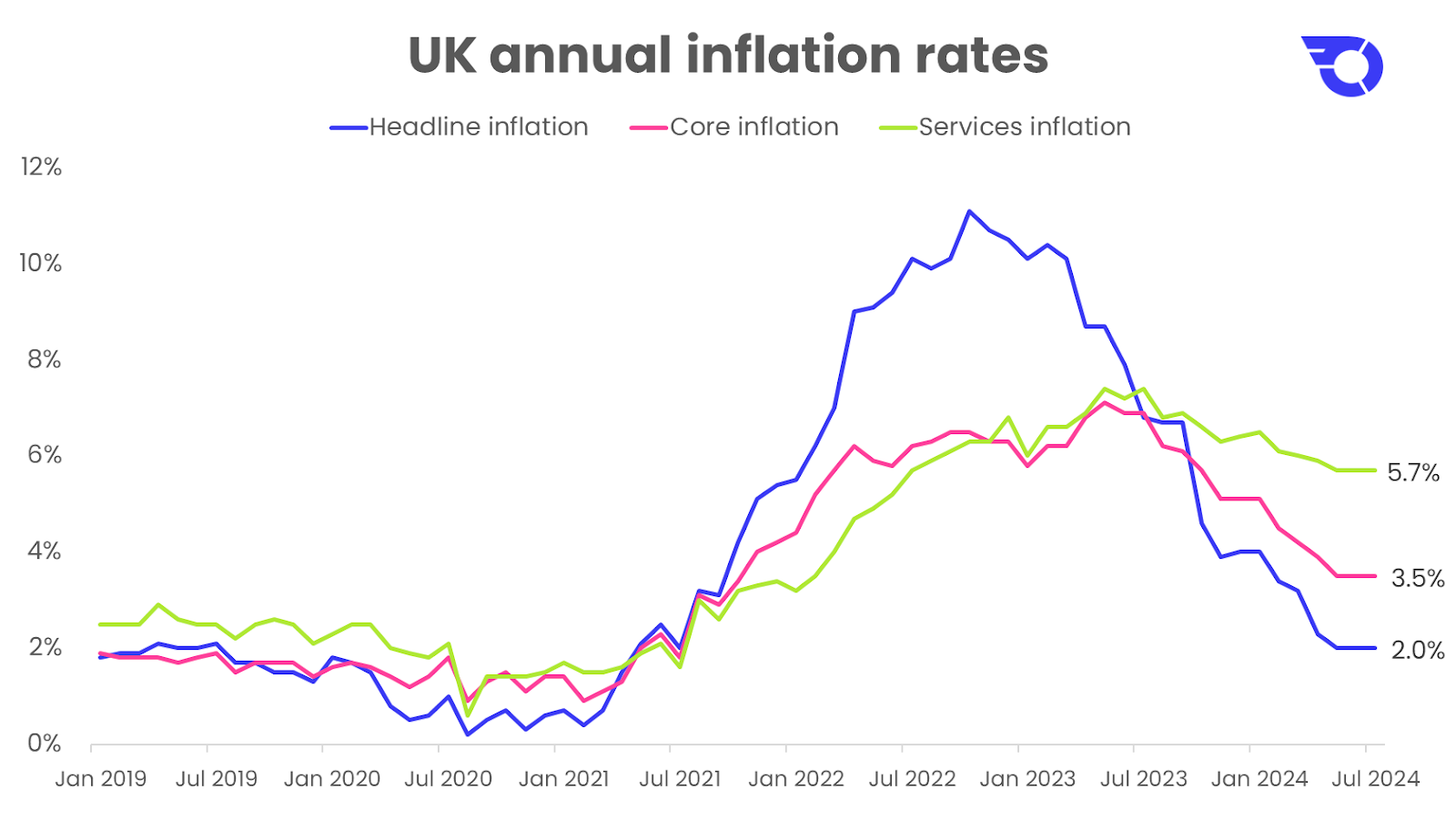

Taylor Swift causing inflation

The headline inflation news for the UK was positive in July, with inflation holding steady at 2%. This was slightly above expectations of 1.9%, but remained at the BoE’s target level of 2% which was first hit in May.

Taylor Swift, however, has been doing her utmost to keep inflation high. Services inflation, which measures inflation in services including hotels and airline tickets, remained elevated at 5.7%, on the back of hotel prices rising 8.8% in the month, likely driven up by Swift’s Eras tour, which came to the UK in June.

