{kind=link}

Mounting geopolitical challenges, the rapid deglobalisation of the economy, and the emerging use of technology in defence and national security apparatus are driving a widespread uptick in military and defence expenditures.1 By 2030, it has been projected that global military and defence spending will grow nearly 40% to reach approximately $3.3 trillion, an increasing share of which is likely to go towards artificial intelligence (AI), cybersecurity, and other defence technologies.2 It is anticipated that businesses and solution providers throughout the value chain may be well-positioned to benefit, including major military contractors with specialised knowledge, suppliers of cutting-edge components and hardware, and providers of defence-specific security software. For investors, this secular growth opportunity could offer exposure to a compelling macro trend rooted in innovation.

Key takeaways

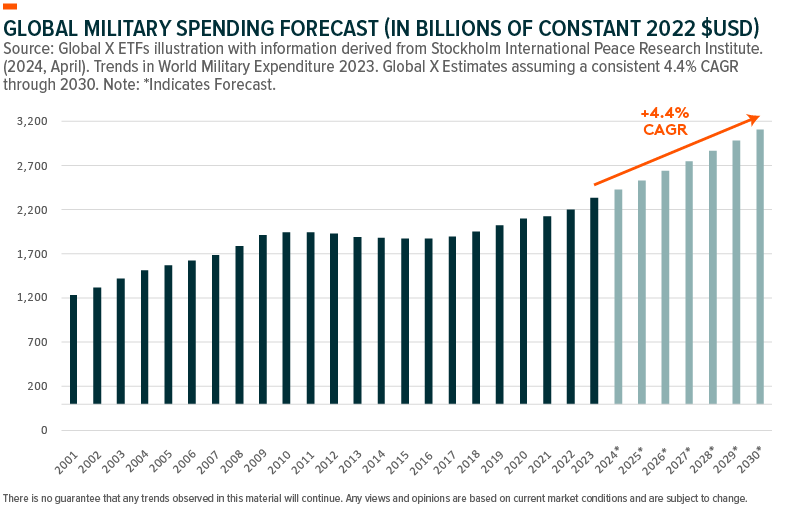

- Since 2020, military spending has accelerated by about 4x to 4.4% Year-over-Year (YoY) Compound Annual Growth Rate (CAGR).3 Growth is expected to remain at these elevated levels through 2030.4

- The defence sector’s projected uptick in software and systems development requires specialised hardware, creating demand for providers of sensors, advanced components, AI chips, and other hardware-based processing, sensing, and networking solutions.

- Cyberspace transcends geographical boundaries, and safeguarding citizen, corporate, and military interests in the digital realm is a focus for countries.

Global defence spending has continued to trend higher

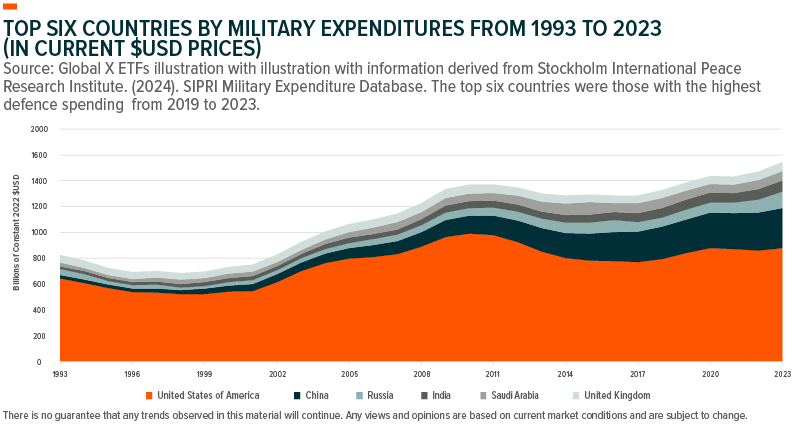

In 2023, global military spending increased for the ninth consecutive year to reach a record $2.44 trillion.5 The United States stood out as the world’s foremost military spender with military expenditures totalling a staggering $916 billion.6 That outlay was 37.5% of total global military spending and three times more than the world’s second-largest spender, China.7 Russia, India, and Saudi Arabia rounded out the top five. Jointly, this group accounted for 63% of the world’s military expenditure.8

