{kind=link}

In response to rising inflation, the Bank of England has raised interest rates to more (historically) ordinary levels, after a long period of extremely low rates. Savers should start to see this reflected in their accounts.

However, when you factor in the extremely high rate of inflation and the soaring cost of living caused by it, most savers that predominantly hold their savings in cash will still see their wealth eroded over time. Even with some savings accounts paying around 5% a year, there are still no accounts on the market that come close to beating the current rate of inflation.

Despite the recent turbulence in both equities and fixed income markets, investing in financial markets remains one of the most reliable methods of wealth creation over the long term.

Historically, timing the market has had an extremely limited success rate. Having said that, because equity and bond returns are positively skewed, we expect to see capital growth over time despite the possibility for more short-term fluctuations.

Given the growing pressure on the cost of living and the eroding purchasing power, we believe investing for the long term should be a key consideration for anyone planning their long-term finances.

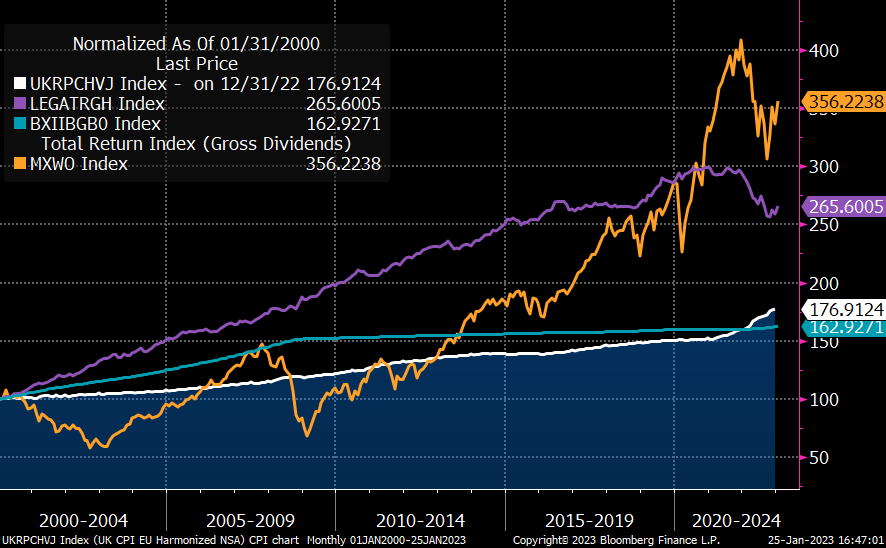

Source: Bloomberg. Date of data: 31/12/1999 to 25/01/2023

Key: White line – UK CPI (UK CPI YoY indexed from 01/2000)

Purple – Global Bonds (Bloomberg Global Aggregate)

Blue – GBP Cash (GBP Overnight Cash)

Orange – Global Equities (MSCI World)

With life expectancy increasing, your money needs to take you further than you might think. For a couple aged 65, there is a 92% chance that at least one of the couple will live to 80 and a 51% chance that at least one of the couple will live to 90 (ONS). Investing early helps to prevent any savings shortfall over the long term.

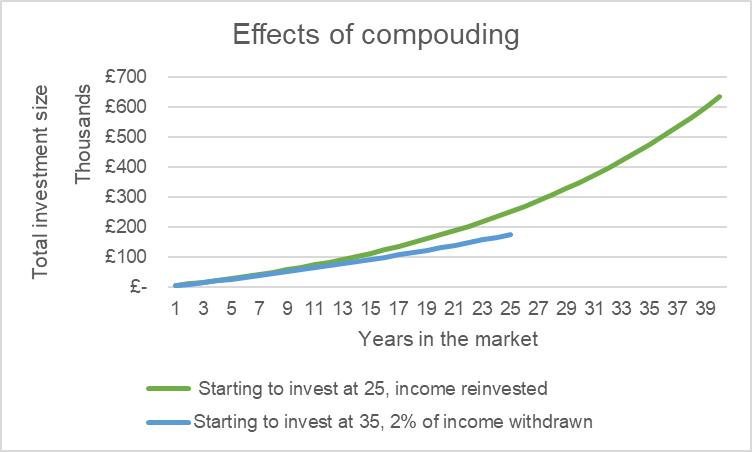

Compounding is a powerful tool

Cash is, rarely, king. Even with interest rates higher than we’ve seen in recent years, the fact that inflation is well above central bank targets means that there is a widespread drain on cash savings.

With the power of compounding on your side, starting your investing journey earlier and reinvesting any returns gives your investments the chance to grow and snowball over time.

For example, imagine you invested £5,000 annually, starting at 25, with an annual growth rate of 5%. If you reinvested the income, this could translate to £634,000 by the time you reached 65.

If this annual investment journey was delayed by 10 years to 35, and the investor chose to take 2.5% of the income every year, the end value by 65 would translate to just £175,000.

How risk impacts your investment prospects

Risk and return, generally, go hand in hand. It’s important to note that each individual investor’s risk tolerance is an important factor in determining their investment goals. Conservative investors, for example, are likely to prefer government bonds over riskier stocks.

Either way, over the long term, both asset types have been shown to outperform cash savings.

Investing in global equities could be the route to higher potential returns but it may come with higher ups and downs along the way (higher volatility). Investing in cash offers a smoother journey but is likely to be a route to lower real returns.

Volatility is part of the investing journey and market conditions are changeable by definition. Despite the temptation to alter your investing strategy in the face of market turbulence, it is almost always best to stay on course. Timing the market is notoriously difficult to get right and staying invested has proved to be a better way of achieving a more favourable outcome.

Volatility can be mitigated by investing across a number of different asset classes and regions. This is known as diversification, the idea that reducing overexposure to a particular sector or stock can mitigate a negative event happening in one particular holding. Diversification can be achieved by having a blend of fixed income, equities and even commodities.

To protect from capital gains tax, investors may choose to put their investment under an ISA (Individual Savings Account). This carries an annual limit of £20,000 at present and is available on InvestEngine. If you’re saving for retirement, a pension may be a better option. Either way, follow the button below to find out what an InvestEngine ISA could do for your long-term financial wellbeing.

Capital at risk. The value of your portfolio with InvestEngine can go down as well as up and you may get back less than you invest. ETF costs also apply.

This communication is provided for general information only and should not be construed as advice. If in doubt you may wish to consult a professional adviser for guidance.

Tax treatment depends on personal circumstances and is subject to change. Past performance is not a reliable indicator of future returns.