Swift’s concerts have significantly influenced consumer price indices throughout Europe, with Sweden’s central bank attributing a notable increase in hotel prices to her performances earlier this year.

Core inflation, which also serves as an important indicator of underlying inflation by excluding food and energy inflation, stayed constant at 3.5% – still above the bank’s 2% target.

Core and services inflation serve as important indicators of underlying inflation as they strip out the more volatile inflation components which are prone to seasonal distortions.

US inflation is also coming down, and faster than expected. Headline US CPI fell faster than forecast to 3% in June, while core CPI rose 3.3%, less than the expected 3.4%. This led to increased bets on interest rate cuts, and a sharp, swift rotation away from the mega-cap companies into more rate-sensitive areas of the market like smaller stocks.

A full house of interest rate moves

July saw a cut, two holds, and a hike from four major central banks around the world.

The Bank of England cut interest rates for the first time since 2020, reducing the bank’s rate from 5.25% to 5% on the 1st of August. The decision was voted through by a slim majority, with the Monetary Policy Committee voting five to four in favour of a cut. The central bank also published inflation forecasts suggesting that further cuts lie ahead, and the market now expects at least one further rate cut by the end of the year.

Elsewhere in the world, the Federal Reserve in the US kept rates on hold at 5.25 to 5.5%. They noted there had been “some further progress” towards the central bank’s target of 2% inflation, as price pressures had eased and the unemployment rate had risen in recent months. Still, they maintained they needed “greater confidence that inflation is moving sustainably towards 2%” before lowering borrowing costs.

The Bank of Japan lifted its benchmark interest rate to 0.25%, as well as announcing plans to halve its monthly bond purchases. This further signals the bank’s intent to reverse the country’s ultra-loose monetary policy and bring some strength to the Yen, which has been on a run of weakness since 2020. The bank in March ended its negative interest rate policy following decades of on-and-off deflation.

The European Central Bank kept its main interest rate at 3.75%, in line with expectations, as it considers whether to cut rates in September despite concerns of geopolitical uncertainty.

Equities shrug off political instability

Despite the month being politically chaotic, equity markets remained largely unconcerned with any political machinations, and were instead moved by July’s raft of central bank meetings and earnings reports.