A combination of geopolitical tension, deglobalisation, and technological advancements may sustain the upward trajectory in defence spending. Between 2010 and 2020, global military spending grew at an approximate compound annual growth rate (CAGR) of 1%.9 But since 2020, military spending growth has accelerated by roughly 4x to 4.4% YoY CAGR.10 It is anticipated that growth may continue at these elevated levels through 2030, surpassing $3.3 trillion.11

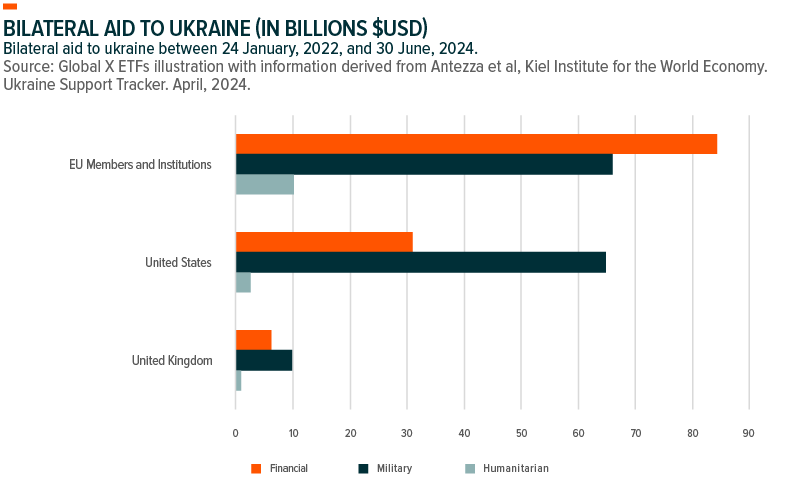

Instability in Eastern Europe appears to be one of the factors driving the recent uptick in spending. The U.S. government has provided more than $107 billion in humanitarian, financial, and military aid to Ukraine since the start of the war with Russia.12 Many other countries, including NATO and European Union members, are also contributing sizeable aid packages to Ukraine.13

Europe’s military expenditure has reached its highest levels since the Cold War, driven by Russia’s invasion of Ukraine.14 2023 saw a significant 16.4% YoY increase in defence investments.15 The United Kingdom was amongst the top spenders among European nations, ranking sixth globally and contributing 3.0% to the global defence budget, surpassing Germany at 2.6% and France at 2.4%.16 These expenditures are inclusive of contributions aimed at supporting Ukraine.17

Shifting focus outside of the Russia-Ukraine War, China boosted its defence budget for the 2024 by 7.2% YoY reaching $232 billion, despite broad economic weakness.18 Similarly, Taiwan, in response to China’s extensive military exercises, proposed a record-high defence budget of $19.1 billion for 2024, a 7.7% YoY increase, bringing its overall defence spending to approximately 2.5% of GDP.19

Not surprisingly, U.S. investments in military and defence initiatives show no signs of abating. The Biden Administration’s Fiscal Responsibility Act of 2023, adopted a proposed topline of $886 billion for fiscal year 2024 defence spending, a 3.2% increase from FY 2023. $842 billion of that $886 billion is earmarked for the Defence Department.20

