{kind=link}

Olympian bonuses

With the Olympics now in full swing, here’s how much each country pays its competitors as a bonus for winning a gold medal.

Not all pay a cash bonus, though. Kazakhstan, for example, rewards its Olympians with an apartment – the size of which depends on their medal colour. 3 rooms for gold, 2 for silver, 1 for bronze.

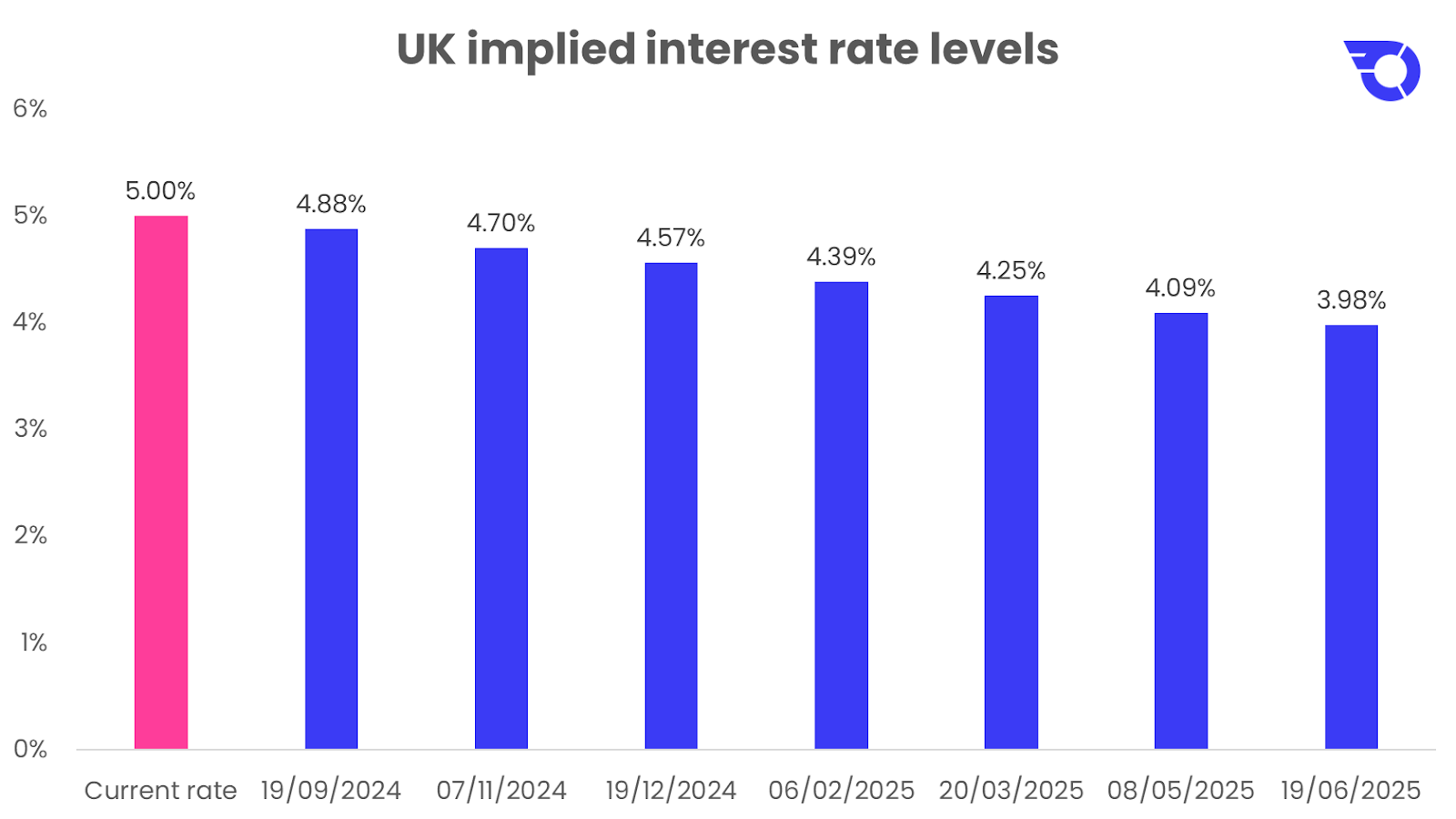

The Bank of England cuts rates

We saw a full house of interest rate movements this week. The Bank of Japan hiked, the Fed kept rates on hold, and the Bank of England made its first cut.

The UK’s central bank cut rates for the first time since 2020, reducing their base rate from 5.25% to 5%. The decision was voted through by a slim majority, with the Monetary Policy Committee voting five to four in favour of a cut. The central bank also published inflation forecasts suggesting that further cuts lie ahead, and the market now expects at least one further rate cut by the end of the year.