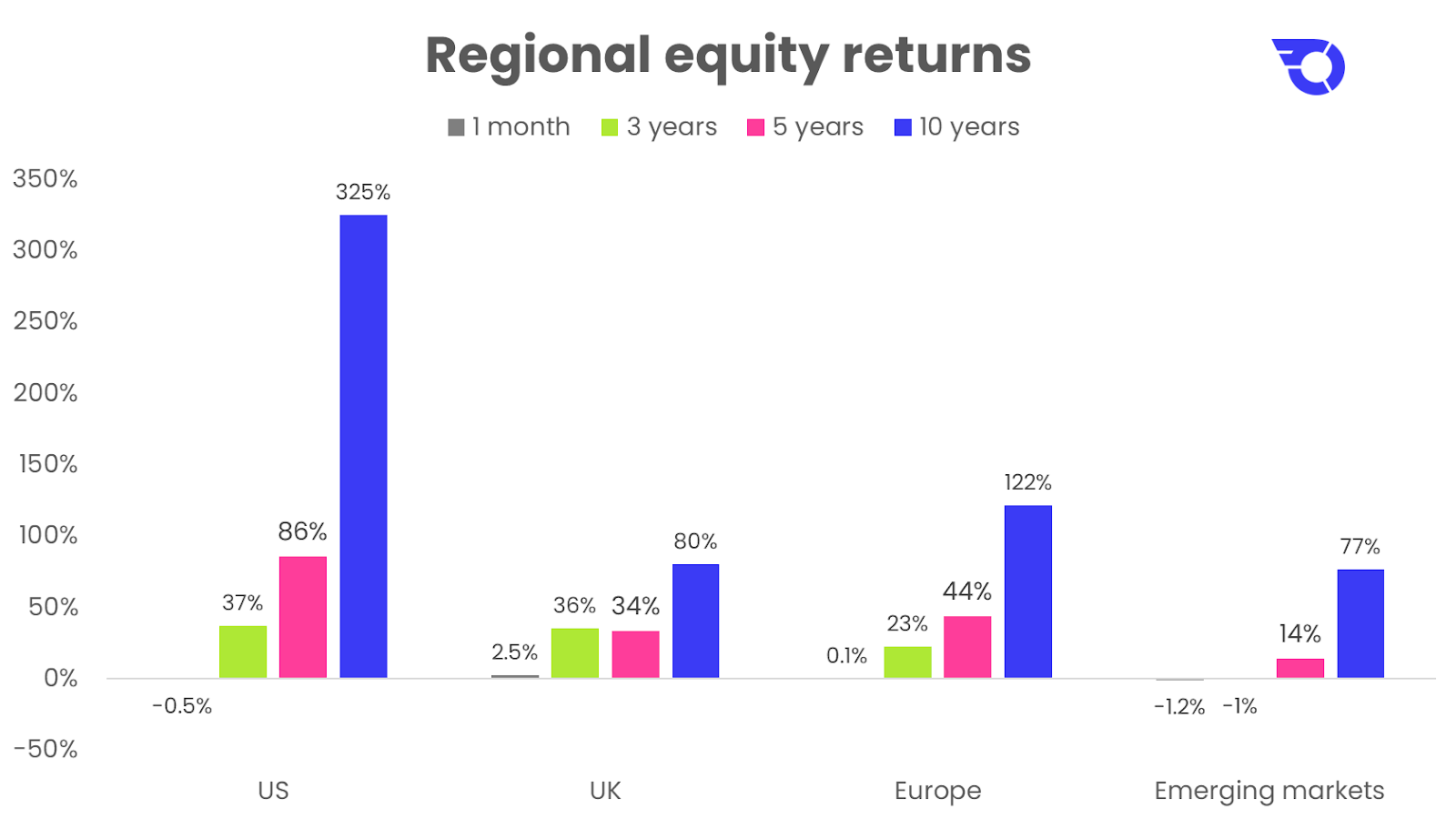

Overall, regional equities were mixed over July, with the UK seeing positive returns, after strong earnings from some of the banks, a bounce in the oil price helping the commodity stocks, as well as increased optimism surrounding rate cuts.

The US market fell slightly in sterling terms, as disappointing earnings from the first few tech companies underwhelmed investors. The better-than-expected inflation data also prompted hopes for earlier rate cuts, which exacerbated the selloff as funds flowed from the richly valued mega-caps into smaller US companies, which are seen to benefit more from lower rates as more of their outstanding debt is tied to floating rates.

Europe remained broadly flat, while Emerging Markets fell 1.2% as investors were unimpressed by the Chinese central bank’s unexpected rate cut and additional liquidity injections. While designed to boost investor confidence, the market took the measures as a sign that deflationary pressures and weak consumer demand were more severe than previously thought.