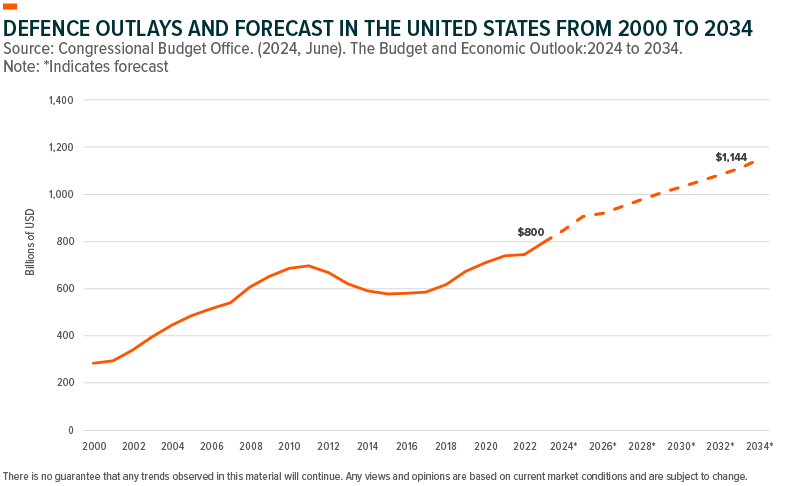

Projections from the U.S. Congressional Budget Office suggest that defence spending will reach $1.14 trillion and represent 2.6% of the GDP by 2034.21

The digitisation of defence is upon us

In the past, military spending primarily focused on acquiring conventional hardware and ammunition. Now, the budget allocation landscape is shifting towards digitisation. Emerging military and security technologies, such as artificial intelligence, cybersecurity, and technology convergence, may be regarded as major drivers behind this surge in defence technology spending.

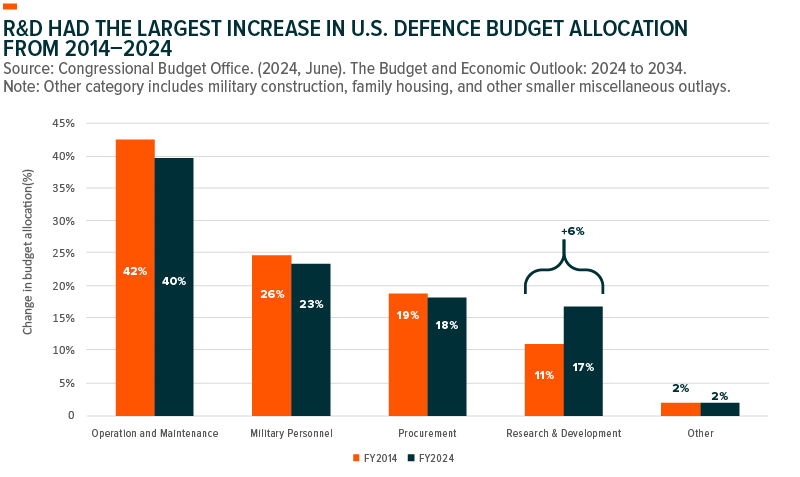

A reliable indicator of a country’s commitment to advancing defence technology is its research and development (R&D) budget. For the United States, the notable increase in R&D over the past decade from 12.8% of its total defence budget allocation in 2013 to 16.8% in 2025, marks a strategic shift for the Department of Defence (DoD).22,23 The DoD’s Fiscal Year (FY) 2025 budget allocates $143.2 billion to R&D, a 10% increase from FY 2023.24 It earmarks $17.2 billion for science and technology initiatives and $1.8 billion to advancing AI capabilities.25

Among the more notable emerging technologies in development are lethal autonomous weapon systems (LAWS). Defined as weapons that autonomously identify, target, and engage adversaries with limited human intervention, LAWS harness the power of high-speed computers, the interconnectedness of the Internet of Things (IoT), and sophisticated big data algorithms. Governments around the world, the United States and China especially, believe that they can secure a competitive military advantage through the development and deployment of LAWS.26

In the growing defence technology market, the software and hardware industries’ presence take on added significance. The global defence information technology (IT) spending market was valued at $79.68 billion in 2020 and is projected to reach $137.65 billion in 2030.27 The defence sector’s uptick in software and systems development requires specialised hardware, creating demand for providers of sensors, advanced components, AI chips, and other hardware-based processing, sensing, and networking solutions.