The small cap rotation

The rotation out of large (predominantly technology) companies and into smaller companies is being driven by inflation expectations, with the start of the selloff immediately following the CPI release in July:

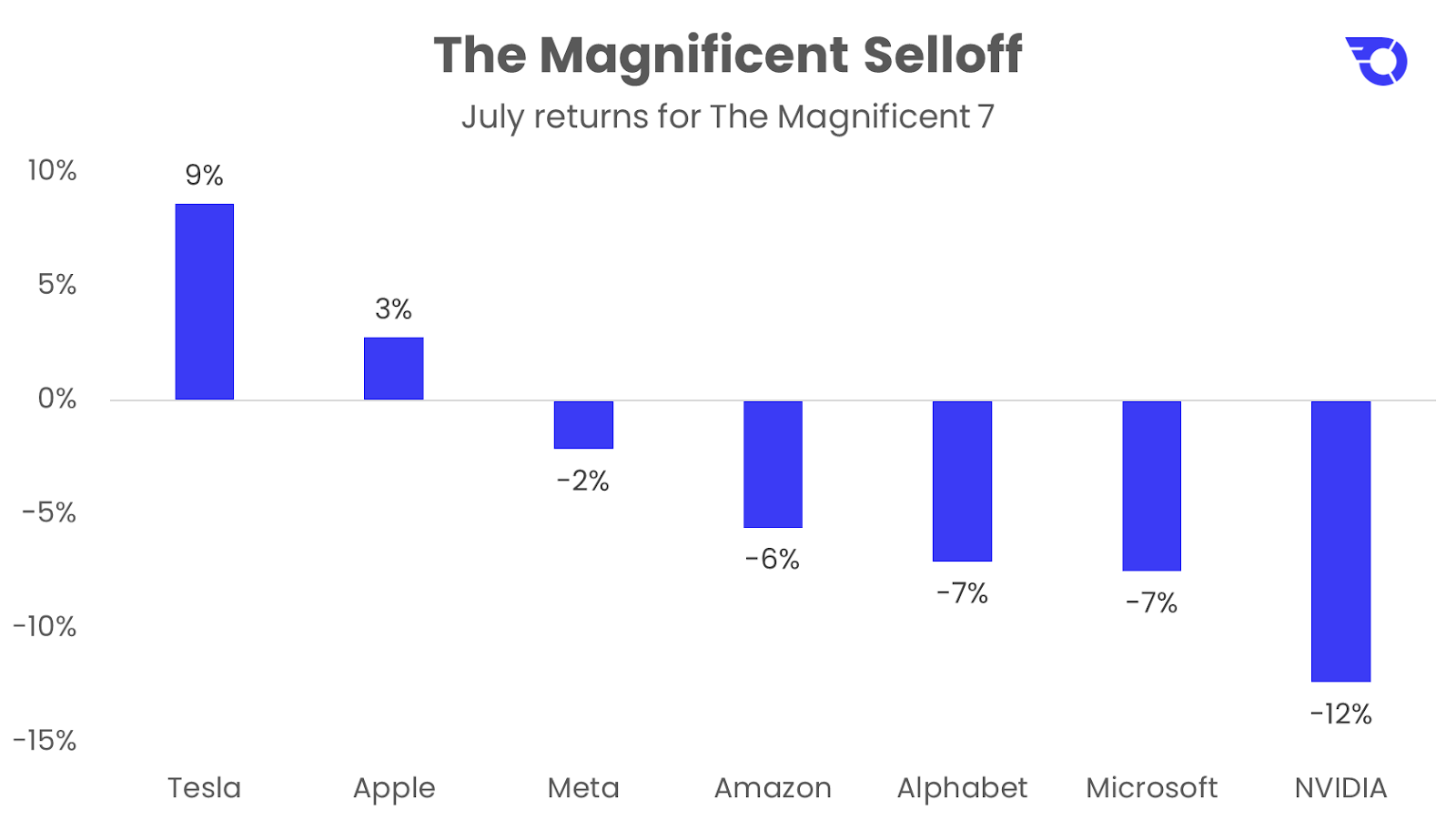

The Magnificent Selloff

It’s been a tough week for The Magnificent 7 tech stocks. All bar NVIDIA have now reported earnings, and the reaction to earnings misses, as seen from Alphabet, Tesla, Amazon, and Microsoft, show that investors are swift to punish anything other than unequivocal good news:

Finding needles in haystacks

A new paper has been released which looks at the distribution of stock market returns. The paper comes from the same author who famously calculated that just 4% of companies accounted for all the wealth gains for the entire US stock market since 1926, and that over half of stocks (55%) actually underperformed 1-month US treasury bills over the period.

This new paper looks into what those biggest winners were, reinforcing the idea that the stock market is driven not by the majority of stocks, but by a tiny handful of companies generating exceptionally high returns, which generate enough to offset the vast majority of underperforming stocks.

The paper shows that the median stock (i.e. the one which would be in the middle if you lined all stocks up in order of worst performing to best performing), had a negative cumulative return if you’d held it for almost 100 years. The implication is that most stocks lose money if held indefinitely. On the other hand, the mean return for all stocks was almost 23,000% – showing emphatically that the tiny handful of exceptional stocks have generated so much that they’ve pulled up the average stock performance, and therefore the market, by a huge amount:

Important information

Capital at risk. The value of your portfolio with InvestEngine can go down as well as up and you may get back less than you invest. ETF costs also apply.

This communication is provided for general information only and should not be construed as advice. If in doubt you may wish to consult a professional adviser for guidance.

Tax treatment depends on personal circumstances and is subject to change, and past performance is not a reliable indicator of future returns.