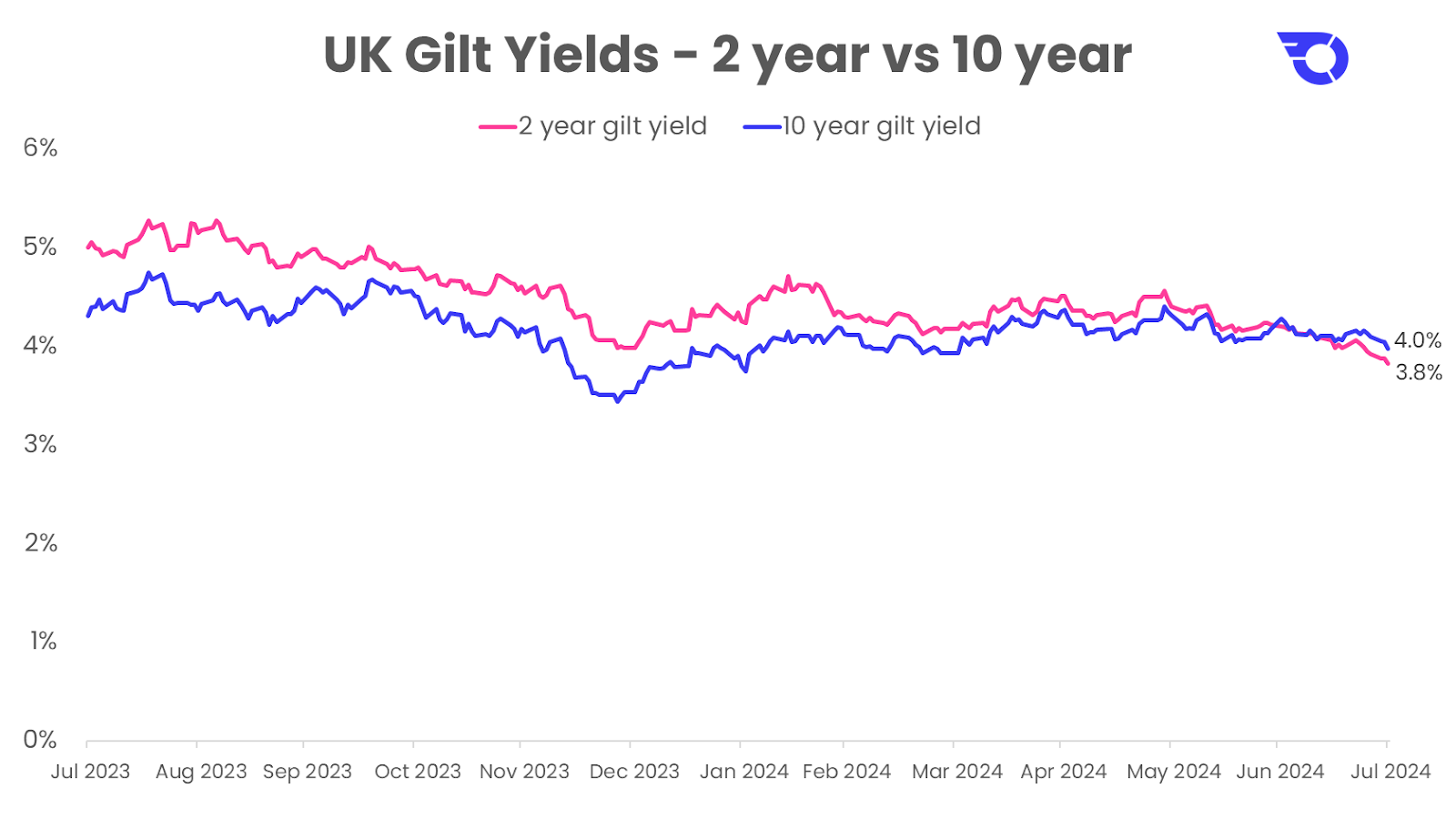

Bond yields fall

With the increased confidence surrounding the Bank of England’s 1st August rate cut, short-term bond yields fell over July from 4.2% to 3.8%. Longer-term bond yields followed suit, with UK 10-year gilt yields falling from 4.2% to 4%.

As short-term yields fell faster than longer-term yields, this caused the UK’s yield curve to uninvert, ending its 13-month streak of inversion (a yield curve inversion occurs when long-term yields are lower than short-term yields, and is considered by some to be a recessionary indicator).

Sterling strengthens

The first half of July saw sterling strengthen considerably versus the US dollar, rising 2.9% amid hopes of US rate cuts, lingering UK inflation, and perceived increased political stability. The second half of July saw some of those gains being given back, but sterling nonetheless finished 1.7% up for the month versus the dollar, rising from a rate of $1.264 to $1.286.

Sterling’s gains were less pronounced versus the Euro, rising from €1.18 to end July at a rate of €1.19.

Off the beaten track

Ken Griffin, the Citadel hedge fund founder, paid $44.6m for a 150m-year-old stegosaurus known as “Apex”, making it the most valuable fossil ever sold at auction.

Elon Musk is planning to put a million humans on Mars in the next 20 years.

A new paper looks at which stocks generated the highest returns over the last 100 years. Seventeen stocks delivered cumulative returns greater than five million percent (earning $50,000 per $1 initially invested). The biggest winner had a cumulative return of 265 million percent (or $2.65m per $1 initially invested). The biggest surprise? It’s not a tech stock…

Estate attorneys in the US are creating trusts aimed at extending wealth until people who get cryonically preserved can be revived, even if it’s hundreds of years later. These revival trusts are an emerging area of law, but are being taken seriously enough to attract true believers and merit discussion at industry conferences.

Nothing to do with markets, but interesting nonetheless. Why is Chile so long?

Important information

Capital at risk. The value of your portfolio with InvestEngine can go down as well as up and you may get back less than you invest. ETF costs also apply.

This communication is provided for general information only and should not be construed as advice. If in doubt you may wish to consult a professional adviser for guidance.

Tax treatment depends on personal circumstances and is subject to change, and past performance is not a reliable indicator of future returns.