This uptick could also create opportunities for new partnerships between the public and private sectors, including those that specialise in data analytics and artificial intelligence/machine learning (AI/ML). Looking at the U.S., in May 2024, Palantir secured a significant contract from the Department of Defence’s Chief Digital and Artificial Intelligence Office (CDAO) for its AI-enabled operating system, starting with an initial order of $153 million, potentially extending up to $480 million over five years.28 Additionally, Palantir received a $33 million prototype contract to integrate third-party vendor and government capabilities into the Palantir-operated data environment, supporting Combatant Command digital needs.29

In March 2024, Palantir secured a contract valued at $178.4 million by the Army Contracting Command to develop and deliver the Tactical Intelligence Targeting Access Node (TITAN) ground station system, the Army’s next-generation AI/ML-enabled deep-sensing capability.30 The contract includes the creation of 10 TITAN prototypes, integrating advanced technologies for real-time actionable intelligence and enhanced mission command.31 TITAN will connect to various sensors, reducing sensor-to-shooter timelines and improving the accuracy of long-range precision fires.32

The U.S. government is also collaborating with defence tech companies like General Dynamics and Rheinmetall who are actively involved in replacing the aged U.S. Army’s Bradley Fighting Vehicle using detailed digital designs and prototypes for testing, a project valued at around $45 billion.33 Lockheed Martin has boosted its directed energy weapon for the DoD, scaling its 300 (kilowatt) kW laser to an impressive 500 kW.34 This laser’s accuracy is refined through precise target tracking data from radar and sensors, promoting effective target destruction.35

Cyberspace is the new battleground

Modern warfare is not restricted to bullets and missiles. Cyberspace transcends geographical boundaries, and safeguarding citizen, corporate, and military interests in the digital realm is a major challenge for countries. Consequently, countries are increasingly exploiting cyber vulnerabilities to achieve and attain military objectives. Organised and criminal hacking is rampant, often causing massive public disruption.36 In May 2021, a hacker group disrupted the computer systems of Colonial Pipeline, an oil pipeline based in Texas that supplies nearly half of the fuel to the East Coast.37 The attack forced the pipeline to halt operations for about five days, leading to shortages of gasoline, diesel, and jet fuel. Cybersecurity companies implementing Zero Trust Architecture and Endpoint Detection and Response solutions could stand to benefit from demand from companies and institutions seeking such solutions.38

Cybersecurity is a vast frontier in comprehensive defence operations. Recent U.S. legislation designed to modernise and secure defence systems, government agencies, and critical infrastructure underscore the commitment required. The Infrastructure Investment and Jobs Act included roughly $1.9 billion in cybersecurity funding for state and local government grants, the electrical grid, and Department of Homeland Security (DHS) cybersecurity research.39

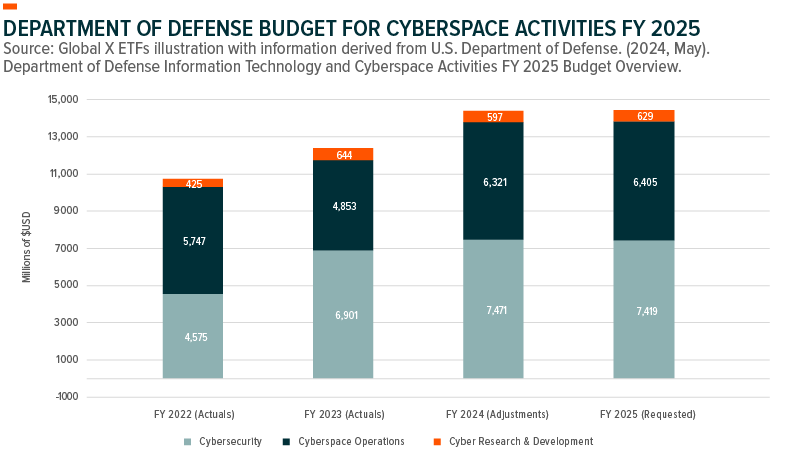

Cybersecurity is a primary concern for the DoD, which divides its cyberspace activities (CA) budget into three portfolios: cybersecurity (requested $7.4B FY25), cyberspace operations (requested $6.4B FY25), and R&D (requested $.6B FY25).40 The requested CA budget for FY 2025 is nearly $14.5 billion, a more than $2 billion increase from FY 2023.41

The DoD has also devised its Software Modernization Strategy, which outlines priority tasks such as accelerating the DoD enterprise cloud environment, establishing a department-wide software factory ecosystem, and transforming processes through digitisation to enable resilience and speed.42 The DoD’s Future Years Defence Plan states that air platforms and platform systems, hypersonic and strategic strikes, air and missile defence systems, and space and space-based systems are among the areas receiving the greatest portion of funding for defence tech innovation through 2027.43

As emerging technologies like AI present new cyber challenges and vulnerabilities, the onus is on governments to devise solutions, which can include diplomacy. For example, in February 2023, at the first ever Responsible Artificial Intelligence in the Military Domain (REAIM) Summit at The Hague, the U.S. State Department proposed the “Political Declaration on Responsible Military Use of Artificial Intelligence and Autonomy,” a plan to ensure that military AI adheres to international humanitarian law and requires each country to establish its own principles for AI-enabled systems.44 Additionally, the proposal mandates that AI capabilities must disengage from the system if they operate unintentionally.45

ARMR LN: an ETF targeting innovative defence tech

The Global X Defence Tech UCITS ETF (ARMR LN) invests in pureplay defence technology companies that derive 50% or more of their revenues from the sub-categories outlined below. The fund is generally unconstrained by geographical limitations and thus seeks to cast a wide net capturing disruptive defence technology companies. The sub-categories for inclusion involve:

- Cybersecurity: Companies involved in the development and management of defence-related security protocols preventing intrusion and attacks to systems, networks, applications, computers, and/or infrastructure for local and/or national defence applications.

- Defence Technology: Companies involved in the development of artificial intelligence (AI), internet of things (IoT), augmented/virtual reality (AR/VR), human-machine collaboration, big data, specialised 3D light detecting and ranging (LiDAR), geospatial intelligence, and/or security scanning solutions (e.g., biometrics, credential authentication, etc.) for local and/or national defence purposes.

- Advanced Military Systems and Hardware: Companies involved in the development of robotics, drones, advanced weapon systems and military munitions, defence-specific power and fuel systems, sensor arrays, processors and networking equipment, space launch systems (including satellites), radar systems, and/or military aircraft/vehicle production, for local and/or national defence purposes.

Conclusion: Defence tech may offer secular growth

The global defence industry appears to be an expansive, rapidly growing market with annual spending in the trillions. Escalating geopolitical concerns, the digital transformation of warfare, and the increasing importance of cybersecurity are possible growth drivers. As the world becomes more interconnected, cyberattacks are becoming more frequent and sophisticated, prompting militaries to adopt cutting-edge technologies such as AI, drones, and cyberwarfare capabilities. Their adoption creates a growing market for defence companies and could presents a compelling opportunity for investors seeking exposure to a sector with potential sustained growth. Exposure to the future of the defence industry means exposure to technological innovation and development.

The risks of investing in ARMR LN are Currency Risk, Derivatives Risk, Equities Risk, Concentration Risk, Market Risk, Operational Risk (including safekeeping of assets), Risks associated with the ability to track an index and Liquidity Risk. More details regarding the risks of investing and in this ETF specifically is available in the ‘Risk Factors’ section of the Prospectus.

Educational content produced as part of a paid partnership

Global X insights do not take into account a person’s own financial position or circumstances of any person or entity in any region or jurisdiction. This information should not be relied upon as a primary basis for any investment decision. Its applicability will depend on the particular circumstances of each investor. Any views and opinions are based on current market conditions and are subject to change. This information is not intended to be, nor does it constitute, investment research.

This document is not intended to be, or does not constitute, investment research as defined by the Financial Conduct Authority

1. Global X Forecast with information derived Stockholm International Peace Research Institute. SIPRI Military Expenditure Database: Military expenditure by region in constant US dollars. (22 April, 2024)

2. Ibid.

3. Ibid.

4. Ibid.

5. Stockholm International Peace Research Institute. Global Military spending surges amid war, rising tensions and insecurity. 22 April, 2024.

6. Ibid.

7. Stockholm International Peace Research Institute. SIPRI Military Expenditure Database: Military expenditure by country in current US dollars 2023. Accessed August, 2024.

8. Ibid.

9. Stockholm International Peace Research Institute. SIPRI Military Expenditure Database: Military expenditure by region in constant US dollars 2023. Accessed August, 2024.

10. Ibid.

11. Global X Forecast with information derived Stockholm International Peace Research Institute. (22 April, 2024), Global military spending surges amid war, rising tensions and insecurity. Trends in world military expenditure, 2023.

12. Council on Foreign Relations. How Much Aid Has the U.S. Sent Ukraine? Nine charts illustrate the extraordinary level of support. 9 May, 2024.

13. Ibid.

14. VOA News. (2023, April 24). Highest Military Spending in Europe Since Cold War: Study.

15. Stockholm International Peace Research Institute. SIPRI Military Expenditure Database: Military expenditure by country in constant US dollars 2023. Accessed August, 2024.

16. Ibid.

17. Ibid.

18. Nikkei Asia. China defense budget grows 7.2% despite other ‘belt-tightening’. 5 March,2024.

19. Global Taiwan Institute. Taiwan Announces an Increased Defense Budget for 2024. 20 September, 2023.

20. National Guard Association of the United States. (2023, June 6). Fight to Increase Defence Spending Continues.

21. Congressional Budget Office. An Update to the Budget and Economic Outlook: 2024 to 2034. 18 June, 2024.

22. Office of the Under Secretary of Defence (Comptroller). (March, 2024). Department of Defence Budget for Fiscal Year 2025.

23. Office of the Under Secretary of Defence (Comptroller). (March, 2014). National Defence Budget Estimates for FY 2015.

24. U.S. Department of Defence. (March 2024). Department of Defence Releases the President’s Fiscal Year 2025 Defense Budget.

25. Ibid.

26. National Defence University Press. (2023, July 7). A Framework for Lethal Autonomous Weapons Systems Deterrence.

27. Allied Market Research. (2021, August). Defence IT Spending Market by System, Type, and Force: Global Opportunity Analysis and Industry Forecast, 2021-2030.

28. Palantir Newsroom. Palantir Selected by Chief Digital and Artificial Intelligence Office (CDAO) to Participate in Scaling Data Analytics and AI Capabilities Across the Department of Defense in Support of CJADC2 Strategy. 30 May, 2024.

29. Ibid.

30. Palantir Newsroom. Army Selects Palantir to Deliver TITAN Next Generation Deep-Sensing Capability in Prototype Maturation Phase. 6 March, 2024.

31. Ibid.

32. Ibid.

33. Bloomberg. (2023, June 26). General Dynamics, American Rheinmetall to Compete for US Army Vehicle.

34. Lockheed Martin. (2022, August 11). Inside the Lockheed Martin Laser Technology.

35. Ibid.

36. Infosecurity Magazine. (2022, November 3). “Disturbing” Rise in Nation State Activity, Microsoft Reports.

37. Cybersecurity & Infrastructure Security Agency. The Attack on Colonial Pipeline. 7 May, 2023.

38. Ibid.

39. BGR Group. (2022). Infrastructure Investment and Jobs Act – Cyber Security.

40. Department of Defence Information Technology and Cyberspace Activities FY2025 Budget Overview. May 2024.

41. Ibid.

42. Department of Defence (2023, March). Software Modernization Implementation Plan Summary.

43. McKinsey. (2022 November 4). How will US funding for defence technology innovation evolve?

44. Nikkei Asia. (2023, June 14). U.S. seeks talks with China on military AI amid tensions.

45. Ibid.